Summary Of What’s In This Weekly Wrap-Up

Last week, the microcap earnings season officially began, with most companies we follow posting impressive results. However, many of these reports got “lost” in a week where the stock market pulled back, amid fears of an AI bubble.

Highlights in this weekly:

- Q3 reports from Crawford United Corporation (OOTC:CRAWA), Bk Technologies Corporation (NYSE:BKTI), First Acceptance Corp. (OTC:FACO), Equator Beverage Company (OOTC:MOJO), Acorn Energy, Inc. (NASDAQ:ACFN), Fuel Tech, Inc. (NASDAQ:FTEK), Power Solutions International, (NASDAQ:PSIX), Cipher Pharmaceuticals, Inc. (OTC:CPHRF) (TSX:CPH)

- An awesome MUST WATCH investor insight skull session with Quant investor Yuval Taylor (@yuvaltaylor).

- Latest “You Make the Call” Fireside Chat, Wesley J. Bolsen, CEO of General Enterprise Ventures Inc (OOTC:GEVI).

- Our in-depth take on ACFN 39% Pullback during the week.

- Our quick take on PSIX 23% Pullback during the week.

Crawford United Corporation (OOTC:CRAWA) and Bk Technologies Corporation (NYSE:BKTI) reported record Q3s, while First Acceptance Corp. (OTC:FACO)’s Q3 numbers strongly rebounded from a few quarters of weak growth. Equator Beverage Company (OOTC:MOJO)’s came in with Q3 revenue of over $1 million, its second consecutive quarter over $1 million. Capstone Green Energy Holdings (OTC:CGEH) entered our coverage universe as a new data center stock (turbines), with a strong Q3 update.

Also on the data center front, investors weren’t impressed with Q3 earnings results from Fuel Tech, Inc. (NASDAQ:FTEK) or Power Solutions International, (NASDAQ:PSIX), down 15%, and 23%, respectively, for the week.

Cipher Pharmaceuticals, Inc. (OTC:CPHRF) (TSX:CPH) came in with a nice year-over-year Q3 report, but investors may not have been impressed with the lack of sequential growth from Q2.

Meanwhile, Acorn Energy, Inc. (NASDAQ:ACFN) underperformed, with Q3 revenue and EPS both down sharply year-over-year and shares falling 39% for the week.

As we are now on the hunt to launch Buy On Pullback #14 (BOP) this week, we will be assessing if any of these pullbacks are good candidates for inclusion in the portfolio. Here’s a table that summarizes the reports highlighted in our morning emails last week:

Earnings calls you may be interested in listening to. Click on the ‘Earning Calls’ tab, then select the most recent quarter to listen to their latest calls:

This past week, we also hosted an Investor Insights Skull Session with Yuval Taylor (@yuvaltaylor), Portfolio Manager at Fieldsong Investments, where he manages $18 million. He discussed his quant strategy focused on operating income growth, earnings quality, and fraud detection, while I brought up how I use qualitative signals in microcaps. We actually bounced that idea around quite a bit.

Also, in our latest “You Make the Call” Fireside Chat, Wesley J. Bolsen, CEO of General Enterprise Ventures Inc (OOTC:GEVI), shared why he just joined the company and how their EPA-certified CitroTech fire inhibitor might help position GEVI as a leader in wildfire prevention and treated wood systems. Q2 sales were only $0.69 million, but up 246% year over year. With a capital raise just completed, our job is to decide if we believe that management can get the company to profitability without further dilution.

Before we get deeper into the earnings reports coverage, let’s start with last week’s skull session events, starting with Yuval Taylor, Portfolio Manager at Fieldsong Investment.

Skull Sessions

Betting on the Underdogs With Yuval Taylor, Quant-Investor

For this week’s featured discussion, we sat down with Yuval Taylor (@yuvaltaylor) of Fieldsong Investments, a self-taught quant who built a 40% CAGR over a decade by combining discipline with deep data exploration. Yuval’s story isn’t your usual finance-to-fund-manager tale. He came out of publishing (30 years in it) and didn’t start investing seriously until a sabbatical in Bolivia sparked the idea. Within a few years, he was managing his own capital with algorithmic rigor and now runs an $18 million hedge fund launched in 2024.

What’s refreshing about Yuval is how grounded his approach is: he relies heavily on quantitative signals and ranking systems with 200 factors, but he’s not dogmatic. In fact, he talks openly about where qualitative nuance matters, especially when it comes to turnaround names that can’t yet be picked up by the numbers alone.

“I’m not like this quant who says, oh, all you discretionary investors, you’ve got your heads up your asses, you know, I’m not like that. I have a great admiration for what good qualitative investors do… I don’t think it can be duplicated.”

He’s particularly focused on operating income growth, cash flow return on assets, and something you might not hear much about in quant corners: the stability of a company’s cash conversion cycle. This gives him an edge in spotting high-quality stocks flying below traditional quant screens. His strategy also rewards what he calls “middling” metrics, like margin growth in the 70th percentile, as more sustainable than the flashy extremes that often mean-revert. I actually loved this point, like finding low ranked stocks by the Investor Business Daily that will eventually make it into their top 50.

ACFN, which I discuss at length later, through a long-term EPS analysis, is a great case in point about understanding the qualitative. ACFN was added to Geoinvesting’s longer-term Focus Model Portfolio on September 5, 2025 at $9.40, peaking out at a return of 251%. We had continually communicated that the stock could run into issues if ACFN were not to renew or replace a contract with a large telecom company that was coming to an end. This would lead to an “air pocket” until a new contract came in. Those who automatically assumed (and perhaps did not understand the business model) that ACFN would maintain a quarterly EPS run-rate of near 30 cents got blindsided by the 12 cents adjusted EPS quarter the company reported on Thursday, sending the stock down 40%. Those who understood the qualitative at least had the chance to make a decision to hold or sell the stock into the Q3 report.

The conversation with Yuval hit on plenty of names familiar to our community. Yuval mentioned holding or previously owning:

- Power Solutions International, (NASDAQ:PSIX), a manufacturer of emission-certified engines and power systems for industrial and transportation markets, is a stock both he and GeoInvesting flagged early in its turnaround, on its way from $12 to over $100.

- Conrad Industries, Inc. (OOTC:CNRD), a builder & repairer of steel/aluminum marine vessels, one of his largest positions.

- D-box Technologies, Inc. (OOTC:DBOXF) (TSX:DBO), a maker of haptic motion systems for entertainment & simulation, a tiny Canadian play he’s hopeful about.

- Hammond Power Solutions Inc. (OOTC:HMDPF) (TSX:HPS-A), a manufacturer of transformers & power-equipment for infrastructure, which he rode from ~$10 to over $40 before selling.

He also shared his evolution in handling risk, initially bruised by options overuse and currency exposure in Europe, but now using hedging strategies with put options on single names and a newer custom hedge for factor inversion environments.

What stood out most was his honest reflection on fraud detection, sparked by getting burned on $TIOG, a stock that Hindenburg research eventually took to the woodshed the deep dive short selling report. That led him to adapt the Beneish M-score to catch both high and low manipulative flags, something we resonated with, given our own background in exposing fraudulent microcaps.

In true Geo fashion, the conversation closed with mutual admiration for underfollowed stocks with long, boring histories, companies that don’t get analyst coverage but whose margins or earnings might just be inflecting after years in the shadows. Yuval sees real value in having exposure to those ideas before the crowd catches on.

For anyone interested in the overlap between data-driven rigor and deep small-cap hunting, the full conversation is worth a listen. You can find Yuval’s work at fieldsonginvestments.com.

—

GEVI Targets Wildfire Defense with High-Margin Chemistry

This week’s Fireside Chat in our “You Make the Call” series featured Wesley J. Bolsen, the newly installed CEO of General Enterprise Ventures Inc (OOTC:GEVI), a wildfire-defense and fire-retardant solutions company, who gave a compelling walkthrough of why he joined and why he believes the company is at an inflection point.

Bolsen, a former executive at Perimeter Solutions, Sa (NYSE:PRM), a fire-safety products and lubricant additives company, came in just 30 days before the call, bringing deep domain knowledge from the fire safety industry. His prior company was a key supplier of aerial fire retardants and now has a market cap of around $4 billion. At GEVI, his pitch is simple: CitroTech, GEVI’s core product, is the only EPA Safer Choice certified fire inhibitor on the market.

Unlike traditional fire retardants based on ammonia phosphate, which are known for aquatic toxicity, CitroTech uses food-grade potassium citrate, making it safer for the environment, pets, and people. Bolsen believes this safety edge will open doors to both residential wildfire defense systems and treated lumber applications in fire-prone areas.

Bolsen explained that unlike foams or gels that evaporate quickly, CitroTech can stay effective for weeks until it is physically washed off by rain.

GEVI’s strategy focuses on three pillars:

- Home defense systems, which are already generating revenue

- Lumber and building material integration

- Ground-based fire prevention, targeting government and utility contracts

The company is still small, with $687,000 in Q2 revenue, but Bolsen emphasized that with over $8 million in cash and minimal debt, GEVI has enough runway to reach breakeven without another capital raise. He also hinted that the near-term catalyst may come from a lumber partnership, where CitroTech could be factory-applied to wood and potentially included in building codes for Class A fire-rated materials.

Bolsen made clear that the company is not trying to build a business model tied to the unpredictability of fire seasons. Instead, GEVI is focused on preventative use cases and recurring revenue streams, particularly in applications like home defense systems and fire-resistant lumber, that do not rely on active wildfire events to drive demand.

On the competitive side, Bolsen acknowledged that GEVI is going up against a dominant incumbent, but he framed the opportunity as a ground game versus an air game. CitroTech’s advantage is being applied from trucks, 24/7, regardless of wind or daylight. Aerial retardants, by contrast, can only be dropped under specific weather conditions.

Licensing is also part of the plan. GEVI may not apply all the CitroTech product themselves. Instead, Bolsen sees value in becoming the “Intel Inside” of fire safety, enabling partners to build with or spray their product.

He closed the conversation noting that the team is lean, the technology is patented, and the business model is built on moving gallons of high-margin chemistry, not chasing fires but preventing them.

We will be watching to see if the company can lock in contracts across wood products or wildfire zones to validate this go-to-market path. Until then, GEVI remains one of the more intriguing asymmetric setups we have spotlighted in this Fireside format.

—

The Weekly Wrap-Up is meant for those in a hurry, along with those who want to spend a weekend hunting for ideas or quickly catch up what we talked about during the week. Our Weekly Wrap-Up brings together everything we discussed during the week in our morning emails and premium alerts, as well as new information and high conviction ideas that we did not communicate that you should know about. From earnings coverage, new research coverage on stocks, picks and research from our subscribers to event highlights from our monthly open forum that takes place to the beginning of each month and interviews with management teams and investors.

Missed any emails this week? You can catch up on all of them in one place — just check out the full archive here. Missed any emails this week? You can catch up on all of them in one place — just check out the full archive here. |

—

Earnings News

CRAWA Shows Us Why Investing Can Be Tough

After we closed Crawford United Corporation (OOTC:CRAWA), a provider of specialty industrial products and engineered components, as an active holding from our Open Forum Focus Model Portfolio last year, the stock nearly doubled. From its initial entry, it has returned 353.5%. This week’s record Q3 numbers stung even more: sales jumped to $47.1 million from $36.7 million, and EPS rose to $1.52 from $0.95. Growth came from both organic expansion and acquisitions, with industrial and transportation segments showing strong orders and pricing.

This is a reminder of how tough investing can be. We closed the position in the focus model portfolio, because of a short term slow down in growth.

However, the stock is still in our select model portfolio universe, one of the areas within our platform that we identify stocks to include in the focus model portfolio. It was added in August 2017, now up 1,372%.

MOJO Keeps Rolling

Equator Beverage Company (OOTC:MOJO), a coconut beverage maker and distributor, just delivered its second straight quarter with over $1 million in revenue, bringing three of the last five quarters above that mark. EPS came in flat at $0.00, an improvement over last year’s loss. It’s nice to see that the company is starting to show some revenue consistency at elevated levels, however, in order for the company to really get a valuation boost it’s going to have to start reporting some tangible positive EPS.

With a small float and limited liquidity, share buybacks didn’t hit management’s prior target of 150,000 shares, likely because of the illiquidity in the stock, but the intent is still there.

If MOJO starts adding new distribution wins, it could get interesting fast.

FACO Finds Its Footing

After a few average quarters, First Acceptance Corp. (OTC:FACO), a non-standard personal automobile insurance underwriter, surprised to the upside with Q3 EPS of $0.27, almost double last year’s $0.14, and showed better underwriting performance. Revenue rose to $140.7 million, up from $129.3 million last year. Management credited improved claims handling and some stabilization in auto repair costs for the strong result. The company may be also benefiting from the sale of its brokerage business in late-2023 brokerage sale, as the acquirer (and now partner) could be writing more policies under FACO.

FACO’s tangible book value is $5.05. FACO’s current price of $4.03 is well below the 1.5x–2x book value typical for insurance companies. If claim frequency stays low, there could be upside potential, implying a price range of $7.57 to $10.10. This stock remains in our Open Forum Focus Portfolio and has become more timely. You can watch my chat with the management that took place during a virtual conference at the Microcap Investing Cliff Note Substack on June 12, 2024.

BKTI Strong Federal Demand Drives Q3 Beat

Bk Technologies Corporation (NYSE:BKTI), a designer and manufacturer of two-way radio communications equipment for public safety and industrial users, reported Q3 sales of $24.4 million, up from $20.2 million last year. Gross margins expanded as the company focused on its premium BKR 9000 radio. The USDA placed a $12.9 million order, showing strong federal demand tied to infrastructure and security.

CGEH Clean Energy Play Capitalizes on Data Center Tailwinds

Capstone Green Energy Holdings (OTC:CGEH), a clean-energy company focused on microturbines and on-site energy-as-a-service solutions, pre-announced strong Q3 results, linking growth to distributed, AI-ready energy systems. Despite CFO and Chairman changes, the quarter was described as transformational, with positive net income and growing traction in microgrid and data center energy markets. We have contacted management for an interview request.

FTEK Muted Quarter But Data Center Narrative Remains Intact

Fuel Tech, Inc. (NASDAQ:FTEK), a maker of air-pollution-control and process-optimization technologies, reported revenue of $7.5 million, slightly below last year’s level and below analyst estimates. EPS of $0.01, flat year-over-year. Management emphasized focus on emissions control solutions for power generation, particularly data center-driven demand. Air pollution control (APC) backlog grew more than 20% quarter-over-quarter, signaling strong future demand. The acquisition of IP from Wahlco adds new technologies to its product lineup, broadening the company’s air pollution control solutions. The stock has been in a downtrend due to a lack of new data center emission control contract wins and weak AI sentiment. However, bids for new data center contracts remain active, with the Q3 call indicating that we should get some answers on this in Q4 2025 or Q1 2026, and some InfoArb on the Q3 call indicates that FTEK’s power play is broadening outside the data center theme.

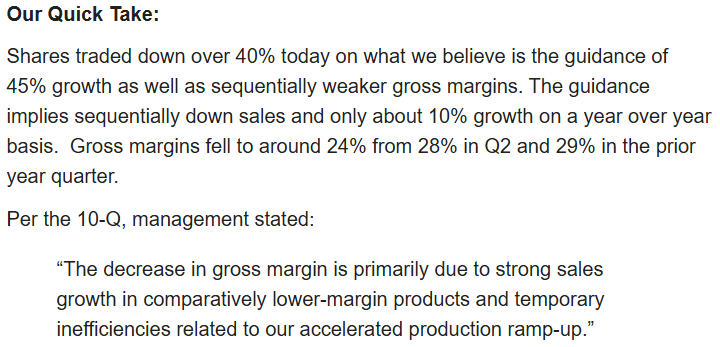

Guidance And Gross Margins Stall PSIX Momentum

Power Solutions International, (NASDAQ:PSIX), a manufacturer of emission-certified engines and power systems for industrial and transportation markets, reported a strong Q3, with sales jumping to $203.8 million from $125.8 million and EPS of $1.20 versus $0.75. Despite the solid numbers, the market didn’t react kindly. Shares dropped over 40% as investors reacted to weaker gross margins of 23.9% (versus 28.9% last year) and guidance indicating that full-year 2025 growth of 45% may have already peaked, implying a sequentially lower Q4.

The quarter showed strength in the data center segment, but operational ramp-up challenges and margin pressure created uncertainty.

Here’s our quick take from our morning email:

PSIX has historically not communicated with investors, but there may be a silver lining:

Well, interestingly, it appears the company is holding a special investor conference call on Monday. We’re trying to get the details to attend the call. Sneaky bastards are holding the conference by invite only.

Cipher Deleveraging, With Strong YoY Growth

Cipher Pharmaceuticals, Inc. (OTC:CPHRF) (TSX:CPH), a Canadian specialty pharmaceutical company with a portfolio in dermatology and other therapeutic areas, reported what looks like a strong Q3 at first glance. Most of the year-over-year growth came from the Natroba™ acquisition, while organic sales and sequential growth remained flat. The company also continued paying down debt and buying back shares.

Management remains upbeat, pointing to licensing discussions and potential accretive M&A, but investors seem to want proof before getting excited again. We’re keeping an eye on Natroba’s continued adoption in the U.S. and progress on licensing or market expansion as key indicators for future upside.

Here’s our quick take from our morning email:

ACFN Faces a Timing Bump

Acorn Energy, Inc. (NASDAQ:ACFN), a provider of remote-monitoring and control solutions for energy-infrastructure assets and IoT systems, reported its Q3 2025 results. Sales came in at $2.48 million, down from $3.05 million, and EPS dropped to $0.12 from $0.29. The decline was mainly due to the early fulfillment of a major telecom contract. Monitoring revenue hit a record, which is encouraging, but a more tepid tone from CEO Jan Loeb rattled investors, pushing the stock down 39% for the week. ACFN remains a solid recurring-revenue business, but with the hardware revenue boost from the large contract now behind it, investors are asking what’s next?

If you think about it, the price drop could make sense from the perspective of investors who might not fully understand ACFN’s business model. To me, it was pretty straightforward. The stock was kind of priced for perfection, meaning that to hold a price in the $20 area, investors would have needed to hear more positive sentiment on when ACFN might either renew the telecom contract that fueled growth over the last four quarters or land a new customer. Well, that didn’t happen and the Q3 press release and earnings call didn’t really give any concrete timeline on when this might happen, which was actually less aggressive than prior earnings call commentary.. So, that leaves a gap of uncertainty and a reason for some investors to bail and come back later.

Anyways, the drop happened, and there’s no real sense in overanalyzing it. If you’ve followed us long enough, you know that even long-term multi-bagger stocks don’t move in a straight line. There’s bound to be disruption, whether it’s market sentiment or short-term interruptions in growth. But it’s actually these pockets of interruptions that can create opportunity. By the way, this is where our buy-on-pullback model portfolio lives. It doesn’t mean it’s “wrong” for short-term investors to bail and come back later when there’s more confirming news that new growth initiatives are working. This is especially true since management threw another wrench into the fire by talking about softness in residential markets due to high interest rates and lower adverse weather events that would lead to more demand for back up power generator demand and monitoring. However, long-term investors might want to take a different perspective with ACFN.

For them, the question becomes: even if the stock might have been expensive or priced for short term perfection at $25 or $30, how does ACFN look down here at $13.00 to $15.00? Ultimately, we think longer-term investors will be rewarded from that range or lower, and we’ll show you why.

Here’s some more context. Over the last four quarters, the company benefited from a large contract with a telecom company, selling sensors installed in generators at cell tower locations to monitor performance. The offering also includes actual “homebase” monitors. After installation, ACFN receives recurring monitoring revenue on a monthly basis, with about 90 percent gross margins. Hardware revenue consists of large upfront payments, while recurring revenue consists of smaller monthly payments that grow over time. The telecom customer originally signed a two-year contract, but accelerated most of the installations, frontloading hardware revenue in 12 months. So, instead of a smoother two-year earnings cadence, growth happened more quickly, leaving recurring monitoring revenue as the main growth driver. This also put pressure on ACFN to find new customers or re-up the current contract quicker than anticipated (contract only covered about 1/3 of the telecom customers tower locations)

And here’s the funny part. Investors probably would have preferred ACFN smooth out the earnings over two years rather than fulfill the contract in one year, which helped build its current $4 million cash position faster.

Timing, not lack of fundamentals, drove this pullback, maybe rightfully so. Long-term investors who look past the short-term reaction may see an opportunity at current prices. Admittedly, if you look at the current annual EPS run-rate of around $0.40-$0.60, you could say that the stock is only worth anywhere from $12 to $18 in the near-term with an aggressive PE of 30x, which I believe is justified given the predictability of the recurring revenue. The company also has $2.00 per share in cash, which could be additive to the value.

However, this does not take into account the company winning any new contracts or making any acquisitions.

| Regarding the wide EPS range, 10 cents (Q3 2025) assumes the company has recorded a tax provision, even though it’s a non-cash event since the company has plenty of NOLs to shield it from actually paying taxes. However, GAAP requires that a company record a provision for taxes if management believes the company will be profitable moving forward. |

In most cases, I don’t perform an extensive long-term predictive cash flow analysis to value stocks. There are so many unknowns. I’m often more interested in understanding if a company can execute a business plan, so that its cash flow has the potential to be a lot bigger than it is today. However, in cases where I’m looking at a recurring revenue model, that analysis can be useful.

So, we did a quick analysis to determine what ACFN earnings per share could look like in five years, given the following assumptions:

- Current base of annual recurring revenue is $6 million

- Total revenue grows at 20% a year

- 15 to 20 percent of hardware revenue becomes monitoring revenue, based on management’s prior statements.

- Recurring revenue gross margins of 90%

- 50% of revenue drops to the bottom line, based on management’s prior statements.

- Is a zero tax provision because of a significant amount of NOLs that should cover our forecast period

- Put a 25x on the end-of-period earnings

- No contribution from large contracts

ACFN – Assumptions

We began by forecasting revenue. For hardware revenue, we assumed it would remain relatively flat in 2025 before growing at a 15.0% CAGR thereafter. This assumption appears reasonable when compared with historical growth rates (2022 and 2023 numbers). Monitoring revenue was modeled as a function of hardware sales, with 17.5% of incremental hardware revenue converting into monitoring revenue, consistent with the CEO’s comments indicating a 15–20% range. These assumptions get as close to 20% annual revenue growth.

It is important to mention that recent monitoring growth has appeared more muted; however, this is because competitors had offered heavily discounted hardware during a mandated upgrade cycle. In this context, ACFN’s ability to maintain its pricing suggests that achieving these growth targets is plausible. Also, keep in mind that when management references an average 20% growth target “over time,” it implies potential variability year to year, including periods of slower growth. In short, ACFN is likely better suited for long-term investors. While the assumptions are ambitious, there remains a risk that actual growth may fall short.

For gross margins, hardware remains at 55%, consistent with 2023 and 2024, while monitoring maintains a 90% margin, in line with 2021–2024 performance.

For operating expenses, we began with R&D by annualizing 9M 2025 results, resulting in $1.097M for FY2025. SG&A was estimated by annualizing 9M 2025 figures, bringing total SG&A to $5.836M. This resulted in operating income of $1.093M, which we used as our baseline. For subsequent years, we did not explicitly forecast operating expenses; instead, we relied on management’s guidance that approximately 50% of incremental revenue flows through to EBIT through operating leverage.

We assumed a 0.0% tax rate due to ACFN’s net operating losses (NOLs). Finally, diluted shares outstanding were projected to grow at 0.4% annually, consistent with historical averages.

ACFN – Income Statement (Historical & Estimates)

ACFN – Valuation (PE Multiple)

Using a 25.0x P/E multiple, we arrive at the following price projections. According to the model, by 2030, ACFN is expected to generate approximately $3.50 in EPS, which implies a price target of $87.38 and 5.62x multiple on invested capital (MOIC) by 2030

I’ll leave it up to you to decide what you would pay for this scenario, today.

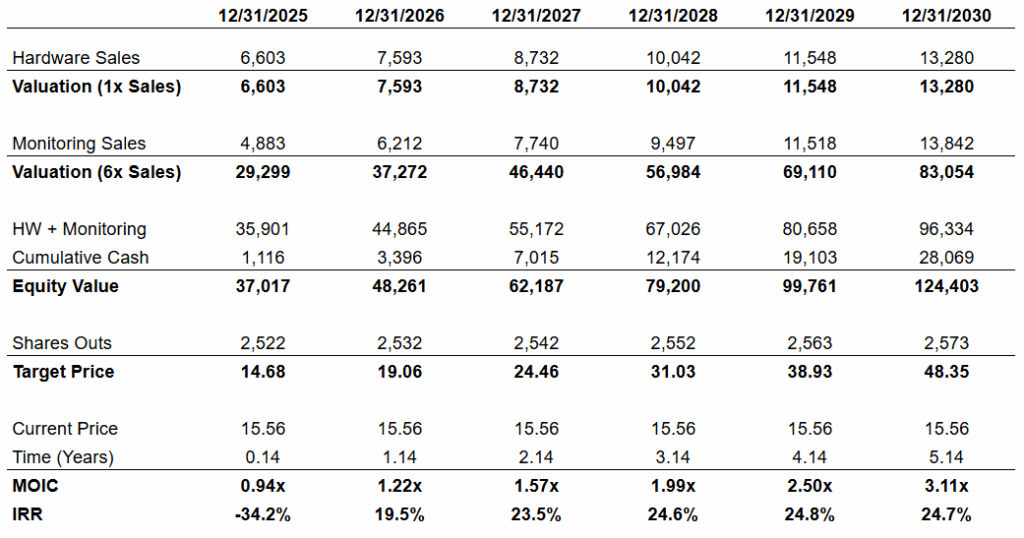

ACFN – Valuation (EV/S Multiples)

We also valued ACFN using EV/Sales multiples. For the hardware segment, we applied a 1.0x multiple, and for the monitoring segment, a 6.0x multiple. Under a hypothetical scenario where 100% of cumulative net income converts to cash and accumulates on the balance sheet, we estimate an additional $28.07M in cash, bringing total equity value to $124.4M and price target of $48.35. This represents a 3.11x MOIC and an IRR of 24.7%.

Another thing worth noting is that the company finally mentioned data centers in the body of its Q3 press release, even though the CEO continually responded to my questions on the data center opportunity with very muted responses during our Skull Sessions with him, saying that it wasn’t really an opportunity.

“We expect secular trends, such as increasing adoption of IoT connected devices, real-time data collection, demand for predictive maintenance and data analysis, compliance and reporting requirements, and growing energy demand from AI, data centers and other sources to provide a long-term tailwind for our business.”

Like many microcap set ups, a lot of your decision-making process will depend upon whether you believe management will execute. It’s the wildcard. We try to improve our odds of being right by hunting in a higher quality universe of the 10,000 microcap stocks in North America. Here’s a nice clip from the ACFN Q3 conference call that makes us feel pretty good about betting on the company, long-term.

—

| If you enjoy performing press release research or think you will see value in a tool that expedites your press release research process, you should check out a press release tool my team is building by going here. |

—

Premium Emails Sent During The Week

Premium Emails Sent During The Week

11/04/2025 – CRAWA Quarterly EPS and Revenue at Record Highs; MOJO Remains Consistent Above $1 Million in Revenues For 3rd Straight Quarter

11/05/2025 – FACO Q3 EPS Nearly Doubles, FTEK Q3 Meets Estimates; Maj’s Faves From Starting Five; Invite to GEVI Fireside

11/06/2025 – CGEH Pre-announces Q3 with Data Center Angle; ACFN Slides on Mixed Q3 Comments; BKTI Continues Strong Earnings

11/07/2025 – CPHRF Strong Q3; PSIX Shares Crash Despite Decent Q3 Numbers; Next Open Forum Invite

—