On September 25, 2017, we disclosed a long position in Tss, Inc. (NASDAQ:TSSI).

TSSI entered our radar on June 2017 at $0.19, where we briefly mentioned that we were adding it to our Tier 1 Pink screen in light of its restructuring efforts which were boosting the bottom line, as well as bullish comments from its Q1 2017 release.

We subsequently added the stock to our “RunToOne” Mock Portfolio on September 20, 2017 at $0.19.

On September 25, 2017 we had a chance to interview management to learn more about their restructuring process, pathway to reaching sustained profitability, and customer concentration risk. The stock was trading at $0.25 at the time.

TSSI became a public company through a merger with a publicly traded special purpose acquisition company (SPAC).

“Special purpose acquisition companies (SPAC) are publicly-traded buyout companies that raise collective investment funds in the form of blind pool money, through an initial public offering (IPO), for the purpose of completing an acquisition of an existing private company, sometimes in a specified target industry such as information technology. The money raised through the IPO of an SPAC is put into a trust where it is held until the SPAC identifies a merger or acquisition opportunity to pursue with the invested funds. Shares of an SPAC are typically sold in relatively inexpensive units that include one share of common stock and a warrant conveying the right to purchase additional shares or partial shares.”

Quick facts (as of 10/3/2017):

- Headquarters: Round Rock, Texas

- CEO: Anthony Angelini

- Number of Employees: 78

- Key Competitive Advantage: A complete product offering for its customers; saves customer’s money; decreases time of deployment of datacenters.

- Price: $0.32

- Insider Ownership: 37.2%

- EV/S: 0.3 using an annual $20 million revenue run rate assumption

- Forward EV/EBITDA: 6x and 3x using a low/high margin assumption heading into 2018

- Fully Diluted Share Count: ~20.0 million

- Fully Diluted Market Cap: $6.4 million

Background

TSSI Description:

“TSS provides a comprehensive suite of services for the planning, design, deployment, maintenance, refresh and take-back of end-user and enterprise systems, including the mission-critical facilities they are housed in. TSS provides a single-source solution for enabling technologies in data centers, operations centers, network facilities, server rooms, security operations centers, communications facilities and the infrastructure systems that are critical to their function. TSS's services consist of technology consulting, design and engineering, project management, systems integration, systems installation and facilities management.”

To know where TSSI is heading, it’s helpful to understand how data centers are evolving, from traditional centers to modular designs. You can think of a data center as a place that houses servers to store information. The growth of the internet, social networking, the cloud and now blockchain tech are key factors that are driving the need for data centers.

Traditional data centers need more up-front planning, involve more equipment and require higher capital outlays. First, you build a brick and mortar building and then you fill it with technology and servers. They must be constructed to accommodate for the future needs of the center and there is always risk and the potential for inefficient use of capital when basing expensive decisions off estimating future growth. Servers are installed on premise.

“The traditional data center, also known as a “siloed” data center, relies heavily on hardware and physical servers. It is defined by the physical infrastructure, which is dedicated to a singular purpose and determines the amount of data that can be stored and handled by the data center as a whole. Additionally, traditional data centers are restricted by the size of the physical space in which the hardware is stored.

Storage, which relies on server space, cannot be expanded beyond the physical limitations of the space. More storage requires more hardware, and filling the same square footage with additional hardware means it will be more difficult to maintain adequate cooling. Therefore, traditional data centers are heavily bound by physical limitations, making expansion a major undertaking.”

Modular data centers solve some of these issues by allowing them to scale over time. Server capacity is built on a frame and delivered to a location, also know as “plug and play.” The modular centers are also lighter, smaller, quicker to deploy, require less equipment and can be more energy efficient.

“A modular data center system is a portable method of deploying data center capacity. A modular data center can be placed anywhere data capacity is needed. Modular data center systems consist of purpose-engineered modules and components to offer scalable data center capacity with multiple power and cooling options. Modules can be shipped to be added, integrated or retrofitted into an existing data center or combined into a system of modules. Modular data centers typically consist of standardized components.

The more common type, referred to as containerized data centers or portable modular data centers, fits data center equipment (servers, storage and networking equipment) into a standard shipping container, which is then transported to a desired location.”

You can learn more about the differences between traditional and modular data centers here and here. Additionally, here is a YouTube video where Dell explains the advantages of modular data centers.

Legacy Years

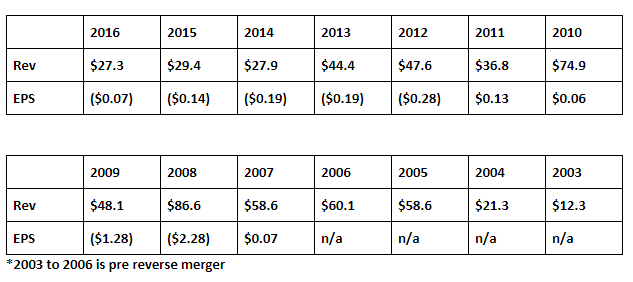

For years, TSSI struggled to gain business traction after its reverse merger in 2007, serving the Traditional Data Center market. This table clearly illustrates this point:

During the company’s “legacy” years, its primary focus was to build expensive brick and mortar traditional data centers and direct involvement with most of the aspects of project implementation, including project management and installing the centers with servers and related technology. This team was headquartered in Maryland. Out of its Texas facility, TSSI operates its facility management business, where it assembles/integrates servers and runs its maintenance services.

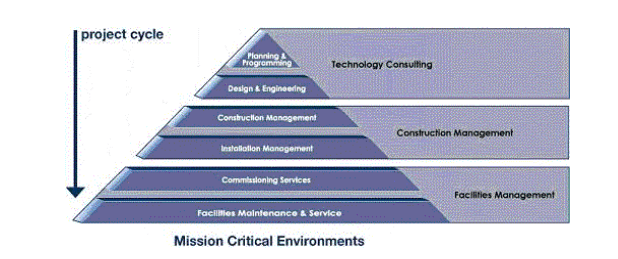

Here is an image from an old 10-K that shows the various aspects of the TSSI legacy business chain:

The erosion of TSSI business over the years was largely the result of two factors:

- Increased competition from larger companies due to favorable industry dynamics. TSSI was essentially a construction company with high capital needs and increasingly low margin opportunities.

- A series of acquisitions focused on growing the low margin, fixing lumpy revenue, and optimizing the construction business did not deliver optimal returns.

The Future

GeoInvesting loves investing in good managers. In 2011, Anthony Angelini joined the company as CEO, replacing the incumbent CEO and founder. He appears to have the experience to turn TSSI around and was very articulate in communicating the challenges and opportunities facing TSSI.

“Mr. Angelini has over 20 years’ experience building and operating services organizations. Anthony has broad experience with international operations, and his businesses have serviced Fortune 100 companies worldwide. Anthony last served as CEO of Zomax, Inc., a Nasdaq-listed company in the Business Process Outsourcing industry, providing fulfillment, eCommerce and manufacturing services. While at Zomax, Anthony implemented a number of growth strategies that lead the Company to be recognized by Fortune and Forbes as one of the fastest growing small companies. He joined Zomax in 1998, following the Zomax acquisition of three companies that he co-founded.”

TSSI carries out a range of “soup to nuts” services that include:

- Consulting- Planning and getting the project ready

- Deployment- Managing the project, including delivery, testing and overseeing installation

- Systems Integration (SI)- Building and integrating servers

- Management (Maintenance)

Early in his tenure, Anthony made an interesting observation that facility management services offering…

- Systems Integration (SI)- Building and integrating servers

- Management (Maintenance)

…are asset light operations with recurring revenue components and high margins.

Thus, this is the direction Anthony decided to take the company, while eventually exiting the legacy construction business. Additionally, management made the decision to continue its consulting business for modular data centers, but to outsource most of the consulting and deployment services to further increase margins; essentially, just retaining a project manager role. In the past, TSSI would provide a substantial amount of labor from its in-house staff.

Industry stats support the company’s new direction:

“The global modular data center market size is expected to grow from USD 13.07 billion in 2017 to USD 46.50 billion by 2022, at a Compound Annual Growth Rate (CAGR) of 28.90%. There is an increasing need for reducing the CAPEX spent on commissioning mission-critical data center facilities. Modular data center solutions provide the required scalability and cost effectiveness for setting up new data centers as well as for upgrading the existing infrastructure. This acts as one of the major drivers of the modular data center market.”

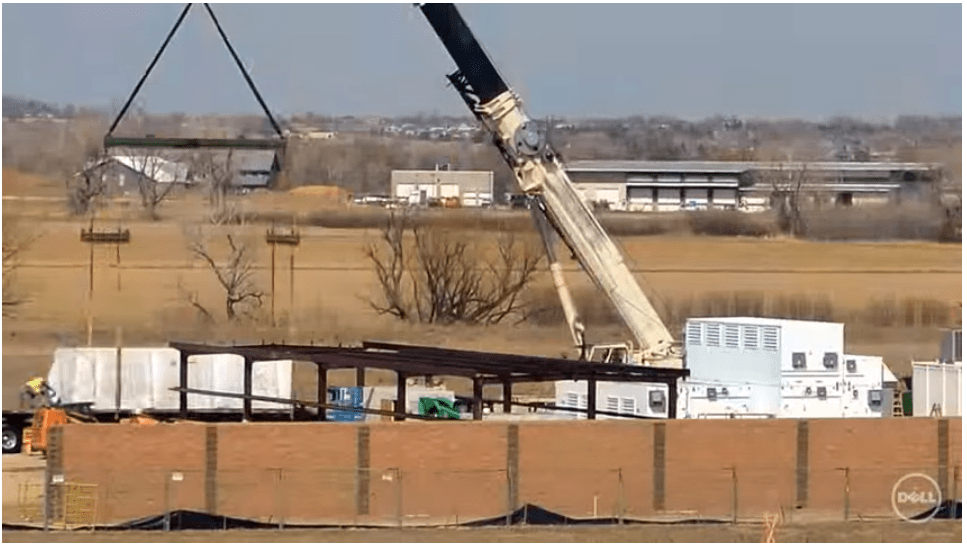

Here is a YouTube video of a modular data center installation:

The exciting part of TSSI angle comes from its facility management services.

Systems Integration

Broadly speaking, this is where the company takes server equipment, technology, wiring and software, and puts it all together according to customer specs, and runs tests.

In the past, traditional data center customers would send their servers to TSSI where it would integrate (rack and stack) and deliver the final product to customer facilities. Think of the chain in this way:

- Customer needs servers for its traditional data center

- Customer sends all its servers to TSSI

- TSSI utilizes in-house equipment along with product it orders to integrate servers

- TSSI sends servers to facility where they must be installed

The growth in modular data centers is tweaking the process:

- Customer has a “pad” to house a modular data center

- Customer sends some sample product and “server” frames to TSSI

- TSSI utilizes in-house equipment along with product it orders to build out the frame

- TSSI sends outfitted frame to be installed at customers’ locations

Since the arrival of Anthony Angelini and a 2013 acquisition of a company that provides integration services, TSSI has put most of its focus on attacking the modular opportunity. It’s worth noting that modular centers also enable operators to benefit from logistics savings:

- Cost saving from sending less equipment to integrators

- Cost saving from sending lighter finished product to third party end customers

Modular centers are good for integrators like TSSI too, due to their cookie cutter build out and less lumpy revenue stream compared to big traditional “one and done” data center projects. Modular data centers provide a better recurring revenue stream compared to traditional center projects, as data centers are gradually expanded over time.

Maintenance

TSSI enters into maintenance contracts with its customers to ensure data centers are running smoothly and to replace/repair equipment that breaks. The company carries out this offering by monitoring centers remotely and by performing yearly inspections. Contracts typically last up to four years:

“We have a 24X7 Network Operations Center in Round Rock, Texas that has the capability of remotely monitoring our data center service contract customers’ facilities for systems operations and emergency events that could lead to outages. Temperature levels, humidity, electrical connectivity, power usage and fire alarm conditions are among the items monitored. The system maintains all site documentation for repairs and maintenance performed on each critical piece of equipment covered under our services. The information is useful to our customers in assessing operational efficiency and causes of failure, and enables them to make critical decisions on repair or replacement strategies based on the operating history of the monitored systems.”

Obviously, this part of the business is quite attractive as it gives the company a recurring revenue stream, which should lead to investors eventually assigning shares much higher valuation multiples. Maintenance offerings can also create a sticky customer relationship and put the company in a good position to gain new business from them as they grow.

Things Are Looking Up

The CEO admits that company could have done a more optimal job in financing the 2013 acquisition. Regardless, the TSSI has been in the process of refinancing its debt with a small equity kicker and after a slow start to getting the acquisition rolling, along with selling off the last of its traditional data center operations and related projects in 2016, things are moving in the right direction.

Margins Increasing

Before Mr. Angelini joined the team in 2011, gross margins were around the 16% level. As the company transitioned away from its legacy business model gross margins have increased markedly. They hovered between 20% and 30% between 2012 and 2016 and have now taken a new leg up, since the company disposed of all its legacy exposure by the end of 2016.

While the first half of 2017 revenues were sharply down due to the elimination of legacy revenue, gross margins improved to 42%.

Profitability Getting Closer

Q2 2017 press release comments

"We feel we have aligned our business properly and have now recorded five consecutive quarters of positive Adjusted EBITDA." said Anthony Angelini, President and Chief Executive Officer of TSS. "We anticipate increasing revenues and profits in the second half of the year as the focus on growth within our core services begins to play out. Our market opportunity remains large and we see positive underlying trends within the services we are focused on delivering."

Management offered a dose of “Information Arbitrage” in its Q2 2017 CC that is no longer available, but that we were lucky enough to listen to it:

- Break-even/profitability levels should now occur at a much lower level of revenue

- Revenues to reach near $5.0 million per quarter by end of year with increasing profitability

Furthermore, the company has started to eliminate liquidity pressures it has been facing.

Caveats

1. Liquidity constraints – As of Q2 2017, the company had:

- Cash of $1.0 million

- A net working capital deficit of $3.4 million

- Short-term debt of $100,000

- Long-term debt of $845,000

“We continue to operate the business with a net working capital deficit and with a stockholders’ equity deficiency. Due to these fluctuations and our liquidity position, we continue to look at alternative sources of funding to strengthen our balance sheet. We are currently evaluating both debt and equity financing alternatives.” Q2 2017 SEC filing

In July of 2017, the company received some liquidity relief when its creditor (2015 loan from Chairman of the Board investment vehicle) extended the maturity of the loan from 2020 to 2022, as well as providing access to an additional $1.5 million.

The Chairman of the Board has now provided liquidity to TSSI in 2015 and again in July 2017, with minimal dilution. This obviously gives me some confidence in the business and that the company won’t embark on a terrible dilutive equity financing, but it is a risk. During the Q2 2017 conference call, which is currently unavailable, management indicated it was close to taking one last step to resolving its liquidity issues.

2. New technology

3. Customer concentration- Will remain an issue in the near-term.

4. Company could be lumped in with electronics manufacturing service (EMS) companies which have been struggling and can carry low valuations. However, TSSI is targeting a high growth niche with a unique product offering. Furthermore, some EMS operators that we track seem to be experiencing a recovery which could lift overall valuations. Finally, many different parts of the value chain exist in the EMS industry. TSSI’s soup to nuts integration/assembly approach is one we have had great success with in the past when investing in other tech companies.

1. Investors may be tepid in believing that management has finally turned the corner, since the restructuring process has been going on since 2011. We think it just took management time to realize they had to let go of their legacy business, and this is understandable.

2. Negative cash flow from operations through the first half of 2017.

Valuation

We can’t use a trailing P/E multiple to value TSSI, since it is still losing money on a trailing 12-month basis and has not consistently made money, but it looks like they are close. Margins are moving in the right direction and with any uptick in sales, income should start dropping to the bottom line.

We don’t think SG&A will move up considerably with an increase in sales, but TSSI has only reported two full quarters (Q1 2017 & Q2 2017) without the legacy business and adjusted EBITDA margins came in at a wide range of 5.3% and 10.3%, respectively. We are going to need to see a couple more quarters before modeling future EPS.

Management has provided investors with some clues, such as optimism that the company is about to reach a quarterly revenue run-rate of $5.0 million, which would be a about a 25% increase from the current run-rate. This would imply a quarterly EPS run-rate of ~$0.01 and 12 month rolling EPS of $0.04, using a low-end margin assumption of 5.0%. Using a high-end margin assumption of 10.0% yields a quarterly and 12 month rolling run-rate EPS of ~$0.02 and $0.08, respectively. We don’t think it is unreasonable to place a 15 P/E on forward EPS, which would translate into a near-term price target of $0.60 to $1.20, or a midpoint of $0.90.

Regardless, for now, Geo bought TSSI as a bet that management has put the company on the right path for profitable growth. The stock is trading at an EV/S of 0.30, using an annual $20 million run-rate assumption and an EV/EBITDA of 6x and 3x using a low/high margin assumption. By any measure, we believe shares look cheap. Aside from operational improvements, shares could get a lift upon TSSI putting liquidity issues to bed. We think this is the biggest near-term roadblock to seeing valuation expand. But this is the reason investors have a chance to buy shares on the cheap.

Ultimately, TSSI can be an excellent acquisition target down the line.

Appendix

Quotes from filings that explain new company direction:

- We have been concentrating our sales efforts towards maintenance and integration services where we have traditionally earned higher margins. Historically our construction services were tied to a few, high-value contracts for the construction of new data centers at any point in time. In addition to contributing to large quarterly fluctuations in revenue depending upon project timing, these projects required additional working capital and generated lower margins than our maintenance and integration services. We have re-focused our construction services towards smaller scaled jobs typically connected with addition/move/retrofit activities rather than new construction, where we can obtain better margins. We have also focused on providing maintenance services for modular data center applications as this emerging market expands.

- We anticipate that our quarterly revenues will be lower than historical levels over the remainder of 2017 as we concentrate our business on facilities maintenance and systems integration services. We made the decision in late 2016 to outsource multiple services that we had previously staffed directly, including consulting design, engineering and some construction project management services. This allowed us to reduce our overhead expenses. We believe that this will decrease the variability in our quarterly revenues and decrease the variability in our working capital by eliminating these large one-off projects. We believe this will also help us manage our liquidity, and contribute to improved profitability.

- This focus towards the modular data center market will increase our customer concentration in the short-term, and concentrate the markets in which we compete. However, our business is now focused on providing a life-cycle of activities in support of the use of modular data centers and rack integration including assembly, deployment and maintenance of these modules. We believe we can be a smaller, more profitable enterprise by narrowing our market focus. The winding down of our less profitable revenue streams should decrease the liquidity requirements of the business, and the reduction of overhead and staffing costs will improve our efforts at profitability and should drive improved financial results for us in 2017.

- In September 2016, we sold the Maryland-based portion of our facilities maintenance business that was not geared towards the modular data center market. During the fourth quarter of 2016, we made the decision to outsource certain services that we had previously provided directly including consulting and design engineering and project management activities. These activities were concentrated on traditional “brick and mortar” type facilities. This decision allows us to continue to provide these services to our customers when required, but at the same time allows us to reduce our fixed staffing and overhead levels. These actions continued the focusing of our activities on the modular data center market. In the first quarter of 2017, we sold another customer contract that was part of our project management business. Collectively these actions generated $1.3 million in cash, resulted in staffing reductions, and allowed us to close our facility in Maryland. As a result of these actions, we lowered our level of operating expenses to improve our efforts at achieving ongoing profitability.

- Over the last several years we have changed our business strategy to pivot the business focus from large, one-off, low-margin data center design and build projects towards services such as our facilities management offering that provide greater recurring revenue streams from ongoing services. This shift was intended to reduce quarterly fluctuations in revenues and margins, and to transition us towards higher margin service lines to improve the profitability of the Company. As part of this strategy, we acquired our systems integration business in 2013 to broaden and diversify our service offering for the data center services market.