The bottom line: we believe shares of Crexendo, Inc. (NASDAQ:CXDO), which trade for $3.15, are worth between $4.29 and $5.42 today.

Voice over Internet Protocol (VoIP) is the routing of phone calls over the internet. It uses the internet to deliver packages of data the same way Netflix delivers video: over the cloud. These ‘packages of data’ were once delivered through low margin infrastructures such as landlines and CDs, Over the last ten years, companies like Adobe (ADBE) and Microsoft (MSFT) began discontinuing hardware infrastructure cheaper for more efficient delivery via cloud. It proved to be an extremely profitable move that also catalyzed growth in these companies.

For many businesses, a complete rehaul of service provider and infrastructure was not appealing just for VoIP; landline delivery did the job in its existing infrastructure. However, as life cycles of deployed product ended and services become available, the contemporary alternative became VoIP.

Earlier this year, we presented our research favoring Altigen Communications, Inc. (OTCQB:ATGN), a VoIP and Microsoft Azure service provider. We concluded two findings:

- Cloud Communications is the new, de-facto communication service, with an endless supply of new customers (for the time being).

- Large, yet unprofitable, competitors of this space exhibit tremendous valuations.

We highlighted that Altigen barely traded for 2x sales, while leaders in the space traded above 10x. Those at the top (10x range) as well as those in the middle (3 - 5x range) hardly turned an operating profit. Here is an updated snapshot of the VoIP industry and company valuations.

.JPG)

We suggested Altigen should at least trade for the same multiple as Crexendo. In February 2019, Crexendo traded under 3x revenue - higher than Altigen - and was unprofitable. What it did offer, though, was a holistic suite of services tailored for the cloud telecom space. Seven months later, the company began generating substantial cash flow.

Crexendo, Inc. is a provider of cloud telecom and unified communication services. In the company’s own words:

Our cloud telecommunications services transmit calls using IP or cloud technology, which converts voice signals into digital data packets for transmission over the Internet or cloud. Each of our calling plans provides a number of basic features typically offered by traditional telephone service providers, plus a wide range of enhanced features that we believe offer an attractive value proposition to our customers. This platform enables a user, via a single “identity” or telephone number, to access and utilize services and features regardless of how the user is connected to the Internet or cloud, whether it’s from a desktop device or a mobile device.

*look to the appendix of this report for a description of Crexendo’s features and solutions

Thesis: The VoIP market is expected to grow from $20 billion in 2018 to $55 billion in 2014, according to Global Market Insights. This is driven by the adoption of cloud services and telecommunications infrastructure. Their findings also highlight the crucial factor of and need for ‘workforce mobility,” a dark horse driver for rapid adoption. Most importantly, VoIP cuts the costs of communications for the consumer and the costs of goods for the provider.

Crexendo estimates that 70% of businesses have not switched to cloud services for communication needs.

Again, in Crexendo’s words:

Our goal is to provide a broad range of cloud-based products and services that nearly eliminate the cost of a businesses’ technology infrastructure and enable businesses of any size to more efficiently run their business. By providing a variety of comprehensive and scalable solutions, we are able to cater to businesses of all sizes on a monthly subscription basis without the need for expensive capital investments, regardless of where their business is in its lifecycle.

GMI's work is not the only research out there supporting our thesis.

- Market Research Future reported that the global IP telephony market will witness a 9% CAGR from 2017 - 2023, driven by demand for web-based services across businesses and industries.

- Per a 2016 report, Grand View Research expects the mobile VoIP market to grow to $146 billion by 2024, highlighting wireless bandwidth capabilities and growing telecom service investment. They estimated this market’s value in 2014: only $28 billion.

- Persistence Market Research expects the global VoIP services market to reach $199 billion by the end of 2024. Long-distance/international VoIP phone calls are expected to generate $190 billion in revenue by 2024. Managed IP PBX is projected to be the largest segment by then, exceeding $80 billion in revenue. Computer-to-phone communication is expected to exceed $100 billion in revenue. Finally, the corporate user is expected to account for over $120 billion in revenue by 2024, becoming the largest user.

We feel Crexendo has one of the best growth prospects among its peers. It is a small company providing VoIP with services that compete with the largest providers. Relatively, it exhibits a low valuation. The company already grows north of 20% with a large backlog of orders that virtually guarantees a base revenue stream. We feel 20% growth is sustainable - regardless of a breakout quarter - thanks to the underlying growth in VoIP demand.

Crexendo’s current backlog sits at $24.7 million. This is larger than its trailing twenty-four-month revenue.

Management tells us the company is at its ‘inflection point.’ It is hard to argue otherwise.

Performance

Revenue has grown an average of 5.25% each quarter for nine consecutive quarters, logging net growth in eight of these periods (only one of these periods reported stagnant revenues; revenues declined less than a fifth of a percent that quarter). Gross margin has increased to over 69%, the highest level within the data we looked at (dating back to 2014 when it was below 53%). Churn rate among Crexendo customers is in the mid-single digits; most revenues are recurring. In Q2 2019, the most recent quarter, revenue grew over 21%.

In Q1 2019, Crexendo turned its first profit of approximately $240 thousand, representing 6.93% net margin. Management delivered $340 thousand bottom line in Q2, representing 9.38% net margin. This means revenue grew 3.49% sequentially; almost the entire marginal increase in revenue flowed to net operating profit.

Crexendo has returned over 100% since its 52-week low in September 2018. Reinvigorated growth rates and sustained profitability have led to the valuation today. As Crexendo scales its business, its valuation will gradually resemble price-to-sales ratios of the competition. Crexendo currently delivers an ROIC of 18.68%, well above our estimated WACC of 8.66%. Finally, as mentioned, net margin grew from 6.93% to 9.38% within one quarter.

We feel comfortable with initiating positions at the current valuation.

Crexendo Valuation

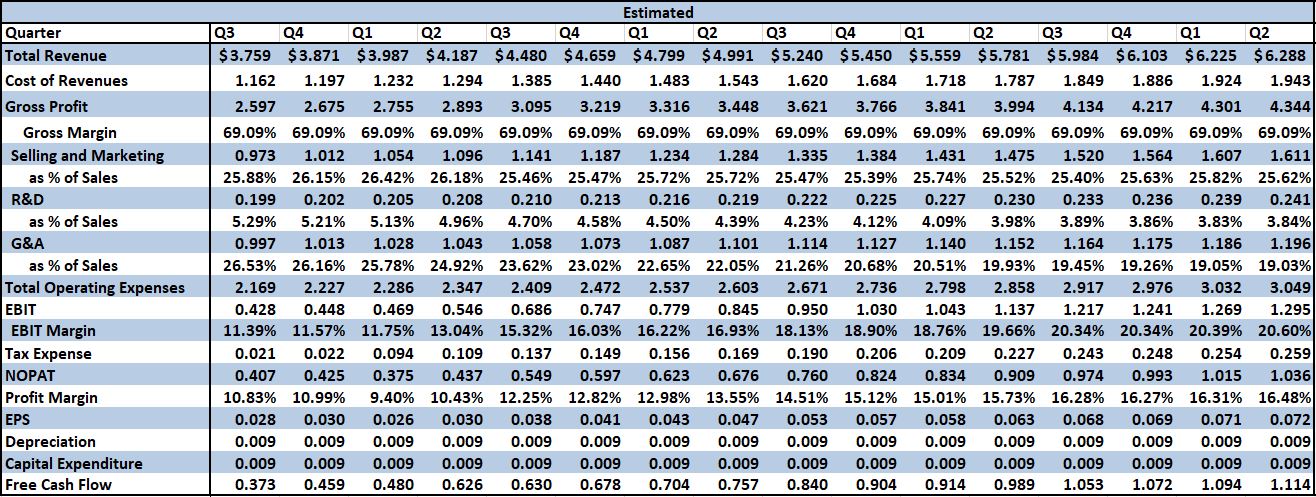

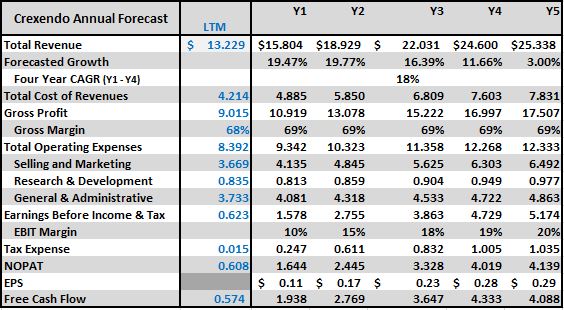

Before we examine comparables, let us look at a more traditional approach. We feel strongly that Crexendo will continue to generate free cash flow.

We will stop short of a breakthrough quarter, although it is certainly possible. We will also cap our forecasted profit margin to under 20%, using Altigen’s current 23% profit margin as a benchmark and target.

We forecast sales to grow at a CAGR of 18% for four years. We model each quarter to grow, on average, $167 thousand in sales or 3.53% quarter-over-quarter. We believe this is possible given the growth trajectory of this industry. Crexendo is preparing to realize $6 - 7 million in backlog revenues for the next two years; historically, Crexendo has been able to grow backlog by under $1 million each quarter. There is runway left for Crexendo to capitalize on sales and distribution channels.

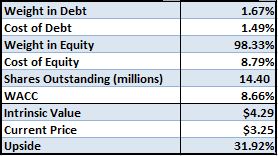

We estimate Crexendo’s WACC to be an adjusted 8.66%. Most of our adjustment comes from a small-cap-beta factor increase. Crexendo’s weight in Equity is over 98% of the capital structure, making the case for a lower cost of capital calculation. However, the security is thinly traded and historically volatile.

Our valuation establishes a $61.7 million price tag on the business currently, or $4.29 a share. This represents 25% upside.

What this also means is, yes, we are bullish towards this entire industry. Crexendo highlights that only 30% of all businesses have switched to the cloud. Hence, we see expanding multiples among participants. Not only have we highlighted Altigen, but we also remain confident in any company with strategic advantages. This includes larger companies who accommodate customers of significant scale, as well as those with strong reseller partnerships. However, we feel Crexendo also provides immense long-term upside potential. Crexendo can deliver 1) operating margin 2) free cash flow and 3) an attractive valuation where others fail, sometimes on all three fronts. If our predictions manifest, the valuation becomes much more arbitrary than a discounted cash flow analysis. Another issue among industry leaders is investors need to pay handsomely for large, unprofitable businesses.

Competition and Comparable Valuation

Competition consists of numerous small companies throughout the United States and overseas as well as large telecommunication companies with revenues in the multi-hundred-million range. We remain very confident in our thesis; there is enough runway for the entire industry.

Crexendo’s largest peers have maintained double-digit growth rates for prolonged periods, setting precedent to the valuation Crexendo may deliver.

- Look below and revisit our table, notice that Crexendo is profitable while several competitors do not even turn (significant) operating margin. Altigen has been rewarded handsomely for its margin friendly business; its multiple has expanded from 1.9x sales to 2.4x in seven months. Last quarter, Altigen delivered over 20% profit margin while growing 4% year over year (cloud revenue grew ~30%).

.JPG)

- Consider again, an important fact regarding Crexendo: almost the entire quarter-over-quarter marginal increase in revenue flowed to net operating profit.

Note the potential upside for this stock. Consistent growth YoY of 20% or greater coupled with profitability will catapult valuation for Crexendo. We have already witnessed an expansion in Crexendo’s sales multiple in the last seven months from 2.7x the run rate of sales to 3.1x. The competition has also taken a leg up; the industry average has expanded from an unadjusted 4.4x revenue run rate to 5.4x since February.

If Crexendo traded for the industry average, shares would be worth $5.42.

What it seems the market has not quite priced in are profitability and value. This is understandable considering we have only witnessed two consecutive quarters of cash flow. Our research and qualitative factors of this business lead us to believe, with confidence, that cash flow will not cease. Moreover, the realization of $25 million in backlog revenue over the next four years will be converted and re-converted (in the case of recurring commitments) into a margin steady and bottom-line-expansionary business model. Finally, this company poses the same opportunities - recurring revenue and large TAM - as the largest industry players, only with less scale; but, for less scale, we earn profitability and potential growth. When the two meet in the middle, our research suggests a transformative increase in multiples. The value of the business also reflects the value of Crexendo’s contracts if Crexendo is acquired.

U.S. Cellular

Crexendo has one interesting partnership that carries great potential but comes with risk. While no one customer accounts for over 10% of revenue, Crexendo's partnership with U.S. Cellular is significant. U.S. Cellular is the fifth largest wireless telecommunications network in the United States. The partnership started in December 2017. Crexendo has kept a tight lip regarding U.S. Cellular's contribution to sales, but noted the following in response to our questions:

We don't actually break that out into segment reporting. But I will tell you that we had our strongest quarter ever with them in Q2 by far. So that was almost 3 times better than we have in any previous quarter. So we continue to see great momentum with U.S. Cellular in that relationship and lots of excitement there. And we recently started rolling out the program to their agent reseller channel and are getting great results there as well. So extremely happy with the relationship with U.S. Cellular and extremely happy with the momentum that we're getting there.

- Douglas Gaylor, August 11, 2019 Q2 Earnings Call

We dug up what limited information was our there. This article is a case study that both US Cellular and Crexendo made available. It highlights how US Cellular armed a school district with Crexendo with ease. It helps delineate some of the advantages of Crexendo and the need for these solutions.

US Cellular's recognition among wide sectors of the economy helps Crexendo emerge as a more de-facto solution. It only reiterates our theses that these schools, cities, businesses are looking for better options and cheaper options. When they turn to US Cellular, they find their way to Crexendo. Crexendo is able to tap into the cloud shift more efficiently via this large existing network. We will continue monitoring the relationship for quantitative data; for now, we see it as a young, promising area for growth.

Uplist Factor

If Crexendo begins the next few quarters like its recent history and begins its uplisting process, it will have access to a larger class of investors. The larger marketplace of institutions and investors will not shy away from the tangible data we have delineated in this report. Management has mentioned this possibility on a conference call (Q2 2019), although we cannot verify this as a certainty.

Insiders

As of March 2019, CEO Steve Mihaylo held over 10.1 million Crexendo shares and 650 thousand Crexendo warrants. The second largest insider is Todd Goergen, who owns only 360 thousand shares of Crexendo and 122 thousand warrants. These numbers have marginally changed since they were reported on March 6, 2019. Steve Mihaylo has not ceased increasing his ownership; most recently, he bought additional shares late August and early September. His owns over 70% of the company and insiders own over 77%.

About Steve Mihaylo

Crexendo CEO Steve Mihaylo founded and spearheaded the telecom provider InterTel in 1969. He grew InterTel to over $500 million in revenue before selling the business to Mitel for $732 million in 2007.

Risks

- Losing large contracts including businesses with many users can derail growth temporarily (and, possibly derail future expectations), which can further affect valuation. Currently, no one customer accounts for more than 10% of revenue.

- Credit risk associated with accounts receivable. Crexendo has experienced customers who went bankrupt in the past. Moreover, Crexendo has customers who account for significant accounts receivable.

- Crexendo uses third party manufacturing in China for hardware phones. Manufacturing, currency, and trade risk is present, especially in margin considerations.

- Credit risk increases with change to customers’ resources during systemic crises.

- There is a risk trade-off to the equity regarding large, favorable customers/contracts. Complex transactions are time consuming and expenditure of resources, even in the case of successful sale, can lead to delays in the recognition of revenue.

- Strategy risk and price, demand, and elasticity risk considerations with regard to competitor pricing and offerings is present.

- Competition risk regarding long standing or larger competitors with larger resources is present.

- Risk associated with competitors’ acquisitions that reduce pipeline of sales or consolidate number of customers.

- Competition risk from numerous small sized providers.

- Cloud security risk regarding private and sensitive data, litigation risk.

- Personnel risk regarding sales personnel.

- Partner risk regarding partner sales channels, losing a partner, failing to add partners, and expensive recruitment and training campaigns in the case of unqualified or underserving partners.

- Risk associated with the change in capital structure for the execution of strategic initiatives, namely acquisitions. Also carries risk regarding leverage.

- Risk associated with the acquisition and/or successful conversion of another company, its cash flows, and its customers.

- Risk associated with and excess sale of Crexendo shares in a thin trading market which can depress stock price substantially in such an event.

- Risk associated with the return to unprofitability, reduction in margin.

- Risk associated with lower margins including higher cost of goods, higher spend on marketing and sales, and research and development.

- Risk associated with Steve Mihaylo’s control of the company given his substantial ownership of Crexendo shares. We feel management, the CEO, and shareholders are well aligned and that this risk is minimized.

- There are low barriers to entry in this industry.

Appendix

Crexendo administers its services through desktop phones, desktop applications, and mobile devices. The following excerpt describes Crexendo products (pulled from the 10-K):

-

Business Productivity Features such as dial-by extension and name, transfer, conference, call recording, Unlimited calling to anywhere in the US and Canada, International calling, Toll free (Inbound and Outbound)

-

Individual Productivity Features such as Caller ID, Call Waiting, Last Call Return, Call Recording, Music/Message-On-Hold, Voicemail, Unified Messaging, Hot-Desking

-

Group Productivity Features such as Call Park, Call Pickup, Interactive Voice Response (IVR), Individual and Universal Paging, Corporate Directory, Multi-Party Conferencing, Group Mailboxes, Web and mobile devices based collaboration applications

-

Call Center Features such as Automated Call Distribution (ACD), Call Monitor, Whisper and Barge, Automatic Call Recording, One way call recording, Analytics

-

Advanced Unified Communication Features such as Find-Me-Follow-Me, Sequential Ring and Simultaneous Ring, Voicemail transcription

-

Mobile Features such as extension dialing, transfer and conference and seamless hand-off from WiFi to/from 3G and 4G, LTE, as well as other data services. These features are also available on CrexMo, an intelligent mobile application for iPhones and Android smartphones, as well as iPads and Android tablets

-

Traditional PBX Features such as Busy Lamp Fields, System Hold. 16-48 Port density Analog Devices

-

Expanded Desktop Device Selection such as Entry Level Phone, Executive Desktop, DECT Phone for roaming users

-

Advanced Faxing solution such as Cloud Fax (cFax) allowing customers to send and receive Faxes from their Email Clients, Mobile Phones and Desktops without having to use a Fax Machine simply by attaching a file

-

Web based online portal to administer, manage and provision the system.

-

Asynchronous communication tools like SMS/MMS, chat and document sharing to keep in pace with emerging communication trends.

Crexendo has another revenue stream from Web Services, which currently accounts for 4.57% of revenues. Here, customers pay a monthly fee to host their website on Crexendo’s data center.

* Note: Price, Upside, and Multiples have been subject to marginal changes during the report's composition.