By Maj Soueidan, Co-founder, GeoInvesting

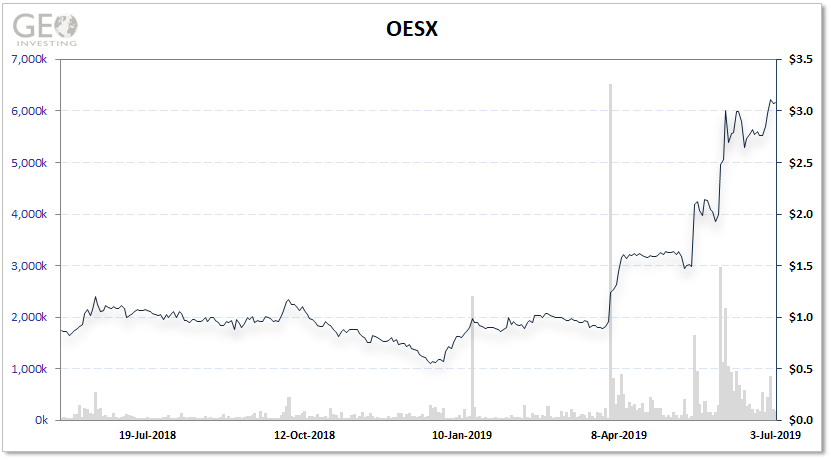

On June 7, 2019 we disclosed that we initiated a long position in Orion Energy Systems, Inc. (NASDAQ:OESX) at $3.00, stating we think the stock has a chance of approaching $5.00. This decision was based upon my interview with OESX management at the 2019 LD Micro conference which we published on June 13, 2019.

Before meeting management, if you asked me if I would be excited about buying a lighting solution company, I would have told you that I have no interest, at all. Where is the growth in that? Furthermore, in July 2015 we were lucky to lock in a quick 60% gain in a bullish Call to Action on shares of Energy Focus, Inc. (NASDAQ:EFOI), a lighting technology company that we rode from $5.80 to $9.89 that reached a high of $29.20. The stock eventually imploded due to one-time large project revenues not being replenished and lack of diversified customer base. But now I understand why some investors are bullish on the growth prospects of OESX, at least in the near-term. With new management, a large diversified legacy customer base and a recently awarded large contract from a new customer, the company has the opportunity to benefit from new trends taking place in the enterprise lighting industry that are adding some excitement to what many might consider a “boring” industry.

These passages from Allied Market Research and Navigant Research say it all:

“Lighting consumes approximately 15% of total global power consumption. Moreover, lights produce around 5% of global carbon emission. Thus, the United Nations Environment Programme (UNEP) has released certain guidelines on energy-saving lighting solutions to reduce carbon emissions. With rapid urbanization and rapid economic growth, the lighting industry is expected to grow exponentially over the next two decades, resulting in more high demand for LED based lighting. Thus, need for more LED-based lighting for effective energy saving and cost saving is expected to drive the Industrial and commercial LED lighting market growth in the coming years.”

“Lighting controls were originally designed for dimming or daylighting, but they have evolved beyond those original functions to include space utilization, conference room management, increased employee productivity, and improved operational efficiency by removing labor required by facility managers or other building personnel. The evolution from an intelligent lighting control system toward an IoT lighting system has occurred in large part because of the easy use of sensors as a host for IoT applications. According to Navigant Research, global market revenue for IoT lighting is expected to grow from $651.1 million in 2017 to $4.5 billion in 2026.”

OESX has stated that the large new contract puts the company on track to attain fiscal 2020 revenues of $135 to $145 million and EBITDA margins of at least 10% (year ends March 31). We calculate that this guidance would translate into earnings per share of $0.40, which is above analyst estimates of $0.33. This compares to revenues of $65.8 million in in fiscal 2019 and a loss of 23 cents per share. The stock has responded nicely since the announcement of the contract.

Still, a less than optimal aspect of the OESX bull case is that it operates a project-based business, meaning that quarterly and annual revenue can experience noticeable lumpiness. So, from a valuation point of view, it is fairly important for OESX to accelerate contract wins from new and/or legacy customers, as well as receive add-on work related to the recent large project win. Although the company has not disclosed the identity of the new customer, we are trying to track down leads as to who this might be. It’s worth noting that management has been buying shares into the stock’s recent runup.

We have already published our notes on OESX from our LD visit, but I wanted to provide a little more detail on the company, as a result of a follow up interview I had with management.

History and Understanding the Business

QUICK STATS

- Market Cap: $90.9 Million

- Shares outstanding: 29.9 million

- TTM revenues (fiscal 2019): $65.75 [or $66.8] million

- Analyst 2020 revenue estimate for 2020: $139.9 million (consensus)

- TTM loss per share: $0.23 (fiscal 2019)

- Analyst EPS estimate for 2020: $0.33 (consensus)

- Current ratio: 1.5

- Total debt: $9.3 million

- Book value: $0.61

The company was founded in 1996 to provide fluorescent lighting retrofit solutions to enterprise customers and completed its initial public offering in December 2007. OESX has a 200 square foot manufacturing facility at its headquarters in Wisconsin (with ample capacity) and an office in Jacksonville FL. For those of you who may not be familiar with the meaning of an enterprise customer, it just means a commercial/industrial business. Retrofit refers to activities related to upgrading lighting technology and fixtures in existing buildings or industrial settings, like hospitals, military facilities, parking garages, warehouses and retail spaces.

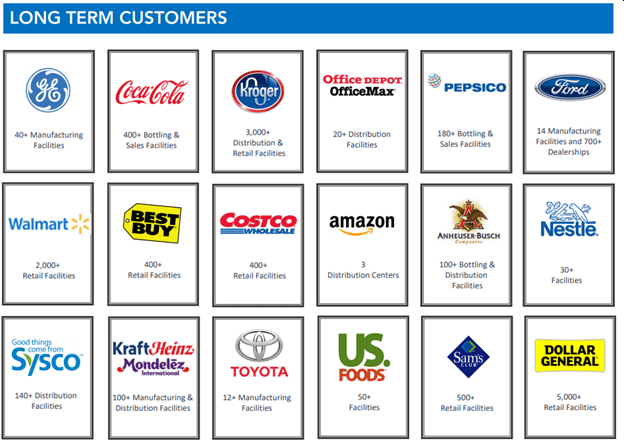

The company has done business with approximately 40% of Fortune 500 companies and its customer base includes some of the most recognizable businesses, including:

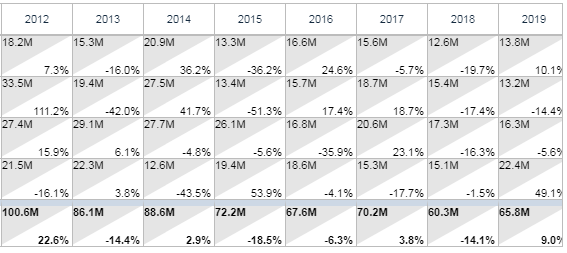

OESX initially experienced rapid growth, with annual sales rising in a straight line to $81 million in 2008, peaking at $100 million in 2012, before falling to its recent level of around $60 million. Then in 2013, the company acquired a Jacksonville Florida based company, Harris lighting solutions, to expand its customer base and product offering, but sales still did not gain traction. As the following table shows, the company did not really grow revenue since going public and spent most of the time losing money:

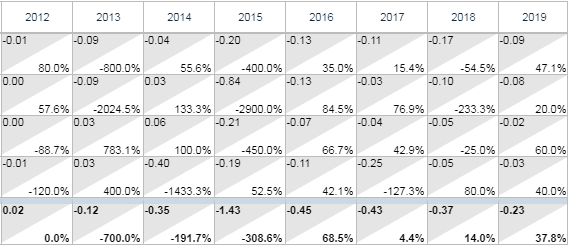

Sales:

EPS:

New CEO Takes Over

The current CEO, Mike Altschaefl, joined the company as Chairman of the Board in 2009 and was appointed to CEO in 2017 when it became apparent that the then current management regime was not getting the job done. Mr. Altschaefl has extensive experience running large companies.

Some of the problems included:

- Being about two years late in adopting LED lighting solutions (as pointed out in our prior research)

- Bloated cost structure due to excessive board and executive compensation, ineffective marketing campaigns and overinvesting in the legacy florescent lighting business

- Subpar sales and marketing process

So, management took steps to put the company back on solid footing. OESX started to offer LED products between 2012 and 2014 but was not experiencing the desired traction. In 2017, under tenure of new management, Orion rightsized the company’s cost structure by consolidating locations, resolving some lingering legal issues of the business and ending poorly performing marketing initiatives. These moves helped to eliminate around $6 million in costs. Revenue growth was also challenged by industry dynamics that caused average selling prices to fall, a situation that management believes has stabilized. Although OESX lost money in fiscal 2019, the company began reaping the benefits of its restructuring moves in the second half of 2019 where the company turned EBITDA positive.

However, I am most excited about:

- changes OESX made to its sales channel that added another avenue to reach new customers and

- its commitment to lean on its competitive advantages.

Sales Channels

Traditionally, the company sold its product through two channels:

- Direct selling product to the end user, while providing lighting fixture construction/installation management services - 47% of revenue

- Selling products to Energy Service Companies (electricians) who sell and install product to/for their own customers - 36% of revenue

In 2016, OESX began selling through what it calls “Agent Driven Distributors” who sell products to Energy Service Companies. OESX now has relationships with 50 agencies across the country that represents about 17% of revenue.

Competitive Advantages

OESX Is building on its strengths as a one stop shop for customers it deals with through its direct consumer channel. And it’s paying off for the company. This passage from the 2019 10K cites the company’s turnkey solution as the primary reason it was awarded the recent large contract:

“These turnkey services were the principal reason we obtained our $110 million revenue commitment to retrofit multiple locations for a major national account customer.”

A hidden opportunity arising from this win is that OESX has identified companies that could use similar solutions that OESX designed for this new account.

I love companies that offer total solutions to their customers. If you are a long-time GeoInvesting Premium Member, you probably already know this. This tends to lead to sticky customer relationships and creates pricing power. It’s also something I talked about in our bullish Tss, Inc. (NASDAQ:TSSI) research article published in September 2017.

The turnkey solution includes:

- OESX engineers visit a customer’s location to assess the environment with the customers engineers

- OESX Quickly delivers an assessment report, which includes a financial and cost benefit analysis

- OESX Designs a customized solution

- OESX Manufactures and delivers the product within 10 days, on time 99% of the time.

- OESX Leans on its technology partners to install IoT solutions into its fixtures

- OESX manages the installation of product (installations are performed by electrical subcontractors that the company works closely with).

A nice take away I received from further research is that the company has 104 patents and 15 more in the pipeline. Furthermore, according to management, OESX not only has one of the most complete solutions compared to its competition but also has THE most efficient lighting solution.

Industry at A Glimpse:

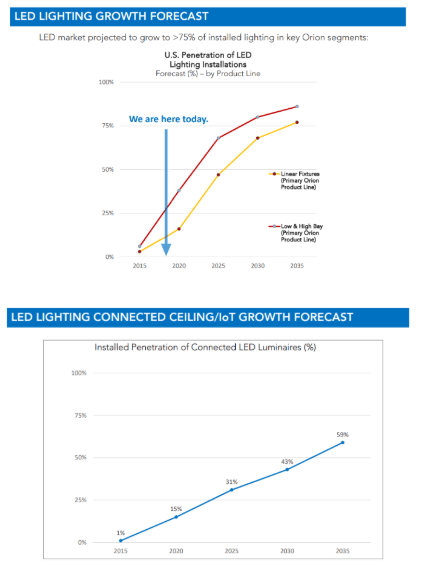

Recall that our June 13, 2019 research note highlighted a chart showing that LED adoption is still in its very early stages:

Here are some reasons to support the case for LED and why investing in companies offering LED lighting solutions may not be as boring as you might have initially assumed.

The obvious benefit of LED is a 40% to 50% cost reduction outcome compared to other sources of unnatural light. Additionally, up to an 80% direct cost savings can arise from adopting IoT applications that LED lighting solutions allow for, such as regulating lighting use through motion control and tracking assets. I don’t know about you, but I had not connected the dots between lighting solutions and IoT. But, apparently it’s the perfect marriage:

“Generally, but especially for industrial locations, lighting is the ideal entry point for IoT data,” said Jamie Britnell, Director of Product Marketing – Lighting, Synapse Wireless (www.synapsewireless.com). “Because all these facilities incorporate lighting, an IoT communication network grid is essentially installed as part of an LED retrofit or in new construction. With this network in place, compatible sensors can be distributed through the facility to monitor various equipment and processes.”

Here are two examples of how IoT solutions are applied through LED solutions:

- “Dubbed Track & Trace and using its established Einstone Bluetooth beacons embedded in the luminaires, the system can monitor resources in real time and additionally provide data about movement and usage.”

- “Using a hospital as an example, Osram says medical equipment such as ultrasounds and portable ECG machines can be tracked in real time on an analytics dashboard. In order to be able to track assets, miniature radio transmitters called beacons are integrated into the lighting infrastructure. These form a Bluetooth Low Energy mesh network by means of which data can be transmitted and received.

The assets to be tracked are equipped with ‘asset beacons’ that also send out signals via Bluetooth. This signal data is transmitted via the mesh network and passed on to a gateway.

Analysis of the data allows the locations of the objects to be calculated and displayed on a user’s dashboard. In addition to identifying asset locations, it’s also possible to create heat maps or analyses of tool utilization, and perform temperature monitoring for sensitive objects.”

The quality of a lighting solution can also have an indirect benefit to a reduction in costs through improved employee productivity. In a 2006 survey:

“90% of employees admitted that their attitude about work is adversely affected by the quality of their workplace environment.”

...and some companies have seen...

"productivity gains of 6% to 16% and reduced absenteeism were achieved by converting to improved lighting."

When you add that, according to the OESX management, an investment in LED carries a payback period of 1 to 4 years, you can understand why companies are getting excited about LED.

Well-Funded

A recent bearish Seeking Alpha article mentioned that OESX would have to raise money soon. With around $5 million available on its credit line and quick product turnaround, it is our opinion that the author is way off the mark with his assessment, at least in the short term. Furthermore, the company’s IR firm replied to the author in the comment section of the article which totally refuted the author’s conclusion. We wanted to include some parts of the article here, but it seems Seeking Alpha removed the article from its site.

However, we need to be aware that OESX filed an S-3 (shelf) in 2017 that remains open:

“In February 2017, we filed a universal shelf registration statement with the Securities and Exchange Commission. Under our shelf registration statement, we currently have the flexibility to publicly offer and sell from time to time up to $75.0 million of debt and/or equity securities, although, we are currently limited to selling an amount of securities equal to one-third of our public float on such registration statement over a 12 month period. The filing of the shelf registration statement may help facilitate our ability to raise public equity or debt capital to expand existing businesses, fund potential acquisitions, invest in other growth opportunities, repay existing debt, or for other general corporate purposes”.

We would recommend that management withdraw the shelf to send a clear message to the market that it does not need to raise money anytime soon.

Conclusion:

After performing additional research into OESX, I am extremely interested in following the company more closely. Due to the project-oriented nature of the business, there is certainly risk that investors will view the company as a one trick pony. But in my opinion, the industry dynamics and the potential for the company being one or two large contracts away from providing the market with more “comforting” visibility is quite attractive.