By Maj Soueidan, Co-founder GeoInvesting

Crexendo, Inc. (NASDAQ:CXDO) Specializes in offering Unified Communication as a Service (UCaaS) solutions and phones to small and medium sized businesses (SMB). I believe the company is reaching an organic growth inflection point that will be accelerated by

- SMBs are more widely adopting UCaaS solutions and ditching their more expensive and feature-limited on-premise communication solutions which require expensive upfront licensing fees.

- COVID-19 putting pressure on companies to move up their UCaaS adoption timeframes

- Consummating several acquisitions over the next several years

Quick Timeline Of GeoInvesting Coverage

June 18, 2018 - Noted we would dig into deeper after Maj met management at the LD Micro conference in early June.

August 6, 2019 - Offered reasons for tracking and mentioned looking to establish position.

October 3, 2019 - Contributor article lays out bullish view on CXDO

November 5, 2019 - Added CXDO to our favorite stock portfolio

April 20, 2020 - Added to our long position

What are Unified Communications?

The Unified Communication (UC) solutions primarily consist of two categories – Cloud-based and On-premise.

Cloud-based communications typically involve no hardware costs. They reduce complexity, eliminate capital expenditure (CAPEX) and lower the total cost of ownership versus on-premise deployments. Companies typically pay a monthly fee based on the number of "seats" that will connect to a UC platform and flat or per-use fees to use certain services.

Premise-based communications involves installing infrastructure (which includes hardware) at the customer location, and is more than likely associated with higher CAPEX costs and expensive licensing fees. They are also less scalable.

UC allows companies to access the tools for communication via a single application or interface. This includes instant messaging, email fax, VoIP, video, etc. all through a single system.

Some of the key components and capabilities of Unified Communications include:

- Collaboration: UC systems allow workers to collaborate more easily.

- Presence: enables individuals to manage their availability. Users can see who is available and choose the most appropriate communications medium

- Unified Messaging: integration of voicemail, fax, email, instant messaging and other electronic media in a single mailbox.

- Mobility: allows team members to access data and features from any location and any device.

- Contact Center: enhance contact center operational efficiency and service capabilities. Enables companies to serve their customers in a variety of mediums (for example, voice, email, Web chat or SMS); provide wait-time messages, position-in-queue updates; and self-service options with interactive voice response.

- Third-Party App Integration: allows integration with third party apps for business process improvement

- Call recording and dashboards with real-time and historical statistics and analytics for better decision making, especially for client services

Some of the cost savings of for a CXDO type UCaaS would include:

- Reduced upfront costs, since a cloud-based system requires less on-premise hardware

- Less IT staff requirements since the platform runs on the cloud

According to Doug Gaylor, President and COO of CXDO, a business that switches to a cloud communication solution from an on-premise solution can experience cost savings of 25% to 50%.

One of the most common questions I get when I'm pitching CXDO or any other UCaaS stock I own, like Altigen Communications, Inc. (OTCQB:ATGN), is how do companies differentiate themselves in a space with lots of competition that all seem to be doing the same thing, to some degree. Although I could think of things like security, I have to be honest, at some level most top companies I have come across in the UCaaS space don’t seem to be too differentiated in terms of products and services.

On the other hand, what I have noticed is that the ones that are excelling have deep roots in the industry with experienced management, along with legacy customer and partner relationships. And that's exactly how I'd describe CXDO.

Furthermore, with only 30% UCaaS penetration, the SBM UCaaS space is wide open and its adoption is just beginning to gain steam. Because this is an industry in which CXDO is squarely situated, I am not too worried about differentiation over the next few years.

As of Q1 2020, CXDO derived 85%, or $3.3 million of its revenue from its UCaaS business, where customers pay monthly recurring fees, 10% from product revenue and 5% from legacy website hosting services that are being phased out.

Reasons I Like CXDO

Management Track Record

What I think we have here is a microcap company being led by a Fortune 500, capable management team. If you reach out to the management trio of...

- CEO - Steven Mihaylo

- COO/President - Doug Gaylor

- CFO - Ron Vincent

… you will quickly conclude that they really understand the UCaaS business and the company’s role in the space. You will also see that Mihaylo and Gaylor have decades of telecom industry experience.

I have met COO/President Doug Gaylor and CFO Ron Vincent, on several occasions, with the first encounter being at an LD Micro Conference a few years ago. I've interacted with Mihaylo on LinkedIn and it seems he's still as passionate about building a business as he has ever been.

I really like companies run by management team members who experienced success working together in the past. You get that with Mihalyo and Gaylor, who have worked with each other for the last 32 years. The company they worked together at was Inter-Tel, which was founded by Mihalyo in 1969. Looking at the description of Inter-Tel, you'll notice it sits in a similar space as CXDO.

"Inter-Tel offers value-driven communications products; applications utilizing networks and server-based communications software; and a wide range of managed services that include voice and data network design and traffic provisioning, custom application development, and financial solutions packages. An industry-leading provider focused on the communication needs of business enterprises, Inter-Tel employs approximately 1,940 communications professionals, and services business customers through a network of 57 company-owned, direct sales offices and approximately 300 authorized providers in North America, the United Kingdom, Ireland, Australia and South Africa."

Inter-Tel was a NASDAQ listed company that went public in the early 1980s through a traditional IPO. Gaylor joined Inter-Tel in 1987 and worked alongside Mihaylo to grow the company to $500 million in revenue before selling it off to Mitel in 2007 for ~$720 million.

“Mr. Mihaylo was appointed our Chief Executive Officer in 2008 and Chairman of the Board in November 2010. Mr. Mihaylo is the former Chairman and Chief Executive Officer of Inter-Tel, Incorporated (“Inter-Tel”), which he founded in 1969 and where he continued to serve until 2007. Mr. Mihaylo led the development of Inter-Tel from providing business telephone systems to offering complete managed services and software that help businesses facilitate communication and increase customer service and productivity. Before selling Inter-Tel to Francisco Partners (Mitel was a portfolio holding), a private equity firm, for approximately $720 million in 2007, Mr. Mihaylo grew the business to nearly $500 million in annual sales. The Board nominated Mr. Mihaylo to the Board in party because he is the Chief Executive Officer of the Company and has more than 40 years of experience in the industry in which the Company competes.”

Gaylor continued to excel after Inter-Tel merged with Mitel:

“Doug was responsible for overseeing the sales efforts in the Western United States where he was ultimately responsible for the activities of approximately 200 sales representatives. Under his leadership as Senior VP, yearly sales for his region reached over $175,000,000 annually.”

It seems Mihaylo wanted a better takeover price than he got in the Mitel deal. So, what do you do in such a situation? Well, you do it all over again.

Mihaylo first showed up as an investor in CXDO through a 2006 proxy filing revealing that he owned 670,000 shares. He later filed a 13G in September 2007 showing that he owned 1 million shares. He was appointed as CEO of Crexendo in 2008 (originally named iMergent) and started rebuilding the core team that worked with him at Inter-Tel. Doug Gaylor, along with Nishith Chudasama (who was also a part of Inter-Tel) were on-boarded in 2009. Vincent joined the company in 2012 after working at Ernst & Young since 2005. This core group has since been building the company into a growing UCaaS company, iMergent. In 2011, management changed the name of the company to Crexendo and eventually made the move to shed the underperforming legacy business to focus on launching its UC business by initially targeting the iMergent web hosting customers which consisted of small and medium sized businesses:

“We provide a variety of cloud-based infrastructure services to all sizes of businesses. Our services include high-quality voice and messaging services over broadband networks, Do-It-For-Me and Do-It-Yourself content management and website building tools, online marketing, online lead generation, e-commerce technology, and training solutions that enable entrepreneurs and small and medium–sized businesses to build and maintain an effective online presence.” Source: 2011 10K

This was definitely a gutsy call since, despite losing a ton of money, the web hosting business was once generating annual revenue in excess of $100 million. You can read more about these changes here and here.

So, it’s impressive that management has been able to grow its UC business to reach profitability from virtually nothing as it wound down web hosting.

It’s also impressive that the company has built its UCaaS offering organically and with less dilution than I would have anticipated. In 2011, the company had shares outstanding of 10.5 million with virtually zero UC revenue compared to the current share count of 14.8 million and a UC annual revenue run-rate of around $13 million.

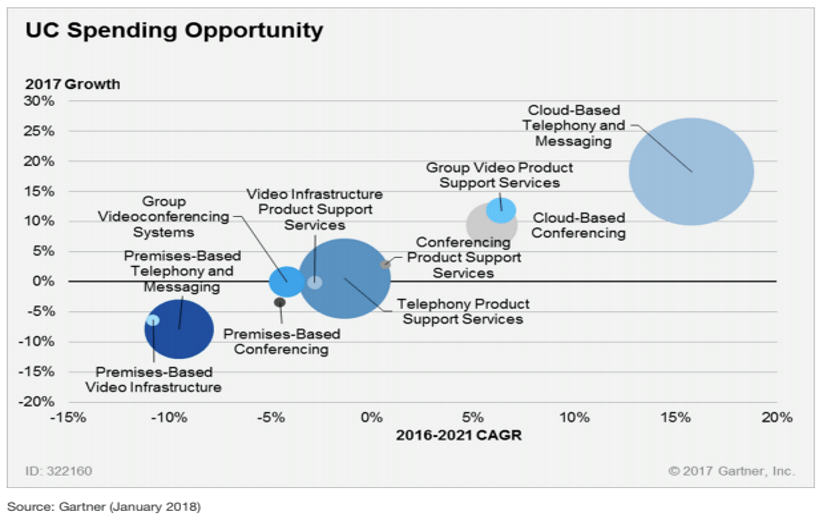

Industry

The global UCaaS adoption is still in its infancy with penetration below 30%, according to Synergy Research Group. Gartner estimates that the rate of organizations deploying cloud telephony is going to double between 2017 and 2021. As seen from the figure below, the premise- based communication solutions yielding to cloud-based and UCaaS service companies are seeing a tremendous growth in the range of 20% to 30% CAGR.

The strong growth will be supported by small and mid-sized businesses that are more aggressively adopting cloud solutions at a much higher rate than the enterprise customers. According to Synergy Research, SMB market accounts for nearly 90 percent of UCaaS adoption. CXDO caters to small and medium businesses and is well positioned for this opportunity. IDC estimates the total market opportunity will reach ~$54 billion by 2022.

Gaylor uses an analogy that the UCaaS industry today is akin to what the smartphone market was over the last 11 years - from almost no penetration to nearly 100% penetration. We could see a similar path for the UCaaS market. The market is already witnessing very fast migration from the traditional legacy premise-based equipment to the cloud.

Furthermore, COVID-19 is accelerating the adoption of UCaaS by SMBs. The coronavirus outbreak has resulted in many businesses allowing employees to work from home or even requiring them to work remotely in compliance to government mandates. Many businesses are seeking alternatives to traditional meetings and business travel. Even before COVID-19, we thought that Crexendo was positioned to expand its customer base as more and more firms sought and continue to seek a transition away from costly old-school on-premise communication solutions to more flexible communications platforms that allow efficient operation on the cloud. Furthermore, CXDO’S services may be even more attractive to businesses now as they look to cut costs.

Growth Plan

The company’s growth strategy revolves around three aspects – Partner Sales, Direct Sales and M&A.

CXDO currently has relationships with 240 Partners, with plans to add 3-5% every quarter. These partners primarily fall under 4 categories:

- Traditional Telecom value added resellers (VARs), companies that sell phone services and CXDO is part of those services.

- Data & B2B VARs include copier companies, cellular companies and any other type of B2B companies for whom UC system can be complementary to their existing offerings

- Managed Service Providers (MSPs), companies that offer consulting services to businesses suggesting the best UCaaS system for their needs.

- Master Agents, companies with multiple UC solutions (from different providers) in their portfolio which in turn they offer to their partners and sub-agents

Of these, the biggest area of growth is B2B VARs. More than two years ago, Crexendo was chosen by US Cellular (the 4th largest cellular company in the US) to be their exclusive partner to provide UC systems to US Cellular business and government customers. This was done after a fairly exhaustive search by US Cellular which all the more validates CXDO’s capabilities.

In the recent Q1 earnings call Doug Gaylor noted the increasing interest in CXDO’s products from non-telecom entities and has added a number of them over the last six to nine months. For example, a number of copier companies have become Crexendo resellers and partners.

“Those copier companies are challenged right now because nobody is buying copy machines but all of their customers that they have out there are desperately looking for ways to communicate remotely and so having Crexendo in their portfolio has helped them out tremendously. I can’t tell you how many of my copier partners have called to thank us about having Crexendo in their portfolio because their sales staff would have been dead in the water with selling copiers and the fact that they have got other solutions in their portfolio to sell now in these troubled times has helped them out tremendously.” Source Q1 Earnings Call

Overall, I love when smaller companies using partnerships to help drive revenue to help keep marketing expenses reasonable.

The company is also actively targeting M&A as a means to bolster its revenue growth. In fact, it is more focused on acquisitions which are revenue and customer centric rather than technology fits. CXDO is looking at such opportunistic M&A in the range of $10 to$15 million and the pandemic has created more M&A opportunities. In the Q1 earnings call, Steve Mihalyo alluded to seeing a spike in conversations and that there are a lot of opportunities for M&A opportunities the UCaaS industry. Doug Gaylor further added that the company should be ready to announce some news on M&A front by the end of the year.

Predictability / Growth at Inflection point

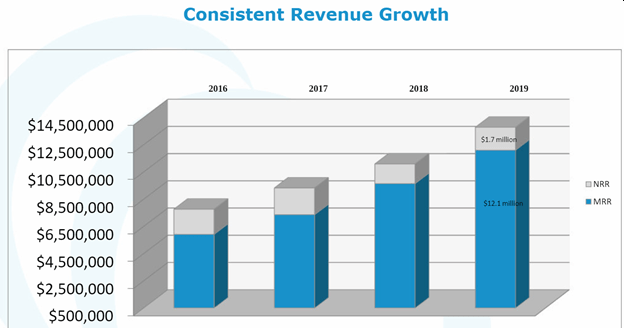

CXDO’s revenue performance shows that their recurring revenue model is doing what a recurring revenue model is supposed to accomplish: Predictability.

The company has posted 20 straight quarters of year over year quarterly growth and 13 quarters of sequential quarterly growth through this streak. More importantly, the company reached and maintained profitability since Q1 2019, a unique accomplishment for a UCaaS company at CXDO’s revenue size.

Source: CXDO June Investor Presentation

- MRR = monthly recurring revenues

- NRR = non-recurring revenues

With cloud gross margins of around 70%, more of the company's new and recurring revenue should drop to the bottom line as operations stabilize (company has been making short-term investments into the business).

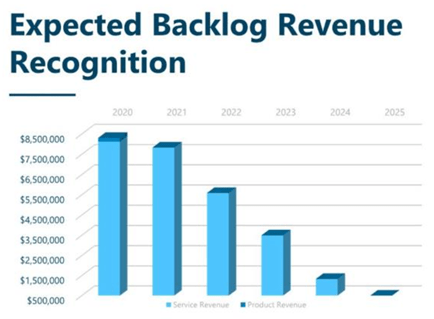

Another aspect that lends to the predictability of CXDO’s model is that it enters into long term contracts with its customers. The sales backlog as of Q1 2020 was $26.6 million, up 10% YOY. Nearly $8 million of that backlog will be recognized in 2020. As shown in the figure below, the backlog scales down a little bit every year over the next few years until 2025, giving a nice visibility into revenue.

To illustrate how backlog is calculated, if a customer signs a $1000 per month agreement with Crexendo for 60 months, CXDO recognizes revenue of $1,000 per month with the remaining amount ($59,000) staying in backlog. The next month, another $1000 moves to revenue and backlog is reduced to $58,000 and so on.

Source: CXDO June Investor Presentation

CEO Won’t Stop Buying Stock

Mihaylo has been backing up the truck, loading shares of CXDO since 2007 when he owned ~1 million shares or ~5% of the company. He now owns 10.3 million shares or 68.7%. I remember a conversation I had with Gaylor and Vincent about this, joking that they keep telling Steve to stop buying since the float was only ~4 million shares! Three days later, a Form 4 crossed showing that Mihalyo was still buying on the open market. He was the majority of CXDO’s daily trading volume on several occasions; He may have been thinking, “Hey, if no one else is going to buy the stock, I will.”

A summary of Steve’s complete Form 4 history is listed here.

Caveats

- Even though COVID-19 may be speeding up the adoption of unified communication services, there still may be a short-term lag in terms of when companies actually deploy capital. Furthermore, CXDO has been giving price concessions to new and current customers, and COVID may lead to some customer attrition. Regardless, UCaaS companies are uniquely positioned to come out stronger than prior to the pandemic.

- Microsoft Corporation (NASDAQ:MSFT) is aggressively entering the unified communications space which could create challenges for all players. However, the SMB space is so wide open right now that given CXDO's small size, we don't think that's a big issue at this point. It's probably more of an issue for a company like $RNG. In fact, it might even create an opportunity for CXDO to find some attractive acquisition candidates that can't compete effectively.

- Valuation Contraction: We have to consider that as the UCaaS space becomes more competitive and more penetrated that overall tier one company valuations in the industry may come down from premium levels over time.

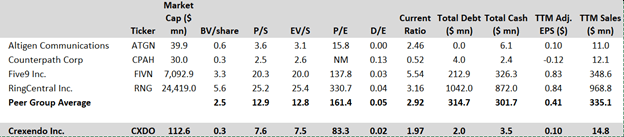

Valuation

With a price to sales and enterprise value to sales of 7.6x and 7.5x respectively, shares of CXDO might look expensive for a small microcap company. However, I think when we will look back at today’s prices, we will consider the stock to be cheap, given that I think

- the pace of organic growth will hold at 20%

- the company is profitable, and

- there is a likelihood that the company is one or two acquisitions away from doubling revenue.

Ultimately, I view CXDO as a bet on a proven management team and believe that the company will be able to maintain a premium valuation, maybe eventually approaching the levels of a tier one player like $RNG.