Written in Collabortation with GeoInvesting Contributor Glenn Bloxham-Mundy

Introduction

Konatel, Inc. (OTCQB:KTEL), through its subsidiaries, provides a variety of retail and wholesale telecommunications services including mobile voice/text/data service, mobile numbers, SMS/MMS services, SD-WAN and IoT mobile data service. One of KonaTel's subsidiaries, Infiniti Mobile, https://www.infinitimobile.com/, is an FCC authorized national wireless Lifeline carrier with an FCC approved wireless Lifeline Compliance Plan, certified to provide government subsidized phone service to low-income Americans.

KonaTel's other subsidiary, Apeiron Systems (www.apeiron.io), is a global cloud communications service provider employing a dynamic "as a service" (CPaaS/UCaaS/CCaaS/PaaS) platform. Using its own national network, Apeiron provides voice, messaging, data, SD-WAN network, and other platform services using innovative network and software designs. All of Apeiron's services can be accessed through both legacy interfaces and rich communications APIs (application programming interface).

KonaTel’s subsidiaries complement each other through the use of mutually shared technologies and infrastructure. KonaTel is headquartered in Dallas, Texas.

GeoInvesting’s brief coverage history of KonaTel includes the following:

January 15, 2021 – Established a small position in KTEL at $0.50 as we came away impressed with the company after an interview with management.

February 8, 2021 – Added KTEL to our COVID-19 risk assessment on how the pandemic would affect companies in the long-term.

February 12, 2021 – Conveyed a primer on KTEL to GeoInvesting members, with the help of contributor Glenn Bloxham-Mundy, detailing a brief history of the company’s beginnings.

March 6, 2021 – Maj had the pleasure of speaking with Sean McEwen, CEO of KTEL and Josh Ploude, CEO of Apeiron via a virtual conversation. In focus was KonaTel's service matrix in which the segments of Mobile Voice, Lifeline, Paas a& CPaaS, and Mobile Data were elaborated upon.

KonaTel Quick Facts, as of 3/29/2021

|

Share Information

|

|

Close Price

|

$0.25

|

|

MCAP (m)

|

$10.2

|

|

EV (m)

|

$10.0

|

|

Shares (Basic) (m)

|

40.7

|

|

Shares (Diluted)(m)

|

44.1

|

|

Trading venue

|

OTC

|

|

Financial YE

|

31-Dec

|

|

Key Metrics

|

|

TTM Revenues (m)

|

$8.7

|

|

P/S (x)

|

1.2

|

|

EV/S (x)

|

1.2

|

|

TTM EPS ($)

|

$0.00

|

|

TTM P/E (x)

|

NM

|

|

Current ratio

|

0.89

|

|

Short- term debt

|

Zero

|

|

Long – term debt

|

0.27

|

|

BV per share

|

$0.04

|

|

Tangible BV per share

|

($0.00)

|

|

Business Activity

|

|

Description

|

Provider of cellular products and services

|

|

CEO

|

Dr. Sean McEwen

|

|

Headquarters

|

Dallas, Texas

|

|

Website

|

https://www.konatel.com/

|

|

Catalysts & key risks

|

|

Potential Catalysts

|

TAM, Larger sales team, Pivot to newer, more robust product suite

|

|

Risks

|

Customer concentration

|

As a GeoInvesting member, you are probably aware that we have been fond of investing in the cloud communication space, such as in like Crexendo, Inc. (NASDAQ:CXDO) and Altigen Communications, Inc. (OTCQB:ATGN), two companies on our Favorite Model Portfolio. Today, we have added KTEL to this list.

CXDO and ATGN can be considered Unified Communications as a Service (UCaaS) service providers, while the KTEL comparable communication solution provides underlying (foundational) services, operating as a Communication Platform as a Service (CPaaS).

In simple terms, UCaaS providers offer a variety of packaged solution to their customers, while CPaaS companies offer an extensible platform to customers (retail or wholesale UCaaS providers) who want to build their own communication solutions. Think of ATGN and CXDO as Ringcentral, Inc. (NYSE:RNG), and Konatel, Inc. (OTCQB:KTEL) as Twilio Inc. (NYSE:TWLO). We love platform-driven companies and can see ATGN and CXDO benefit from a relationship with KTEL, if pursued and developed.

To understand why, consider that the UCaaS arena is quite competitive, in which being able to offer a solution with many product features is critical. So, UCaaS players could utilize KTEL’s platform and APIs to extend current communication solutions.

We thought putting UCaaS vs. CPaaS into perspective would be useful to help you understand KTEL’s story. You can read more about UCaaS and CPaaS here.

We need to caution that we are still in the very early innings of understanding KTEL's growth plan and still have yet to develop a high conviction that management can execute this plan.

The company completed its reverse merger in 2017 and since then has not really grown consolidated revenues. 2017 Revenue were $11.5 million compared to revenue of around $9.0 million in 2018 and 2019 and a 2020 run-rate of $9.0 million based on the nine months 2020.

However, this is what creates opportunity in microcap land. A dive under the hood reveals that certain parts of the business are growing nicely, which may be close to showing up in the consolidated revenue line (potential InfoArb). Closer inspection also points to the company potentially being on brink of reaching profitability for the first time in its history. This assumption is based on KTEL’s small or break-even quarterly profits through the first nine months of 2020.

Furthermore, over the last couple of years, the company has worked to integrate and expand its two acquisitions, Apeiron and Infiniti Mobile, (it took nearly a year just to complete the FCC approval process for its acquisition of Infiniti Mobile) and refocus its efforts into higher margin business prospects to counter the lack of growth in its legacy product lines.

We are excited to find KonaTel at what we believe could be an important inflection point if new products combined with the launch of a new aggressive marketing plan pays off.

Finally, as you know, we love following companies that have large insider buying, as is the case in KTEL. The CEO, D. Sean McEwen, purchased 2.0 million shares of KTEL in a private transaction in October 2020, increasing his personal stake to 15.5 million shares or about 38% of the total shares outstanding.

Background

KonaTel’s story begins in 1983, when its Chairman/Founder, D. Sean McEwen, started a software company called ‘TriTech Software Systems’ at the ripe age of 22 years old. Hailing from a Software Engineering background, McEwen leaned on his technical expertise where his company innovated today’s modern-day emergency 9-1-1 computer aided dispatch (CAD) system; an iteration of the emergency dispatch systems invented in the 1970s but based solely on Microsoft technology with integrated GPS based tracking and predictive routing technology.

Over 17 years serving as CEO, he and his partners evolved TriTech into an enterprise application and systems integration company, specializing in mission critical enterprise software solutions for public safety (Police, Fire, EMS).

In 1995 his company received a distinction as the most innovative Windows application from Microsoft, and in 1998, TriTech was listed as #344 on the Inc. 500 with a five-year revenue growth of 846%. McEwen and his team successfully scaled the business from just 1 employee to 130 at the time of his exit, selling the business to WestView Capital Partners in the mid-2000s. At that time TriTech was generating around $40MM in annual revenue. Today, TriTech has over 4,000 employees and brings in around $500MM in revenue annually.

It was during this period that McEwan discovered his love of building and scaling software companies in a financially sustainable manner, with the business being fully self-funded until it reached positive cash flow. An integral part of his success at TriTech was in the transformation from a group of software engineers creating a great product into a fully functioning sales and marketing-oriented business - an experience that he would have to lean on down the line.

Following his exit to West View Capital Partners in 2005, McEwen spent 9 years working on an array of projects: VC work (specifically post Angel/early VC rounds), serving as and gaining notoriety as a founding board member of the first ever ETF of ETFs, Russell Exchange Traded Funds T (NYSE:ONEF) (sold to Russell Investments of Russell 2000) and taking on various global (USA, China, Peru, Croatia, and Serbia) consulting roles within the software and telecommunications industry.

However, over this period he realized that being a passive investor did not align with his personality and the entrepreneurial itch grew. By 2014, he had enough and so he took $2.6MM of his own cash and purchased the assets of a dying telecommunications company called ‘Coast to Coast’ - a cellular reseller. This business would lay the foundations for what would become KonaTel as we know it today.

Initially, KonaTel began as a cellular reseller (a/k/a MVNO – mobile virtual network operator). An MVNO does not own its wireless network:

“a wireless communications services provider that does not own the wireless network infrastructure over which it provides services to its customers. An MVNO enters into a business agreement with a mobile network operator to obtain bulk access to network services at wholesale rates, then sets retail prices independently.[1] An MVNO may use its own customer service, billing support systems, marketing, and sales personnel, or it could employ the services of a mobile virtual network enabler (MVNE).”

After 2 years and getting the MVNO business close to a point of profitability, McEwen’s software instincts kicked in and he realized that ultimately, if he were to be successful with KonaTel and avoid the telecommunications’ price race to the bottom, he needed to pivot the business model away from simply re-selling (which ultimately had a ceiling to its upside) into a software platform as a service company that “owned” its wireless network.

McEwan’s thinking was that by constructing a wide/diverse telecommunications software platform, KonaTel would create true intrinsic value and would be able to sell a multitude of valuable services on top of this layer, much in the ilk of Amazon with AWS - in software, McEwen’s experience taught him that owning and controlling the source-code and software is everything.

It was around this time that, when exploring accretive acquisition opportunities, McEwen decided that he wanted to take KonaTel public. While adapting the business, he recognized the value of being a public company, particularly in the sense that it positioned you strongly versus private companies when undertaking acquisitions, as you effectively have currency for acquisitions through your stock. So, in 2017, KonaTel went public on the OTC market under the ticker KTEL. Shortly thereafter, KonaTel completed its first two acquisitions. First, the company acquired ‘Apeiron Systems’ - a communications platform service company created by Joshua Ploude (still serving as Apeiron’s CEO) that complemented KonaTel’s long-term strategy well, and true to McEwen’s thinking, the transaction was made easier as a public company allowing them to purchase the business exclusively through KTEL stock. Their second acquisition was a cellular reseller known as ‘Infiniti Mobile’ that holds one of the few FCC approved national wireless reseller compliance plans (i.e., licenses) for the Lifeline cellular market.

McEwen spent the next year and a half tidying these businesses up - for example, Infiniti Mobile was sitting on over $700k in debt which needed to be paid down. McEwen purchased the business at the time in part for its FCC license and potential cash flow and hence used this to reduce debt materially and as it stands today, they are almost entirely debt-free with positive cashflow and revenue growth. What’s interesting here, though, is the fact that this was done without a sales team - something that we will revisit shortly and believe is key to accelerating KonaTel growth story.

As it stands today in 2021, KonaTel operates as national telecommunications carrier, with 2 subsidiary businesses (namely Apeiron and Infiniti) providing innovative communication solutions across diverse segments: fixed line voice, 4G & 5G mobile voice also supporting private LTE (CBRS), Lifeline, mobile data (IoT), SD-WAN and other platform service (PaaS & CPaaS) offerings. KonaTel’s diverse revenue portfolio, especially with its Lifeline component, provides a defensible moat against a variety of economic downturns, which was demonstrated during the negative economic impact of COVID-19.

Company Breakdown

As we mentioned, KonaTel operates through two subsidiaries in the telecom market: Apeiron (~70% of sales) and Infiniti Mobile (~30% of sales).

Aperion’s Business

Apeiron is a facilities-based multi-discipline communications carrier providing business and developer-oriented services. The company’s primary technology is built on a foundation of its software-driven Communications Platform as a Service (CPaaS). Apeiron developed, owns, and operates its carrier-grade, facilities-based national network that processes over a billion transactions each month. The company holds a Federal Communications Commission (FCC) Internet Telephony Service Provider (ITSP) license with multiple Autonomous System Numbers (ASNs) enabling direct allocations of local numbers and IP address resources.

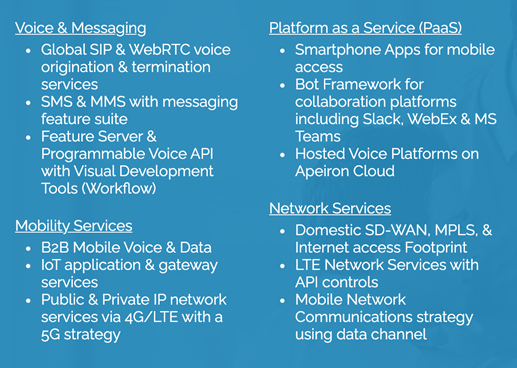

Apeiron’s multi-region national private cloud network includes full OSS (Operational Support System) integration, enabling real-time auto-scale capabilities that can handle most any workload or growth rate. Apeiron’s fully redundant national network can deliver private voice and IP service to most any U.S. address as well as full Over the Top (OTT) support including mobile 4G and 5G endpoints with full support of the FCC’s newly emerging private LTE / CBRS initiative. Some of Apeiron’s services are outlined in the below image:

It’s worth noting that, with Aperion, the opportunity lies in the idea of ‘Edge Computing’ - in essence, bringing their service right to the customer’s doorstep and pushing the network out to the ‘edge’ which allows for quality control and service level guarantees, a key selling point. For example, when we us Zoom for video-calls, we do so by using the public internet and hence signal quality is not guaranteed; it is instead what’s known as ‘best service’ and of course calls can therefore break-up and lack quality.

This is where Apeiron can add differentiating value to its clients. For example, a bank could work with Apeiron to guarantee a quality of service for all their telecommunications needs in a high security manner - the result being no packets dropped on the calls while their high security measures are also met.

Without owning the network and the points in between (network operations centers, software, hardware, switches, etc.), you simply cannot control the entire call flow and ‘push’ guaranteed quality to the ‘edge’. Hence, Apeiron controls both qualities and do not then have to pay subsequent royalties, resulting in higher margins. Sean is very focused on building the reach of Apeiron’s network, not only for quality-of-service reasons, but because doing so also provides KTEL with a cost advantage. For example, competitors that don’t aggressively build out their network will raise prices to limit network congestion, opening the door for KTEL to take market share.

Apeiron is broken down into two business units. The exciting growth driver for KTEL is going to be Apeiron’s CPaaS business unit it will market to end customers that include to applications developers, call centers and small and medium size businesses.

The Apeiron MVNO business unit markets to MVNO’s that desire to beef up their service offerings. Furthermore, this unit now houses KTEL’s legacy MVNO business which now has the benefit of layering on services that the Apeiron acquisition brought to KTEL.

Apeiron’s Industry

Apeiron ultimately operates within the Telecommunications market which, after decades of fierce competition, has in some areas become a price race to the bottom. Instead, McEwen suggests that the value in this industry comes from platform companies operating through their extensible software-based businesses, particularly in specialty verticals that many GeoInvesting members will know well: PaaS and CPaaS.

CPaaS stands for Communications Platform as a Service and is essentially a cloud-based service platform that allows developers to add real-time communications features to their own applications without needing to build backend infrastructure and interfaces. Prior to this development, real-time communications have taken place in applications built specifically for these functions, e.g. Skype, FaceTime, WhatsApp, etc. However, over time companies noticed the friction caused by this - e.g. why can we call our banks via our native mobile phone app but yet we cannot speak with them through our banking apps? These real time communications apps have been the paradigm for a long time due to the high cost of building and operating a communications stack. However, well developed CPaaS platforms offer a development framework for building real-time communications features without having to build a network. This typically includes software tools, standards-based application programming interfaces (APIs), sample code, and pre-built applications.

CPaaS and PaaS providers like KonaTel are able to deploy cloud solutions to offer clients of any size the ability to easily develop and embed communications features into their applications and infrastructure. Development teams using CPaaS can save on a whole host of costs: HR, infrastructure, and time to market. Moreover, with CPaaS companies, developers can pay exclusively for the services they require through competitive, consumption-based pricing models.

With the growing trend of customer-facing communications, the need for ‘contextual communications’ is one of the biggest drivers of the CPaaS market, as companies seek to improve overall customer experience. The demand for high quality communications has also been heightened with the rapid shift to work-from-home due to COVID, which is also expected to continue post COVID as many companies are realizing they can deploy and manage a decentralized workforce with the good communications tools. Some common use cases are video-enabled help desks, appointment reminders, call center call processing, and authentication services. With the former example, video-enabled help desks allow customers to receive more personal and engaging service than traditional channels.

For example, when embedding Apeiron’s click-to-call APIs, a customer could click a button on a company’s website and instantly contact a support agent. Agents can also use contextual information about each customer to provide more customized service, such as the current items in their online shopping cart, the webpage they are currently on, or previous tickets with the support department. Companies can also use CPaaS services to better track customer engagement across different platforms.

Infiniti Mobile Business and Industry

KTEL’s second business unit, Infiniti Mobile, is one of a small group of licensed national mobile carriers to hold an approved Federal Communications Commission (FCC) mobile Lifeline Compliance Plan (LCP license), which gives it a hunting license to obtain licenses in all 50 states. So far, the company holds active Lifeline licenses in eight states including Georgia, Kentucky, Maryland, Nevada, Oklahoma, South Carolina, Vermont and Wisconsin. According to industry source CGM, there are approximately 39 million Lifeline eligible households in the United States, approximately 10 million currently have Lifeline service. Established in 1985 under the Regan Administration, Lifeline provides subsidized phone service to millions of qualifying low-income households and has enjoyed bi-partisan support for decades. Following FCC guidelines administered by the FCC’s Universal Service Administrative Company (USAC), Infiniti Mobile manages a national network of agents and other distribution methods to verify, issue, and administer Lifeline cellular service delivery for eligible low-income U.S. households. From our research it appears that the FCC is not going to be liberal in handing out additional LCP licenses.

By the way, Infiniti gets access to Apeiron, giving it some cost advantages and superior service creds over competitors.

Catalysts/Why Now?

We believe that there are several reasons to be bullish on KonaTel’s future. Firstly, from a macro point of view, at GeoInvesting we believe investing in PaaS and CPaaS companies is a safer way vs. UCaaS to invest in secular trend and those best-placed in the space will benefit from this tailwind in the years to come, either through industry consolidation (with acquisitions at premiums) undertaken by incumbents or through long-term growth. In our interview with Founder D. Sean McEwen, he corroborated this view and mentioned it being a key reason he founded KonaTel with a pivot toward the software as a service, recurring revenue business model.

Secondly, we are excited to find Apeiron at what we believe could be an important growth inflection point; new products combined with the launching of aggressive marketing campaigns pay off. In this case, the inflection is the evolution of KonaTel from a small group of software developers with a great product suite to a fully-fledged marketing and sales-oriented business.

This transformation would mirror what McEwen achieved at TriTech earlier in his career and would ultimately lead to a material increase in revenue. In the world of sales, according to McEwen, you typically have two types of set-up: farmers and hunters. The former nurtures the already established relationships and tends to grow share of wallet slowly over years. The latter, however, goes out to the market and ‘hunts’ for new business opportunities and logos. And it is here, in the latter category, that KonaTel has significant opportunity.

To date, KonaTel has achieved everything through little to no direct sales and/or marketing, a remarkable achievement and testament to both the business as well as industry trends. However, McEwen now intends to ramp up their sales team and we believe this to represents an opportunity to predictably grow revenue materially, as well as de-risk the customer concentration.

KonaTel intends to ramp this up first through both a web-based and indirect agent sales channels, like most competitors. They must, however, proceed cautiously, as these relationships can be damaged quickly if KonaTel were to fail to deliver.

Thirdly, although McEwen took KonaTel public through the OTC markets, he intends one day to bring them onto the NASDAQ. While this may be some time off and will require certain SEC financial requirements to be met, it would ultimately provide more liquid ‘currency’ for acquisitions, raise awareness with investors and elevate valuation multiples. In late 2020, KonaTel up-listed from the OTC Pink to the OTC QB and at the same is no longer designated as a Penny Stock per SEC rules.

Fourthly, Infiniti is only actively marketing its services in 1 of the 8 states it is approved in, and still can apply for licenses to offer its services in 42 more states. There is obviously a huge runway for growth at Infiniti which we believe is a very sticky business with very little competitive threats. In fact, while investors will likely want to focus on Apeiron, we really like what Infiniti brings to the table: Predictable and “moat-ish” cashflow.

Lastly, we believe that McEwen’s past record both with KonaTel, as well as his time in the VC business, his first venture and successful exit from TriTech and his time serving on the board of ONEF, will allow him to execute successful accretive acquisitions and embed them into the business effectively when the time is right. To do this, capital may likely need to be raised but if delivered successfully, we could witness positive margin expansion and a stronger competitive position.

Valuation

KonaTel currently trades at a relatively subdued valuation vs. peers, as many investors are likely unaware of its possible imminent inflection point. Shares are currently trading at a P/S of about 1.2 on a ~$10MM market cap (as of 3/29/2021) and its latest 10Q highlights its early success in shedding their lower-margin, commoditized business in favor of more meaningful, value-add revenue that enables a high RoIC.

We think there’s a couple of ways to value KonaTel. Firstly, from an EV/Sales ratio, which allows us to take debt into consideration rather than a simple P/S, it’s currently trading at a P/S around 1.2 (as of 3/29/2021). When compared to comps, we believe a ratio more in line with 2-4 to be a realistic base-case, with a best-case, should their growth be sustained, nearer the 10 range. At an EV/S of 4, we would be looking at a share price of around $0.86, and at an EV/S of 10 a price of around $2.14.

Another, more rough and ready, measure would be to look at valuing it off its revenue alone. Peers seem to trade between a 6-8 multiple here, which on current numbers would suggest KonaTel to be worth in the region of $1.32 - $1.76. Twilio Inc. (NYSE:TWLO) is selling at P/S of 29!

All in all, KonaTel has around $700k in the bank, fairly low long-term debt, is cash flow positive and is setting up for the next leg of revenue-growth.

Risks and Caveats

The main risk identified to date is customer concentration, particularly within the Apeiron business who currently have two key customers. On the positive side here, Apeiron’s primary customer is on a 3-year contract and are only 5 months into this. Moreover, it’s a government-related contract and hence payment is both timely and reliable. So, while management highlighted customer concentration as a risk on our call and has a goal of reducing this percentage of 5%, the risk still exists for now.

Another risk to consider is the potential dilution incurred if the company raises capital for future growth (in Sales and Marketing) as well as acquisitions. McEwen acknowledged multiple times the importance of careful capital allocation practice as a CEO and we believe should he pursue an acquisition, based on his track record, it will likely be smooth and quickly accretive.

Additionally, we are considering the impact of scale within this industry - as a small business, how does KTEL compete effectively within the CPaaS API market vs large players such as Twilio Inc. (NYSE:TWLO)? This question is posed considering our understanding that at this moment in the US, larger CPaaS players use their volume to negotiate better rates from the carriers and then pass that through to the customer.

So, the risk would be that at KonaTel’s volume, they sometimes come up as more expensive vs larger CPaaS players like Twilio. However, research into the company to date suggests that KTEL provides services more down-market with APIs that tend to be more user friendly for their SMB clients vs. the large Enterprise space Twilio operates within

Conclusion

KTEL combines software interfaces for easier to use experiences, creating low code configurations of CPaaS rather than raw access to APIs. The thinking here from KTEL is that if they make it easier, more useful with additional value-added services for those who don’t have large development shops (like most SMBs), they’ll consume more.

It is worth noting that this industry is incredibly exciting but equally as challenging to truly understand. We continue to work with KTEL’s management and perform research to better understand their competitive advantage in the space. We believe we’re getting close.

This is an industry undergoing secular change, as more and more companies look to outsource large CapEx infrastructure. KTEL and its subsidiary businesses, particularly Apeiron, should benefit from their ability to offer ‘edge computing’ - this is because they own every single component (hardware, software, switching infrastructure, etc.) and hence do not rely on any cloud hosting services. This allows them to co-locate switching-centers where the biggest telecom carriers exist, in turn ensuring quality control for the customer.

Lastly, as Jim Barksdale famously once said, ‘the only way to make money is bundling and unbundling’. We believe that KTEL’s strength is in the bundling of services, ultimately creating a closer rapport with end-users/customers and in turn driving up their ROI in their customers’ eyes.

References