Summary

Idea

Long

|

Catalyst

New management joins the company; Restore growth of legacy assets; Enter new growth markets.

|

Challenges

Expanding Margins; Shaking stereotypes that the company will be an unpredictable construction management type company; Managing tight labor conditions.

|

Time Frame

Will take time to play out, meaning that we can a scenario where the company loses money over the next couple quarters as it attempts to drive revenue and possibly work through the low margin inventory of its legacy business.

|

I believe that Addvantage Technologies Group, (NASDAQ:AEY) is on the cusp of meaningful revenue growth as it capitalizes on short term low hanging fruit opportunities that a new management team is quickly monetizing to drive revenue.

“AEY is a communications infrastructure services and equipment provider operating a diversified group of companies through its Wireless Infrastructure Services and Telecommunications segments.

Through its Wireless segment, Fulton Technologies provides turn-key wireless infrastructure services including the installation, modification and upgrading of equipment on communication towers and small cell sites for wireless carriers, national integrators, tower owners and major equipment manufacturers.

Through its Telecommunications segment, Nave Communications and Triton Datacom sell equipment and hardware used to acquire, distribute, and protect the communications signals carried on fiber optic, coaxial cable and wireless distribution systems. The Telecommunications segment also offers repair services focused on telecommunication equipment and recycling surplus and related obsolete telecommunications equipment.”

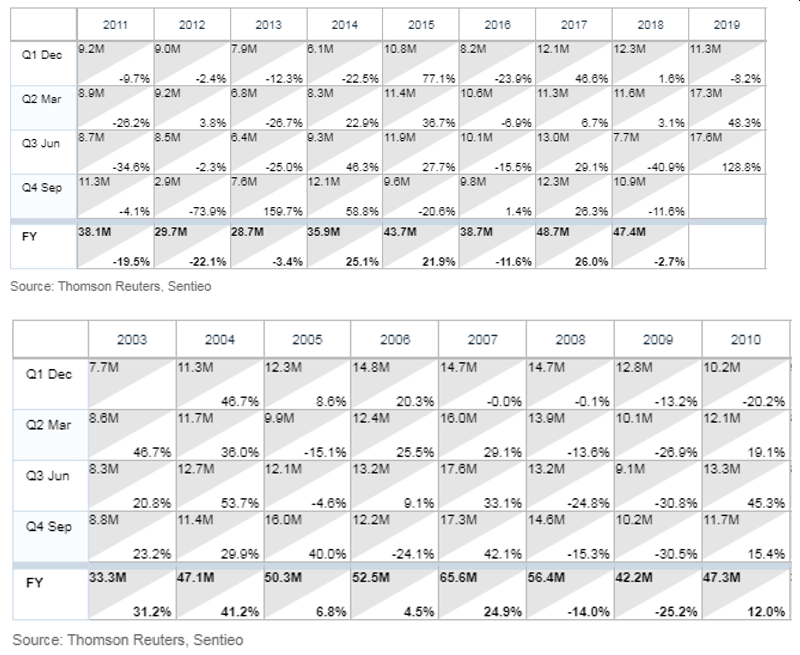

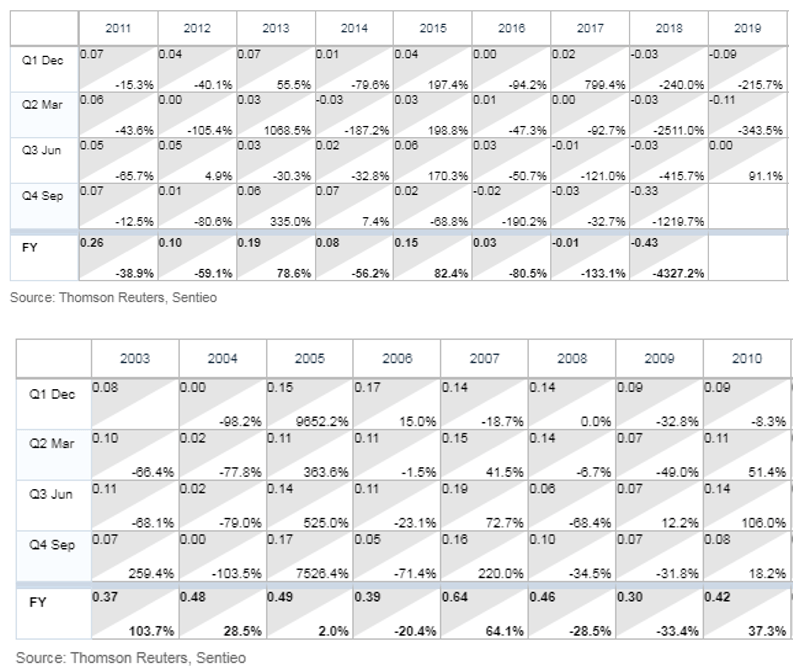

I need a little more time to determine how profits will fare as revenues accelerate. However, with shares trading near tangible book value of $1.90, a price to sales of 0.36 and an enterprise value to sales of $0.33, investors have the left company for dead because revenue and profitably have weakened significantly after revenues peaked at $65 million in 2007, and attempts by past management to revive the business have failed. Here is a look at the company’s sales and EPS history:

Sales (As we will discuss later, Q3 2019 was significant in that it was the first quarter without any contributions from the Cable segment which was sold in 2019. It is encouraging that the company’s remaining legacy assets and newly acquired assets purchased in 2019 have more than made up for lost revenue)

Revenue

EPS

EPS

This story is simple and straightforward: A new qualified management team has implemented restructuring initiatives to grow revenues and expand margins. These steps have included disposing of AEY’s underperforming legacy cable equipment assets, right-sizing the company’s telecom equipment business and recently purchasing wireless tower infrastructure assets, at a bargain price, that were ignored by its previous owners. I believe that management will be successful in restoring profitability, resulting in much higher stock prices over time. I also see a good possibility that shares could increase ahead of profitability, due to my belief that:

- Revenue growth will be healthy enough to start building investor confidence, and

- Investors will start to figure out AEY’s new role in helping all four Tier One telecom companies build out their 4G and 5G wireless tower infrastructure.

AEY is currently right around break-even. I believe that if AEY can restore telecom margins at just half of where they were 3 to 5 years ago and achieve conservative low margins on its wireless business, the company will be in position to report significant EPS as revenue growth accelerates.

Quick Facts:

- Head Quarters: Broken Arrow, Ok

- CEO: Joseph Hart

- CFO: Kevin Brown

- Number of Employees: 139

- Price - $2.10

- Insider Ownership: 57.7%

- Price/Sales of 3.6

- EV/S of 3.3

- Shares Outstanding: 10.3 million

- Market Cap: 21.7

- Need to raise capital: Low

Criteria Check List

AEY fully meets 6 out of 10 of our most important requirements for price momentum, growth and risk-based quantitative data.

|

|

Requirement

|

Comments

|

|

|

Recent 52-week High (generally within 3 months)

|

Reached 2.20 on Sept. 12, 2019

|

|

|

Strong EPS Growth Rate (Based on 2 criteria below)

|

|

| |

- > 30% EPS Growth Rate - Yes

|

3rd Qtr. 2019 loss per $0.00 vs loss of $0.03

|

|

|

- GeoPowerRanking (GPR)*; Number of consecutive quarters that EPS is expected to grow at least 20 to 30%. - TBD

|

n/a

|

|

|

10% Revenue Growth

|

3rd Qtr. 2019 revenue increased 129%.

|

|

|

Minimum Operating Cash Flow and Balance Sheet Requirements (Based on 4 criteria below)

|

As of 3rd Qtr. 2019

|

|

|

|

$571 Thousand as of 3rd Qtr. 2019

|

|

|

- Long Term Debt to Equity Ratio less than 20% - YES

|

1%

|

|

|

- Current Ratio is at least 2:1 - YES

|

2.2:1

|

|

|

- Days in receivables < 90. This shows that the company converts its account receivables to cash within 90 days. (measure of liquidity) - YES

|

32

|

|

|

Return on Equity is at least 15%

|

Negative as of Q3

|

|

|

Minimum Pre-tax Operating Margins of 8%

|

At breakeven

|

|

|

Preferably Under 50 Million Shares (Fully Diluted)

|

10.3 Million shares as of 3rd Qtr. 2019

|

|

|

High Insider Ownership (generally greater than 15%)

|

57.7%

|

|

|

Limited Institutional Ownership (generally less than 20%)

|

11.2%

|

|

|

P/E Divided by Growth Rate (Peter Lynch’s PEG Ratio) is Less Than 1.0

|

Still Losing Money

|

* See more on GeoPowerRanking

History

AEY Came public through a reverse merger in 1999 with a public entity that:

“Marketed and sold in-store advertising to national advertisers.The advertising is positioned on solar powered calculators attached to the handles of shopping carts.”

Right before the reverse merger, AEY (previous name: Advanced Media Group - AMG) was trading at around $3.00, but had reached ~$35.00 on the heels of a deal with Walmart that ended up going sour. The majority of AMG’s revenue was generated through its relationship with Walmart, who eventually elected not to extend its contract with the company.

After the reverse merger, the advertising business was eventually put to bed, with the company taking on the business and management of the merged company that sells cable equipment, Tulsat:

“Tulsat sells new, surplus, and refurbished cable television equipment throughout North America in addition to being a repair center for various cable companies. Tulsat purchases equipment from cable operators who have surplus due to either an upgrading in their systems or an overstock in their warehouse. Equipment is sold new, refurbished and “as is" to CATV operators or resellers who sell to cable T.V. operators. Throughout North America, South America, Mexico and Pacific Rim. Eventually, Tulsat also began buying new equipment from original equipment manufacturers and their resellers.

Tulsat’s revenues were about $20 million at the time of the reverse merger, reaching $65 million at its peak in 2007. Earnings per share also peaked in 2007 at $0.65. However, the cutting cord trend that began in 2010, where information and entertainment can be accessed through lower cost services delivered through antenna or the internet, has reduced consumer demand for wired cable services and thus cable equipment. The cutting of the cord has also eliminated smaller cable operators.

“Cord cutting refers to the process of cutting expensive cable connections in order to change to a low-cost TV channel subscription through over-the-air (OT) free broadcast through antenna, or over-the-top (OTT) broadcast over the Internet. Cord cutting is a growing trend that is adversely affecting the cable industry. Netflix, Inc. (NASDAQ:NFLX), Apple Inc. (NASDAQ:AAPL) and Hulu are some of the popular broadcasting services that encourage cord cutting. The cord cutting concept received a considerable amount of recognition beginning in 2010 as more Internet solutions became available. These broadcasters have convinced millions of cable and satellite subscribers to cut their cords and change to video streaming.”

As of March 2019, Tulsat’s annual sales were tracking at $16 million.

To combat the declining cable business, the company decided to stay within its core competency of selling equipment, and created a telecom division by acquiring two companies.

In 2014 the company bought Nave Communications, a 21 year old provider of used core telecommunication networking equipment that the four tier one telecom companies - At&T Inc. (NYSE:T), Verizon Communications Inc. (NYSE:VZ), Sentinelone, Inc. (NYSE:S), At&T Inc. (NYSE:T)MUS, along with lower tier companies like $ZAYO, $CTL, Crown Castle Inc. (NYSE:CCI), United States Cellular Corporat (NYSE:USM) and Everstream - purchase to build and maintain their networks. AEY management explained to me that:

“A core network’s key function is to direct data and IP signals over communication networks.”

This equipment is installed at Data Centers/Central Offices, located throughout cities that help connect wired and wireless networks.

Nave is a direct beneficiary of telecom companies upgrading and repairing their equipment as industry trends put pressure on them to improve the effectiveness of their network infrastructure.

Nave purchases its equipment from

- OEM’s selling their outdated equipment

- Telecom companies decommissioning their equipment when they are upgrading their networks

- Other resellers

- telecom companies that have excess inventory. In case you are wondering why telecom companies have excess inventories, a big reason is because they purchase equipment from OEMs in bulk to get pricing discounts.

Nave was generating about $14.0 million in annual revenue at the time of the acquisition and profitable at 6% net margins.

In 2016 AEY acquired Triton Datacom, a 15 year old provider of new and refurbished communication and networking products like VOIP desktop phones, headsets, switches and wireless routers manufactured by companies like $CSCO, Polycom, Avaya Holdings Corp. (NYSE:AVYA), Juniper Networks, Inc. (NYSE:JNPR), and Ciena Corporation (NYSE:CIEN). The bulk of Triton’s customers are private businesses building out their communication infrastructure or telecom companies that resell equipment to their private business customers. Triton is a play on private enterprises adopting unified communications solutions.

Triton was generating annual revenue of about $14 million at the time of the acquisition and profitable with 15% net margins.

Both acquisitions were expected to be “immediately accretive to earnings.” However, management failed to effectively oversee the businesses and scale them. In fact, by the end of their 2018 fiscal year this new telco division was EBITDA negative. Furthermore, the cable business continued to experience a decline in revenues.

So, Why Do I like AEY?

- • New Qualified Management

- Focusing on the low hanging fruit - Nave and Triton

- Sold the cable business

- Enters the high growth wireless infrastructure market

- Some Favorable Industry Dynamics

- Customers will continue to view purchasing and repairing used telecom equipment as a cost-effective alternative to buying new equipment, where OEMs are shortening their product cycles

- 5G rollout

- Turnaround Is Working

- In less than a year, management’s initiatives to turn the business around are already clearly evident.

- A bullish bet with downside protection

Management Team That Has What It Takes

AEY has a few moving parts, all in the telecom/wireless business. So, given the inability of past management to put the company on solid footing, it’s uniquely important that new management is deeply intertwined in the telecom space. As we pointed out in our research report on Crawford United Corporation (OOTC:CRAWA) (previous symbol HICKA), we also like it when some of the management has private equity experience.

In the case of AEY, a private equity management kicker is nice to have, since acquisitions, and in our opinion, the eventual sale of some or all of the business, is a possibility.

Together, the CEO Joseph Hart (joined the board in 2015; became interim CEO in 2018; became permanent CEO in Q1 2019) and CFO, Kevin Brown (joined the company in March 2019) fit the bill.

Mr. Hart has a long history of holding high level management positions at several telecom companies, taking on operations roles for wired and wireless projects, including spearheading AT&T in building its fiber network globally. Mr. Brown has experience across several industries and extensive private equity experience.

“Mr. Joseph E. Hart is President and Chief Executive Officer, Director of the Company since September 2018. Mr. Hart was the CEO of Aero Communications, Inc., which is a company that performs installation, maintenance, and network design and construction for the telecommunications industry. From 2006 to 2014, Mr. Hart served as the Executive Vice President of Network Infrastructure Services and Operations for Goodman Networks, Inc., a provider of end-to-end network infrastructure, professional services and field deployment to the wireless telecommunications and satellite television industry. For the previous 20 years, Mr. Hart served in various executive leadership positions for various telecommunication and wireless companies.”

“Mr. Kevin Brown is Chief Financial Officer of the company since 2019. Mr. Brown is a seasoned financial executive with extensive experience in the telecommunications industry. Since 2011, he has served as a Partner at 4M Investments ("4M"), a family office private equity investment firm. In this role he oversaw the performance and financial management of 4M's portfolio companies, including leading its telecom infrastructure investment efforts and evaluating tower, fiber, DAS and small cell opportunities. He also has served in several executive positions within 4M Investments' portfolio companies, including as Global CFO, and ultimately the CEO, of Intercomp Global Services (2011 to 2014). Intercomp Global Services grew to become the largest payroll and accounting services provider in The Commonwealth of Independent States (CIS), with over 600 employees across Russia, Ukraine and Kazakhstan. Mr. Brown led the sale and negotiations process to profitably sell the business to a private equity buyer. Prior to 4M Investments, Mr. Brown worked at M7 Aerospace LP, serving in varying levels of seniority, including as its CFO and ultimately as its CEO. He was an integral part of growing M7 Aerospace from a small aviation company into a $135 million Aerospace and Defense company with 650 employees. Mr. Brown successfully led the company to a successful sale to a strategic buyer, Elbit Systems of America. From 1998 to 2004, he worked in Strategy and Corporate Development at Crown Castle International, one of the largest telecom infrastructure businesses in the world, where he was part of the Strategy and M&A team responsible for evaluating transactions, deal sourcing and due diligence efforts globally.”

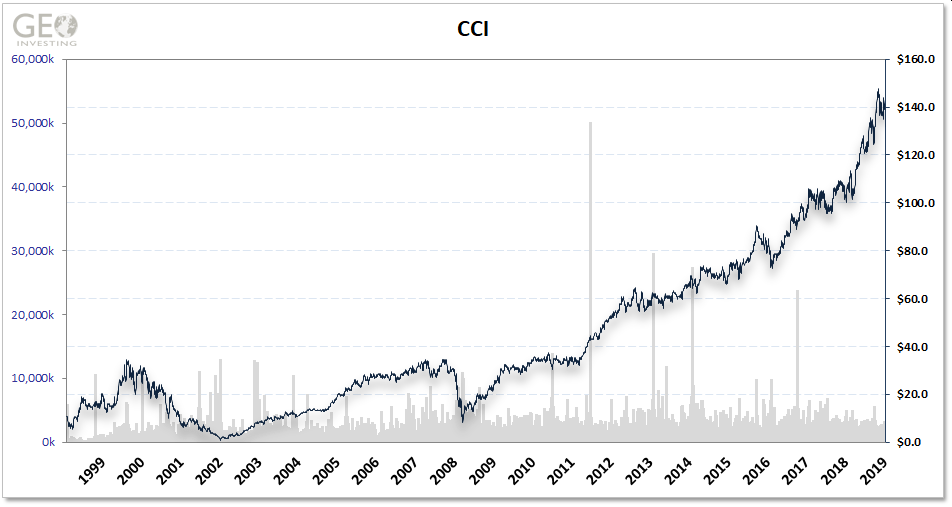

Hart first joined AEY as a Board Member, but then at the recommendation of the Board was asked to take on the role of temporary CEO to commandeer a review of all of AEY’s business units. After he was appointed permanent CEO, he sought out Brown to help execute his plan of action. AEY actually reunited Hart and Brown who had worked together the early stages the Crown Castle Inc. (NYSE:CCI) success story.

“Crown Castle is America's largest provider of shared communications infrastructure, with more than 40,000 cell towers and approximately 70,000 route miles of fiber supporting small cells and fiber solutions across every major U.S. market.”

Brown was actually involved with bringing CCI public in August 1998, while Hart joined the company soon after. During their tenure at CCI, the stock reached a $1 billion market capitalization and has continued to perform well:

Hart felt that the new direction AEY had to take was clear:

Feasting on Low Hanging Fruit - Getting Telco Ready for Growth

Hart’s first order of business was to make changes at Nave and Triton Datacom to put them on a path to grow revenue at improved margins. Both companies have been around for a long time and have cultivated deep customer relationships, but had reached a growth bottleneck that AEY’s past management could not loosen.

Nave

In the case of Nave, management concluded that the company’s inventory controls were, well…out of control. Nave was not tracking or analyzing inventory very well, which effected its ability gauge important inventory metrics and, in some instances, made it extremely challenging to locate products stored in the warehouse. Furthermore, Nave did not have capability to test equipment before shipping orders to customers. Finally, it was not offering high margin equipment repair services to its customers. The end result was a poor-quality product and poor customer satisfaction. To be fair, Nave was very good at procuring and buying equipment.

After a thorough review, management chose to outsource most of Nave’s operations to a reputable firm that specializes in areas where Nave was lacking, Palco Telecom.

“PALCO’s professionals specialize in transforming the increasingly complex Post-Sales Support, Integration, and Manufacturing Support Service processes into a competitive advantage for our clients. PALCO utilizes a best-of-breed approach utilizing existing processes developed via innovation and exhaustive research in our support of many of the fortune 500 as well as injecting tailored process models to deliver best-in-class post-sales customer experience performance.”

Palco also conducts testing and repair services. The testing aspect is a big deal, since it allows Nave to certify that it is selling products that work, which can help Nave expand its margins. Furthermore, repair services are a big source of demand in the telecom industry and carry high margins. Partnering with Palco has also removed a significant amount of annual costs from Nave.

Nave now only procures inventory and markets and sells products, while Palco inspects, tests, packages and ships products.

"Effective immediately, Nave inventory management and order fulfillment will move to Palco Telecom, a world-class third-party 3PL reverse logistics provider in Huntsville, AL. This move will allow Nave to begin serving a much wider geographic customer base, opening up additional sales and revenue opportunities. The movement of inventory and order fulfillment operations will also streamline operations to improve inventory efficiencies and shipping time while significantly reducing operating costs.

Most of the existing leased 90,000 sq. ft. Nave warehouse and operations facility in suburban Baltimore will be sublet to further reduce operating costs. ADDvantage will reduce the Nave workforce in Baltimore by 15 employees.

I am pleased to announce we are investing in equipment to provide product repair services to our customers, and that we plan for service to be a contributor to our revenue in 2019. We are also improving our testing capabilities in response to increased customer and industry demand for higher quality products."

Essentially, Nave does what it does best and lets Palco do what they do best.

Here is a summary of the changes that occurred at Nave as outlined in its SEC filings:

“As a result of an internal operational review, we determined that our overhead costs were too high relative our top-line revenue and the location of our facility was hindering our ability to serve our customers in the western part of the US. Therefore, in September 2018, we moved our operations from Baltimore, Maryland to a third party reverse logistics partner, Palco Telecom (“Palco”), located in Huntsville, Alabama. We incurred restructuring charges of $0.9 million in fiscal year 2018 as a result of moving our operation to Palco. However, this strategic move should provide, among other things, the following immediate and planned future benefits:

- Warehousing and inventory fulfillment cost savings – As a result of moving the operations to Alabama, we anticipate that we should generate operating cost savings in excess of $1 million per year due to lower facilities, payroll and overhead costs. Since Palco’s expertise is logistics, their systems and processes should improve Nave’s inventory storage and efficiency of fulfillment of inventory orders, which will in turn allow Nave to better serve its customers.

- Inventory certification – Palco has the in-house ability to test and repair telecommunication parts. Nave plans to implement a process in 2019 to offer customers certified telecommunication parts with enhanced warranties in response to increased customer and industry demand for higher-quality products. In order to implement this process, Nave will be making additional investments in test equipment to be housed in Palco’s facilities. Although Nave will incur additional costs to certify its inventory, we believe this change will provide increased top-line revenues as well as improving our brand quality. We intend to add additional sales personnel as necessary to support this demand.

- Geography – Nave’s operations were located on the east coast in Baltimore, which we believe negatively impacted our ability to be competitive in the western US due to inventory shipment delivery times. Subsequent to the move to Palco, our inventory fulfillment operation will now be in Alabama, which will significantly improve delivery times across the US, which will allow Nave to increase its customer base across more geographic areas of the US.

- Repair – Today, Nave cannot repair telecommunications products internally and generally does not offer repair services as a product line to its customers. With the move to Palco and our investment in test equipment, Nave plans to begin offering customers repair services in late 2019. We believe that this product offering will generate increased top-line revenue and profitability for Nave.

In summary, we believe that this operational move of our warehousing and inventory fulfillment operations to Palco should provide many efficiencies in our inventory processes and operating cost savings as well as provide better quality products to our customers. This strategic move should also allow Nave to expand its US customer base to the western US as well as offer additional product lines. All of these factors should not only increase Nave’s top-line revenue, but also its bottom line profitability.” 2019 10K, Page 11

Triton Datacom

While Nave’s issues spanned across most aspects of its business, Triton’s centered mainly around one problem: not taking steps to grow out of its overcrowded manufacturing facility to efficiently operate, expand its higher margin refurbishment business and enter new markets.

Triton sells new and refurbished equipment. However, at 30%, the gross margins on selling refurbished equipment are significantly higher than selling new equipment, which carry about 20% gross margins. Apparently, the legacy facility was inefficient located in a condo type office complex with no single dedicated area with capacity to store inventory. In other words, the company owned office space scattered around the complex. In the end, the company could not accommodate growth in the refurbished business. So, over the last few months, management has been moving Triton operations from an 8,500 square foot facility to a new nearby 24,000 square foot facility. Better inventory management will allow the company to take advantage of selling products on-line, like through Amazon Prime, where the company has to guarantee 48-hour delivery.

Here is a summary of the changes that occurred at Triton as outlined in SEC filings:

As a result of an internal operational review, we determined that our current facility was hindering our ability to perform efficiently as well as not allowing us to grow this business. In addition, we identified product lines that we needed to stock in order to increase revenues and reach a broader customer base. Therefore, in fiscal year 2019, we are planning to move our operation to a new location in a similar area. Once this strategic move is completed, it will provide us the following benefits:

- Operational efficiencies – The new facility will allow us to refurbish more customer premise units per person and will also allow us to expand our models that we refurbish. Currently, we primarily focus on the refurbishment of Cisco IP desk phones, but we will now plan to add additional assembly lines to focus on additional manufacturers that our customers are requesting.

- Investment in additional new and refurbished inventory ‒ Increasing the footprint of our warehouse and adding additional storage height will allow us the opportunity to invest in additional inventory. This will include the addition of new manufactures as well as increased quantities of current inventory to fulfill customer demand.

- Wholesale broker-to-broker sales expansion – As a result of the investment in additional new and refurbished inventory, we plan to expand our brokerage service team and to expand our broker sales platforms.

- Carrier customers – The new facility will provide the footprint space required to expand our focus into the telephone carrier market, which we do not currently support. Therefore, as we expand our product line offerings discussed above, we plan to begin marketing to the telephone carrier market in late 2019.

In summary, we believe that the move of our facility in 2019 and investing in additional inventory product lines across multiple manufacturers should provide the platform for us to grow Triton’s top-line revenues and improve its overall bottom-line results. 2019 10K, Page 12

Sell the Cable Business

New management had also set a goal to sell the declining cable business. So, on December 4, 2018, AEY sold one of its cable properties to David Chymiak, LLC, a company controlled by David Chymiak, the Company’s Chief Technology Officer, director and a substantial shareholder. Chymiak was one of the original founders of Tulsat (cable business

Then, on June 30, 2019 AEY sold the rest of its cable assets to Leveling 8, Inc, a company owned 100% by Chymiak, for an aggregate of $3.9 million in cash plus another $6.4 million 5-year promissory note bearing an interest rate at 6% per annum.

To summarize:

- Cable TV segment’s Broken Arrow, Oklahoma facility sold for $5.0 million in cash in December 2018

- The rest of Cable TV segment business sold for $3.9 million in cash $6.4 million 5-year promissory note (with an annual interest rate of 6%) in July 2019

These moves helped AEY pay down all of its long-term debt and put the company back in compliance with covenants associated with its line of credit.

Enter High Growth Telecom Markets

New management wanted to enter wireless service communication markets, such as wireless tower construction services for Tier One wireless operators. Actually, old management had made failed attempts at this goal due to partnering with a company that didn’t have the capability to grow the business.

Barriers to entry in developing relationships with the top 4 carriers that own 95% of the telecom industry revenue are high, which is why AEY pounced on the chance to purchase two underperforming tower infrastructure assets (Fulton Technologies and Mill City), now called Fulton, from a private equity firm, Resilience Capital.

“One of the key attractions of acquiring Fulton is that it had existing contracts and customer relationships. Fulton is an approved vendor with the four major U.S. wireless carriers, leading communication tower companies, national integrators, and major equipment manufacturers. The acquisition allowed us to enter the wireless communication space quickly and cost effectively. The customer contracts that Fulton has eliminated a key barrier for us to enter this industry due to the required experience and safety qualifications necessary to obtain the contracts.”

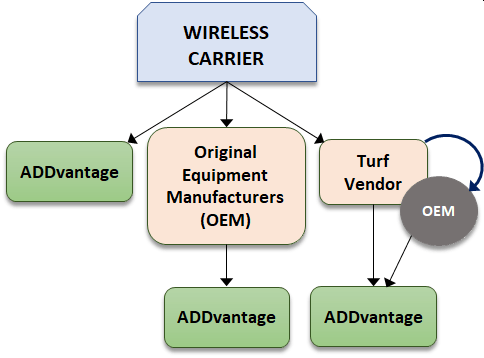

Fulton provides two basic services to wireless carriers. The lion’s share of its revenue comes from managing the installation, upgrades and maintenance of equipment on existing wireless towers. Fulton procures/buys materials (generic material common to most towers), manages the equipment (carrier specific equipment provided by carries and/OEMs/turf vendors), hires the labor, manages the labor and oversees the installation and commission of equipment. Business originates from multi-year Master Service Agreements (MSAs) with wireless carriers, OEMs, turf vendors or a combination. Turf vendors (who are sometimes also OEMs) manage projects that have been awarded to them by wireless carriers or OEMs that have been awarded a project. Mastec, Inc. (NYSE:MTZ) Is an example of a turf vendor. In some instances, a carrier will deal directly with AEY. In this case, the carrier has purchased equipment from OEMs, like Nokia Corporation Sponsored (NYSE:NOK) and Ericsson (NASDAQ:ERIC), that an AEY will use to complete the project. In other instances, the wireless carrier will transfer the project to OEMs and turf vendors, in which case AEY has MSAs in place from the requisite OEM and/or turf vendor.

AEY currently conducts a substantial amount of business with AT&T, who tends to farm out projects to OEM’s and turf vendors. That being the case, AEY would still like to increase the amount of work it gets directly from AT&T, since this would benefit margins. However, a bigger opportunity lies in targeting carriers that tend to lay off less of their wireless infrastructure work to OEMs and turf vendors.

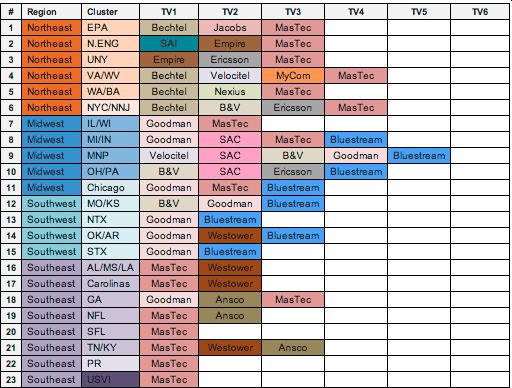

“Unlike Verizon Wireless, which assigns a network manager to each part of the country, AT&T contracts with wireless infrastructure specialists to build and upgrade its network.

These contractors are known in the industry as “turf vendors” because they have responsibility for different geographic regions. Some are multinational construction giants like Bechtel and Black & Veatch, while others are regional firms dedicated to telecom and wireless.”

Please note that AEY usually has multi-year MSAs in place before projects are deployed.

A smaller piece of Fulton’s revenue comes from temporary tower deployment:

Mobile cell sites are transportable on trucks, allowing fast and easy installation in restricted spaces. Their use is strategic for the rapid expansion of cellular networks putting into service point-to-point radio connections, as well as supporting sudden increases of mobile traffic in case of extraordinary events (trade fairs, sports events and concerts, emergencies, catastrophic events, etc.). Mobile cell sites require neither civil works nor foundations, just minimal requirements like commercial power and grounding. The mobile units have been designed to be a temporary solution, but if requested, they can be transformed into a permanent station.

Even though AEY had to infuse some working capital into Fulton, the $1.7 million ($1.3 after post-closing adjustments) AEY paid for Fulton appears to be a steal. It appears Fulton was on track to generate annual revenue of $16 million at the time of the acquisition. Over the years, Resilience had levered up to acquire several telephone businesses and decided to exit their positions at the funds end of life. Resilience easily sold off the larger businesses. According to the company, Fulton and Mill City were the smaller portfolio positions left with a fund that needed to be sold. Hart had actually worked with Fulton in the past, so he knew it had potential. Furthermore, Hart worked at one of Fulton’s highly successful billion-dollar customers, Goodman Networks, for eight years.

We also see some potential synergies between Fulton and Nave. Wireless carriers are Fulton’s major customers, creating a source of used equipment and recycling opportunities for Nave. A future opportunity exists for Nave to enter the wireless equipment industry by reselling used equipment it has access to when Fulton upgrades and/or decommissions wireless tower sites.

Industry

Fulton

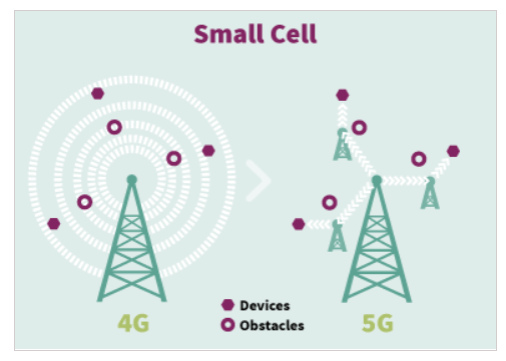

When you look at the industries that AEY participates in, it's easy to conclude that its wireless tower infrastructure business clearly has the most upside. Regardless of the hype, we can't ignore that 5G is here. Even though consumers won't see the benefits of 5G heading into 2020, 2020 will be the year that wireless telecom companies like AT&T start to accelerate their build-out of their 5G infrastructure. Around 30 States have already enacted regulation to help support the build-out of 5G. The infrastructure needs do not only include wireless towers, but also small cells that are needed to connect 5G networks, related equipment and equipment at the business level.

Source: https://www.infineon.com/cms/en/discoveries/mobile-communication-5g/

“Based on the communication infrastructure, small cells are expected to grow at a significant market share during the forecast period. Small cells are low-powered portable base stations that can be placed throughout cities. Carriers can install many small cells to form a dense, multifaceted infrastructure. Small cells' low-profile antennas make them unobtrusive, but their sheer numbers make them difficult to set up in rural areas.”

It certainly seems that AEY is getting involved in this industry at a pretty serious inflection point. The market is expected to grow exponentially for years to come, and the ball is going to be in AEY’s court. In fact, the 5G infrastructure market is expected to experience a crazy CAGR of around 70%, between 2019 and 2025, with most of the growth occurring in North America.

While 5G definitely adds some pizazz to the story, it's not just 5G that is driving the wireless infrastructure build out.

“The bottom line: 5G is indeed exciting, but 4G will be paying the bills for the next several years.”

The current infrastructure needs to expand to meet the demands of all the information and services being consumed. With or without 5G, wireless operators are going to have to upgrade their infrastructure to be able to handle stresses on their current networks and improve performance. Furthermore, 5G operates on different frequencies then 4G and has a much more narrow coverage area, which means 4G will need to fill the gaps where 5G is unavailable. This is similar to how 4G and 3G work together. Furthermore, telecom companies have not utilized all their 4G capacity and more spectrum will be made available for 4G, which will require field work.

“Carriers seek to address increasing mobile traffic demands and the expectation of 24/7 connectivity. As more and more devices require a wireless connection to operate, technology needs to rapidly improve to accommodate these needs. 5G promises to withstand the connectivity demands of the future and current wireless infrastructure needs to be upgraded to grow hand in hand with advances in wireless technology.”

“The carriers are going to continue to deploy their existing spectrum and future 4G spectrum that will continue to justify investment as they try to increase capacity and coverage in 4G where they can realistically make money.”

Regardless, it's clear that wireless carriers will be upgrading their infrastructure at an accelerated pace for years to come.

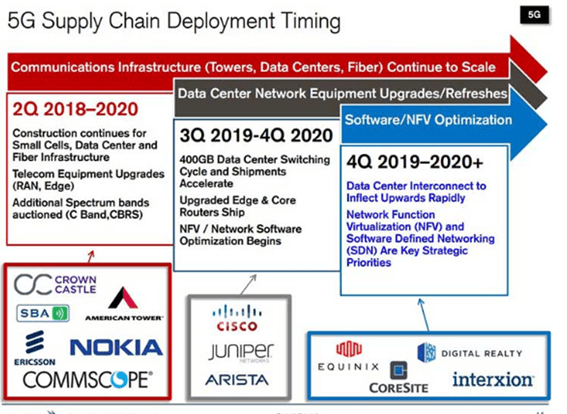

This following detailed infographic depicts some the phases related to 5G deployment:

Nave and Triton

I could not get a great read on the industry growth rates of the markets that Nave and Triton serve.

As a reminder, Nave sells used networking equipment to telecom companies and now, with the help of Palco, can offer test & repair services. Triton sells new, used and refurbished equipment to private businesses. Even though the telecom equipment industry and many of its segments are expected to grow less than 5% per year, reasons exist to believe the AEY’s telco segment can grow at a healthy clip for the next few years.

Companies repair their telecom equipment for a variety of reasons. Just because equipment breaks, it does not mean they will want to buy the same new equipment or upgrade to more expensive equipment. Sometimes equipment that a company may own is still very essential and useful to their networks, so it makes sense to repair broken equipment or buy similar used equipment.

Moreover, after certain amount of time OEMs do not support old equipment since they want to push higher margin new equipment. This is magnified by the fact that OEM product replacement cycles are shortening. Customers can extend the lifecycle of products/platforms/services from either repairing their own equipment or buying refurbished equipment at lower prices. According to International Data Corporation, the secondary telecom equipment industry is about a $4.5 billion industry, with the repair segment standing at about $750 million.

“One large player dominates the repair segment, with the rest of the market being comprised of smaller players with revenue under $10M, each comprising less than 3% of the market.”

So, at a combined current annual revenue run-rate of $32 million, Nave and Triton have plenty of room to capture market share to and gain pricing power in a very competitive environment.

Overall, I think Nave and Triton are sitting in a nice spot. The way consumers and enterprises stay connected and communicate is rapidly evolving. For example, enterprises are quickly adopting cloud communication platforms, which bodes well for Triton that sells related equipment:

New Management’s Plan Is Quickly Bearing Fruit

Given the problems Nave and Triton were experiencing, it’s encouraging that both were able to basically maintain sales near levels at which they were acquired. This indicates that the businesses are probably respected players in their markets. More importantly, the progress that the new management regime has accomplished after they began their tenure in July of 2018 is extremely encouraging. The company's 2019 third quarter report ended June 30 shows that the moves management has taken to position the company for profitable growth are already evident:

- Q3 sales rose 129% to $17.6 million

- Adjusted EPS improved to a loss of 1 cent from a loss of 7 cents (eliminates the cable business contribution and acquisition costs associated with the Fulton acquisition).

Breaking out the segments

Nave's revenue for the third quarter was $4.9 million, easily putting it in track to exceed an annual revenue run-rate of $14 million, the same run-rate as when AEY originally purchased the company. Triton’s revenue came in at $3.9 million, similar levels where revenues were at the time it was acquired.

Furthermore, the Telco segment was slightly EBITDA positive for the quarter, reversing a prior year loss. We must note, however, that with a combined EBITDA margin of 5.4% for the quarter, Nave and Triton still have a long way to march towards where they were at the time they were acquired.

During the 2019 third quarter, Fulton's revenue rose 102% to $8.7 million, its first full quarter of contribution to AEY, and is right at breakeven. This puts Fulton on an annual revenue run-rate of $34.8 million, easily exceeding the pre-acquisition run-rate.

We should begin to get a glimpse of what the new Triton looks like once their move into its new facility is completed, but given what management has already accomplished with Nave and Fulton, I'm very optimistic Triton’s performance will quickly improve.

To summarize:

- The annual revenue run-rate of the Telco segment as of Q3 2019 was around $32.0 million, compared to actual annual revenue of $24.6 million in 2018.

- Fulton sports an annual revenue run-rate of around $36.0 million, compared to around $16.0 million immediately prior to it being acquired. (Although, Fulton’s revenue is subject to seasonality due to weather).

- AEY’s combined annual revenue run-rate is now around $70.0 million.

Valuation

We will probably still need to wait a few quarters to start valuing the company on potential earnings. Until then, given the company’s tangible book value per share is $1.90, combined with a P/S of 0.36 and EV/S of $0.33, I think AEY is a great bet, being that is it currently being priced to fail.

I'm not a huge fan of valuing stocks in most industries using book value per share. Dying companies can fall below book as cash balances dwindle and aging nonproductive assets fail to deliver attractive ROIs. But it can serve as a floor in turnarounds when the opportunity for unlocking value or growth exists. If you are right, shares will eventually trade at multiples of book as growth begins to dominate valuation. It's also worth noting that Fulton is recorded at $1.3 million on the books, the post-adjusted acquisition price. However, I think that is worth a lot more based on its Q3 revenue performance.

In situations like AEY, I like to have fun playing around with some assumptions. Here is a table that breaks down revenue and EPS by segment, using Q3 2019 revenue run-rates and conservative margin assumptions:

|

Segment

|

Revenue

|

Net Margins (1,2)

|

EPS (4)

|

P/E

|

|

Nave

|

$20M

|

3%

|

$0.06

|

|

|

Triton

|

$12M

|

7.5%

|

$0.09

|

|

|

Fulton

|

$36M

|

3%

|

$0.108

|

|

|

TOTAL

|

$68M

|

3.8% (3)

|

$0.26

|

~8x

|

Notes1,2,3 - Margin Assumptions:

- Nave: 3% (50% of the net income margin at time of acquisition)

Triton: 7.5% (50% of the net income margin at time of acquisition)

Fulton: 3% (typical low construction/infrastructure company)

- Total: Weighted Average

Note 4 - Shares outstanding = 10M

To be clear, peak margins will not occur until higher revenues are attained. It’s also probably unreasonable to use Nave and Triton’s pre-acquisition margins due to their markets being more competitive and to the costs associated with being a public company. Furthermore, AEY will probably have to deploy higher amounts of capital to grow their revenue and a bigger focus on on-line revenue at Triton will limit margin expansion due to the associated marketing and transaction costs. That is why I used a margin level of 50% of pre-acquisition margins. Regardless, it’s fair to assume that margins are not anywhere near their peak potential, given that the company appears to be in the early phases of a multi-period sales and profit margin recovery period. Furthermore, Nave margins could have some upside past my assumption, since it can now start selling higher margin refurbished equipment. Also, I didn’t even factor in any top line growth assumption.

Regarding Fulton, the company is going to have some gross margin stability, due to its cost structure and asset light characteristics. This advantage exists because a good deal of equipment used in projects is provided to Fulton by the wireless carriers, OEMs and turf vendors. So, my margin assumption may be too low.

Caveats

- With the high the growth that comes with 5G, so too will the undersupply of skilled labor which could pressure AEY’s margins. This is where I see the biggest risk.

- There may be challenges in managing personnel and margins as Fulton attempts to meet the high demand for its services.

- Fulton will be viewed as a low margin project-based construction company. However, the wireless infrastructure growth rate is so robust that I don’t see it this way. Quite the opposite is true; I view the business as very repeatable for some time. It would be nice if it could pursue some recurring or repeatable maintenance and service business.

- Telecom companies and wireless carriers are known to sporadically delay infrastructure spend.

- Revenue lumpiness due to weather constraints

- I am confident that AEY will experience healthy revenue growth, but I don’t have a complete read on the margin profile of all the business segments.

- Interruptions in growth at Triton might be a concern if the transition away from handsets and related hardware occurs faster than the company anticipates. (Most of Triton’s revenue is from phone hardware-related sales).

Regarding the last caveat, there will continue to be a need for equipment, even as technology changes. A key to Triton’s and Nave’s success will be how well they manage inventory to evolve with changes. I posed my concerns about the Triton caveat to management. Here are their answers:

- Connection to the internet is not going to be replaced. There is a need for refurbished switches and other equipment secured on their network. As technologies evolve, so will their business. The products will just change. They will aim to follow the technology and learn how to refurbish.

- VOIP services are much less expensive then cell phone service for each employee.

- Many offices want phones at every desk vs. for every employee. Think of mid/lower level office employees at companies. Everyone needs to be able to communicate and companies want them to do so over their own network. They want the connectivity between phones on their network with built-in extensions to make it easy to find people and communicate.

- We don’t believe companies will not hand out cell phones to most employees. This only happens in higher level professional settings. They are expensive, get dropped/damaged easily and are difficult to manage and recover when the employee leaves.

- Desk phones are getting smarter and smarter, allowing them to hand off to personal cell phones, tie into CRM systems and communicate with employee networks.