Summary

-

Through a reverse merger transaction with a start-up “A.I.” data analytics medical device company (Firefly Neuroscience), Wavedancer, Inc.'s (NASDAQ:WAVD) COBOL code modernization business is set to be sold to the CEO for $1.5 million, or at a P/S multiple below 0.2x, a valuation we feel is ridiculous.

-

The reverse merger press release did not mention that the CEO is buying the legacy modernization business! WHY?

-

Our valuation opinion is based on management’s own presentation in 2021, before the current CEO’s appointment in August 2021, where it set revenue goals of $100 million by 2025, or 10x the company’s annual revenue run-rate, and $10 million in EBITDA.

-

The presentation is no longer on the company’s website, but it can still be viewed via an 8K.

-

The stock has been in the dumps for the last three years due to management’s failed attempt to expand outside the company’s core code modernization business by purchasing a blockchain logistics software company in 2021 called Gray Matters for $7.5 million.

-

In early 2023, WAVD sold Gray Matters to a venture capital firm for $2.4 million.

-

WAVD has a track record of competing in the code modernization industry. Now that they sold Gray Matters, management has been able to focus on its core business again, and just won two long-term contracts (August & September) worth up to $19 million, much more than what the CEO is offering to buy the WHOLE modernization business for.

-

Interestingly, the CEO has also been acting as CEO of Gray Matters.

-

As justification for the $1.5 million price tag, in the merger proxy, the company now cites weak industry factors, despite appearing optimistic in recent press releases announcing the new contract wins and its third quarter 2023 SEC filing.

-

Using the source that WAVD itself used in its favorable 2021 investor presentation, shows that the lines of COBOL code addressable market has about quadrupled since then.

-

Additional conversations with an industry expert also indicate that the code modernization industry is experiencing new strong tailwinds that will last several years.

-

In fact, over the last two months, International Business Machines (NYSE:IBM) and Amdocs Limited (NASDAQ:DOX) acquired code modernization assets.

-

We list other options that WAVD’s Board could explore to unlock shareholder value.

-

$SSNT 5x move and $SLGD’s ~100% rise shows what can happen when a shareholder-friendly reverse merger transaction takes place.

WAVD modernizes databases/IT infrastructures that were built on outdated COBOL code and has mainly focused on selling its services to U.S. government agencies. The stock previously traded under the symbol IAIC and under the name Information Analysis (founded in 1979).

We are baffled by the recent events.

-

Why are they doing a reverse merger with a company that has significant capital needs and minimal revenue?

-

Why is the CEO, Jamie Benoit, trying to buy the modernization business for just 0.2x sales and 0.08x current long-term backlog?

-

Why did the company only include these details in the reverse merger proxy filing and not also include them in the reverse merger press release?

-

Why did management's outlook on the modernization business, discussed in the reverse merger proxy, suddenly sour after they continually talked about the great growth opportunity of this industry, even as of its third-quarter 2023 SEC filing?

-

Why hasn’t management disclosed that the source it used to paint a positive picture in 2021, in terms of the billions of lines of COBOL code that could be modernized, has quadrupled this stat?

Please note that we have no position, long or short, in WAVD. But per our terms and conditions, we may establish any type of position in the future.

We want to stress that we understand the last three years have been tough on management and members of the Board, and that we are not necessarily opposed to the company consummating a reverse merger.

However, it’s our opinion that the Board should have chosen a more established company than a start-up instead of one with less than $1 million in sales that is going to raise significant capital to attempt to commercialize its product. And we are not talking about a company that management was exploring in the “motorcycling industry,” as discussed on page 129 of the reverse merger proxy. Seriously!?

However, at the very least, the Firefly reverse merger transaction could have been structured in a manner more favorable to shareholders.

On a side note, Benoit’s $1.5 million offer is less than a $2.5 million tuck-in acquisition of an IT firm the company made before Benoit joined the company.

If the Board needs a reference point, here is what happens when you actually consummate reverse merger type deals that are beneficial to shareholders.

-

$SSNT is now going through a reverse merger type transaction, where the legacy business will be spun off and remain public and in shareholders’ hands. The stock went from around $3.00 to over $20.00 in about 30 days.

-

$SLGD rising ~100% on December 26, 2023 shows what can happen when a public company hosts a reverse merger with a quality company.

At the end of this article, we’ve outlined deal alternatives that the Board could consider.

Feel free to reach out to us if you would like to discuss the facts surrounding Wavedancer. We love talking about stocks.

The Crux Of Our Gripe - Part One

On November 16, 2023, WAVD announced that the Board approved a transaction, in which upon shareholder approval, Firefly Neuroscience, Inc., an A.I. medical device company will reverse merge into WAVD.

Firefly is an:

AI-Enabled medical technology company focused on bringing FDA-cleared Brain Network Analytics platform

It appears Firefly recently entered the commercialization stage.

As part of the reverse merger transaction, WAVD’s CEO, Jamie Benoit, is seeking to buy the legacy assets of the company for $1.5 million, or less than 0.2 times revenue.

Benoit was appointed as CEO of Wavedancer on August 26, 2021. Under his leadership, shares outstanding have increased 53%. (13M to 20M pre-reverse split and 1.3M to 2M post split), while losses ballooned.

Now, WAVD Shareholders will get diluted down to owning ~8% of the new entity, after taking into effect the issuance of 28.7 million shares to Firefly. Firefly’s revenue for the first nine months of 2023 was $479,000 ($648K annual run-rate).

At the current price, the new entity will be trading at a market cap of around $45 million, or around 70 times Firefly’s 2023 revenue run-rate.

We can’t fathom how the stock will be able to come close to holding that kind of valuation, given new market conditions, where quality matters, and where Firefly will have to raise a ton of money to execute its commercialization plan.

Even though the Board approved the merger, the transaction still needs to be approved by shareholders.

This is all occurring at a time where the code modernization industry is experiencing new growth trends, and in the face of the company setting a goal in 2021 to generate $100 million in revenue (more than 10 times revenue) and $10 million in EBITDA by 2025. This goal was based on a $1 trillion addressable market opportunity referenced by management.

Oh, by the way, the addressable market, in terms of lines of COBOL code that may need to be modernized, has since quadrupled!

Unfortunately, the company has been unable to meet its financial targets and is still operating at around the same revenue run-rate as it was when it set these goals.

In our opinion, this was due to:

-

Underperformance of the acquisition of Gray Matters in 2021 for $7.5 million plus additional consideration if certain performance metrics were achieved.

-

Diverting resources and focus away from the legacy code modernization business.

-

Failing to stay focused on some of the objectives laid out in WAVD’s 2021 presentation, which included aggressively acquiring other companies in the modernization code industry.

Gray Matters sells some type of blockchain supply chain software solution.

After WAVD reported a string of large quarterly losses, management pulled the plug on Gray Matters in March 2023, initially selling the company to a venture capital firm for $1 million and a 24.9% interest in Gray Matters, which was later amended to $2.4 million and no ownership interest.

Apparently, it appears that the software wasn’t ready for prime time and required more resources that WAVD could provide:

“We encountered unanticipated challenges with the software product we acquired which required substantial modifications and disrupted our sales efforts. Additionally, deterioration in the capital market for early-stage technology companies, which occurred shortly after our purchase, adversely impacted our ability to raise capital required to fund GMI.”

By the way, guess who’s the CEO of Gray Matters and listed as the founder? If you guessed Jamie Benoit, you’d be correct. This can be clearly seen at Gray Matters’ “Meet the Team” page.

(Maybe it’s nothing, but we found it weird that Benoit is listing himself as the founder of Gray Matters when, as far as we can tell, that information was never brought up when WAVD acquired the company.

At the time of the sale (of Gray Matters to WAVD), the CEO was apparently Jeff Gerald who later sued WAVD.

The good news is that now the company can get back to focusing on its “boring” modernization business that’s already secured two long-term government contracts, totaling up to $19 million, since the sale of Gray Matters.

- Seven year, $12 to $15 million contract in August 2023.

- Three year, $4 million contract in September 2023.

Imagine that, get back to the core business and start making progress again!

It was actually the award of an up to seven-year, $25 million government contract in 2020 that moved the stock from around $0.20 to over a dollar ($2.00 to $10.00 adjusted for a reverse split), under the pretext that the company had visibility for the first time in a long time, allowing it to aggressively pursue growth in its modernization business.

You can read about why we liked the company at that time and included it in our model portfolios, here. The stock actually went to hit a high of around $6.00 ($60 post reverse split) when the company was spinning its block chain software logistics strategy. Shares have now more than round-tripped.

Although we locked in some gains during the rollercoaster ride, it still hurts, as we thought the stock was on the path to being a long-term megabagger. To put it bluntly, we take our reputation seriously, so we took this one to heart. WAVD matched our Tier One quality microcap markers, while intersecting with our checklist of multi-bagger markers we’ve built over the last 30 years.

In light of these facts, we think it’s prudent for the Board to reconsider the reverse merger transaction, or at the very least, modify the Firefly transaction to create long-term shareholder value by allowing shareholders to participate in the potential growth of the modernization business.

As it stands now, if Benoit perseveres, he’ll have interest in the modernization business, Gray Matters (as he’s listed as the CEO & founder), and will have some ownership in Firefly. Why can’t shareholders get a piece of all this action? All they seem to be getting is some “call option” on Firefly.

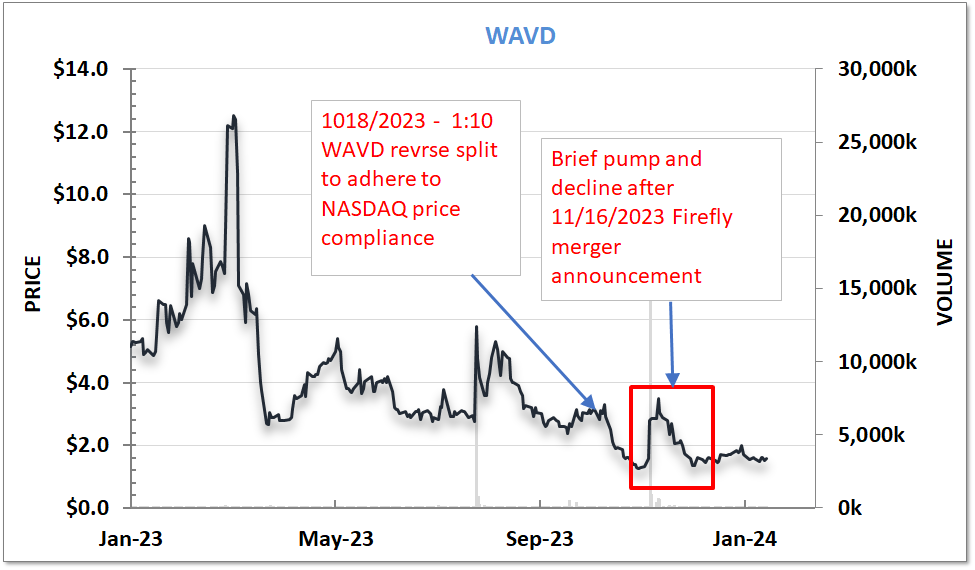

We think investors agree with us, since the stock is trading 49% lower from when it affected a 1 for 10 reverse split on October 18, 2023 to remain listed on the NASDAQ, and lost all the initial gains from a temporary pump in shares thatWAVD experienced when it entered into the A.I. reverse merger agreement.

Furthermore, the investment banker engaged to assist with the transaction, Brc Group Holdings, Inc. (NASDAQ:RILY), has not issued a fair value opinion on the transaction. So we’ll do it for them. In our opinion, it ain’t fair.

On top of that, some boutique investment firm, Southwind Capital, introduced to the Board by Benoit mentioned that, under certain conditions, the modernization assets would be worth more than the $1.5 million it was being sold for.

The Crux Of Our Gripe - Part Two

Let’s Make A Deal

We do not have an opinion on Firefly, but with sales of less than $1 million, we assume it’s going to require significant capital as it just entered the commercialization stage (aka.. dilution).

“The Company is in the development stage and faces all of the risks and uncertainties associated with a new and unproven business. Our future is based on an unproven business plan with no historical facts to support projections and assumptions. We have no operating history as a distributor of medical devices to clinicians. The Company is currently generating minimum revenues and does not expect to generate significant revenue until it has successfully launched broad commercialization of the BNA Platform.

Our financial statement footnotes include disclosure regarding the substantial doubt about our ability to continue as a going concern.

To strengthen our liquidity in the foreseeable future, we have taken the following measures: (i) negotiating with existing and new investors to raise additional capital; and (ii) taking various cost control measures to reduce the operational cash burn.” Proxy

Better yet, the reverse merger press release did not mention that Benoit is buying the legacy business. This is all it said.

“WaveDancer’s operating subsidiary Tellenger, Inc., a provider of modernization services to the federal government, will be divested through a transaction closing simultaneous to the Firefly merger.”

Well, if you read the boring lines in the 8K filed along with the press release, you’ll notice this.

“On November 15, 2023, WAVD entered into a Stock Purchase Agreement with Wavetop Solutions, Inc.(“Wavetop”), a company owned and controlled by WAVD’s chief executive officer, to sell all of the outstanding shares of Tellenger, Inc. to Wavetop. Tellenger is the company through which WAVD operates its day-to-day business.

Wavetop has agreed to purchase all the outstanding shares of Tellenger under a Stock Purchase Agreement for a total purchase price of $1.5 million plus the assumption of the employment agreements that WAVD possesses with Jamie Benoit, Gwen Pal and Stan Reese which includes the obligation to pay severance under such agreements.”

Why wouldn’t the company disclose this very important information in the press release? Could it be that it knows that most microcap investors and shareholders probably aren’t going to read the proxy? Is the Board concerned that activists might find this story intriguing?

While not disclosing all the facts of the transaction in the press release isn’t illegal or breaks any laws, we feel it is incredibly disingenuous, especially when taking into account the last few years.

But here’s what hurts more. Benoit’s potential purchase is occurring right when the company secured some long-term contracts, at a time when the industry is inflecting to a new period of growth that will probably last several years.

After reading the rest of this report, you might find yourself asking,

“How the heck could WAVD not find anyone to pay more than $1.5 million for the legacy assets?

Greenfields Opportunity

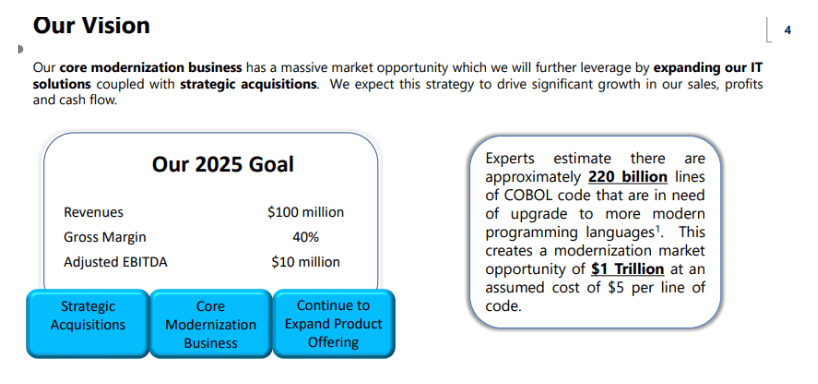

So, how big is this COBOL modernization opportunity? Luckily, the company shared their insights with investors prior to Benoit’s appointment as CEO. Greenfields would be an understatement!

In June 2021, WAVD published a presentation showing it was aiming for its modernization business to generate over 10x its annual revenue, or $100 million, and adjusted EBITDA of $10 million, due to a favorable $1 trillion addressable market opportunity to attack a portion of the:

“...220 billion lines of COBOL code that are in need of upgrade to more modern programming languages.”

Source: Investor Presentation dated June 2021

Again, to put that into perspective, before the disastrous Gray Matters acquisition, the company had a history of generating revenue of around $7 to $10 million a year, and being right around break-even.

|

By the way, don’t waste your time looking for the presentation. It appears that management removed the presentation from its website. However, here is the link to the 8K with the presentation.

|

Making good on their enthusiasm, on April 27, 2023, the company completed a tuck-in acquisition, Tellenger, for $2.5 million. Tellenger accomplished some of WAVD’s new growth initiatives outlined in its presentation by securing new markets, adding ancillary services and broadening its customer base:

“With Tellenger’s range of products and services, organizations can proactively manage cyber and cloud risks, better safeguarding critical intellectual property and preventing large-scale data breaches and ransomware attacks. In addition to IAI solutions, Tellenger, Inc. will continue to provide cyber security solutions across a broader set of industries, including healthcare, manufacturing, and government sectors.”

Finally, per the third quarter 2023 SEC filing, the company still saw the a large opportunity in their modernization business:

“Through our acquisition in April 2021 of Tellenger, Inc. (“Tellenger”), which is now a wholly owned subsidiary of the Company, we acquired competencies in web-based solutions and cybersecurity. Tellenger is a boutique IT consulting and software development firm specializing in modernization, software development, cybersecurity, cloud solutions, and data analytics. We believe combining web-based solutions with system modernization will provide us with the skill sets that are needed to migrate legacy systems to the cloud. We foresee this as a key component of our modernization growth since there are billions of lines of code, in both the governmental and commercial sectors, that eventually must be modernized. It is also our intention to better leverage our resources, largely gained through the acquisition of Tellenger, to take advantage of the growth in the cybersecurity market.”

Already Favorable Industry Outlook Improves

As we stated, as part of a reverse merger transaction Benoit is aiming to buy the legacy business for less than 0.2 times revenue. We are baffled that the Board accepted this bid at a time when the company has divested the cash-draining asset bought under Benoit’s tenure, and at a time when the industry is about to inflect to new growth heights.

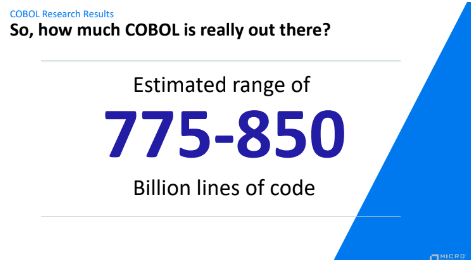

In fact, THE market research source WAVD referenced in the company’s 2021 presentation updated some data points, showing that the number of lines of COBOL code “out there” has quadrupled since then:

Source: Microfocus Presentation - ‘How much COBOL is out there? New opportunity for application modernization’

Expert Call

Expert calls we’ve conducted confirm the new growth tailwinds. For example, apparently, IT resellers are now packaging code modernization offerings into an entire suite of digital/cloud modernization offerings, due in part to customers demanding that be the case.

So now, code modernization firms have a whole army of resellers to market to, as opposed to having to market to the end customer, thereby increasing scalability as well as shortening sales cycles.

This is going to lead to resellers and cloud software-focused companies to potentially buy code modernization companies.

For example, Astadia, competing primarily in the government sector, was acquired by Amdocs Limited (NASDAQ:DOX) for $75 million on November 2, 2023. AmDocs is an Israeli IT provider that helps organizations accelerate mainframe modernization and cloud migration. We estimate that AmDocs paid one to two times revenue for Astadia.

We found it very interesting that AmDocs, a company in the media industry, is buying a code modernization company operating mainly in the U.S. government sector.

Why? Because WAVD primarily targets the government. This also seems contradictory to WAVD statements it made in its reverse merger proxy that the government is taking their moderation efforts in-house.

The following conference call excerpts regarding the acquisition put a lot of what we’re talking about into focus:

“We just did an acquisition around Astadia. And you might think, well, that's an interesting acquisition for Amdocs. Well, because we have an interest to move legacy mainframe stuff as well to the cloud. Why? Because number one, we can move them to modernize systems. Number two, we want to be part of that ecosystem of helping our customers move and migrate to the cloud. And it's a multiyear journey.

So when you talk about like some of the wholesale systems are like decades old, right? So there's an opportunity to get them out of data centers and move them on to the cloud, like I won't mention names or anything like that, but there was one guy that had like old Sun SPARCstation sitting around running applications that you had to do something about. So there's still -- there's still these opportunities around. So this is why in terms of growth pillars, we think this is a multiyear investment. We're doing key acquisitions to get more...

Timothy Kelly Horan

Oppenheimer & Co. Inc., Research Division

We're on Astadia -- so I guess most of that stuff is COBOL. And I mean are they using artificial intelligence to rewrite the code or how do they migrate the code to cloud?

Anthony Goonetilleke

Group President of Technology & Head of Strategy

Yes. So yes, it's a good question. Great, great question. So it's 2 things, right? So one, there is a group of individuals that have amazing experience of modernizing enterprise applications. right? Just that's all they've been doing, right? So they're focused on it and they have experience on it. Number two, they have built a tool set on how to do kind of side-by-side code testing, modernization and the third angle of it, in addition to the platform that they have to do it, so they have these platforms.

So when you think of -- you can go to ChatGPT and give them a bit of COBOL code and say, "Hey, like modernize this -- write this in Java, no problem. But on the other hand, when you take a complicated enterprise application and you're trying to break it down into functions in Java and try to migrate and modernize it. It's not that straightforward, right? So they have built these methodology over a number of years that help you accelerate it, but also the big thing that really interested me when I sat with them was take some of the risk out of that process.

So people are most concerned not about the ability to modernize and move it to the cloud, but am I screwing something up, right? Like what's the risk in doing this because I don't have documentation. I don't know the code for this, like is it going to run the same way I expected. And they're putting a lot -- there's a lot of IP on there to test side-by-side do comparison, do audit trails while modernizing it, which is just as important.”

On January 18, 2024, International Business Machines (NYSE:IBM) announced the pending acquisition of application modernization capabilities from Advanced,

“a strategic move by IBM to bolster its position in hybrid cloud and AI.”

The terms of the deal were not disclosed, but is expected to close in the second quarter of 2024.

“This acquisition will enhance IBM Consulting’s services in mainframe application and data modernization, marking a significant step in IBM's ongoing commitment to supporting clients through their digital transformation journeys.

CEOs are prioritizing technology modernization to accelerate business transformation and gain a competitive advantage. According to a recent IBM Institute for Business Value survey, 67% percent of executives surveyed say their organizations need to transform quickly to keep up with the competition, and 68% of respondents say mainframe systems are central to their hybrid cloud strategy.”

Industry stats

The Application Modernization Services Market size is expected to grow from $5.2 billion in 2022 to $32.8 billion by 2027 at a Compound Annual Growth Rate (CAGR) of 16.7% during the forecast period.

Interestingly, the growth forecast is increasing. In 2021, the CAGR was set at 14.3% per this report.

Alternative Strategies

We think that the more shareholder-friendly moves would include the following:

- Work with investors to finance a purchase of the modernization business at a fair price

- Keep searching for a company in the industry that would pay a fair price. (And follow option 4 below)

- Merger/Spinoff - The SSNT model referenced in the introduction of this report.

- Complete a reverse merger

- Firefly

- More established company

- Spin off the legacy business to shareholders, while retaining some interest in the reverse-merged company. (And follow option 4 below)

- Do nothing at all

- Build on the two new contract wins.

- Go back to the plan outlined in the 2021 presentation.

- De-list from the NASDAQ and de-register from the SEC to save money until turnaround gains sustained momentum.

- Explore expense reductions.

- Report financials on OTC Markets.

We are asking the Board to consider these options and leave a legacy that says you cared about maximizing shareholder value.

We know you’ve been through a lot and you’re probably tired, but if you consider the options that we laid out, we’re fairly certain that it will pay off in the end. At this point, at least we know one Board member has voted against the current transaction on the table.