Introduction

$MSLP ($0.56; $18.6M market cap)

MusclePharm is a US-based performance lifestyle company. It develops, manufactures, markets and distributes branded nutritional supplements. It offers various types of powders, capsules, tablets and gels. It comprises recognized brands such as MusclePharm and FitMiss® and is sold in more than 100 countries globally.

On January 15, 2021 we disclosed our long position and also decided to place the stock on our Run to One Model Portfolio when it was trading at $0.48. This is a very preliminary look at the company and we will like to see a few more quarters of progress before getting too excited. But we believe the stock is an interesting bet at the current price, given that it is selling at a price to sales of 0.3 and enterprise value to sales of 0.4, as noted in the table below.

In our December 6, 2020 weekly wrap email we highlighted bullish comments from management:

“Our management team has spent the last two years dramatically restructuring MusclePharm and are now generating positive cash flow and well positioned for long-term profitable growth even in the current COVID-19 pandemic environment. The business turnaround was driven by reducing low margin sales into inefficient channels, increasing gross margins, decreasing operating expenses and improving our overall EBITDA. We have many of the leading brands in nutrition but we needed to do a much better job of realizing the value of our brands by reducing product discounts and being more efficient in our promotional activity, reducing SKU’s that are not properly positioned, and better aligning our operations with repositioned top-line growth. We have strengthened our scalable platform in 2020, with a focus on increased profitability. Our omni-channel strategy is working and enables us to capture a greater share of this large and growing space. We also believe we are very well positioned to utilize our leading brands to expand outside of the nutraceutical space in the near future.”

Quick Facts – As of 03/11/2021

|

Share Information

|

|

Close Price

|

$0.56

|

|

MCAP (m)

|

$18.6

|

|

EV (m)

|

$23.6

|

|

Shares (Basic) (m)

|

33.1

|

|

Shares (Diluted)(m)

|

49.1

|

|

Trading venue

|

OTC

|

|

Financial YE

|

31-Dec

|

|

Key Metrics

|

|

TTM Revenues (m)

|

$66.7

|

|

P/S (x)

|

0.3

|

|

EV/S (x)

|

0.4

|

|

TTM EPS ($)

|

$0.03

|

|

TTM P/E (x)

|

18.7

|

|

Current ratio

|

0.3

|

|

Short- term debt

|

$6.2

|

|

Long – term debt

|

Zero

|

|

BV per share

|

NM

|

|

Tangible BV per share

|

NM

|

|

Business Activity

|

|

Description

|

Markets and distributes nutritional supplement products

|

|

CEO

|

Ryan Drexler

|

|

Headquarters

|

Burbank, California

|

|

Website

|

https://www.musclepharm.com/

|

|

Catalysts & key risks

|

|

Potential Catalyst

|

Increasing trend of healthier lifestyle

|

|

Risk

|

Slowdown in consumer spending; Weak balance sheet and loss of traction on restructuring

|

Brief History

The company was founded by Brad Pyatt in 2008 and grew at a rapid pace which saw multiple new product launches and very high-profile celebrity endorsement deals. Its products at one time were endorsed by Arnold Schwarzenegger, Tiger Woods and Manchester City Football Group. While the revenues grew rapidly primarily fuelled by celebrity endorsements and high marketing spend, profitability remained elusive. The CEO, Brad Pyatt was ousted and Ryan Drexler took over as the new CEO. He undertook the restructuring of the business including cutting SKUs and breaking out of large endorsement deals.

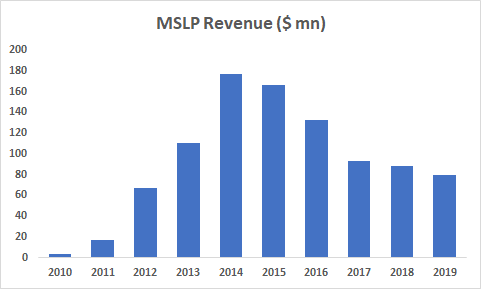

As seen in the chart above, the company’s revenue increased dramatically in the initial years (2010-2015) aided by celebrity endorsements, but since then have been on a downward trajectory as the focus of the new management has shifted to profitability and cash flows.

We note that the MuclePharm’s stock traded at a high of $14 in 2014 before the scale of losses drove investor interest away from the company. It currently trades at $0.56, and while the sales have gone down significantly, the company has turned the corner into the green and is on track for sustainable long-term profitability. Below are our brief reasons for trascking MSLP.

Reasons for Tracking MSLP

Restructuring initiatives generating positive results: As discussed above, the management team has been actively pursuing restructuring of the business and the efforts seem to be paying off as the company delivered healthy Q320 profitability numbers. Even for the nine months of 2020, the profitability has improved dramatically. Some of the initiatives include: 1) Reducing product discounts and promotional activity; 2) Cutting down on low margin SKUs, 3) Reducing operating expenses and 4) focusing aggressively on the cost of goods sold (COGS) through better sourcing of raw materials to improve gross margins.

Nine months ended September 30,2020 versus nine months ended September 30, 2019

- Gross margin improved to 30% compared to 9.9% a year earlier

- Adj. EBITDA was $2.4 million compared to a loss of $11.6 million

- Diluted EPS of $0.01 versus a loss of $(0.94) per share.

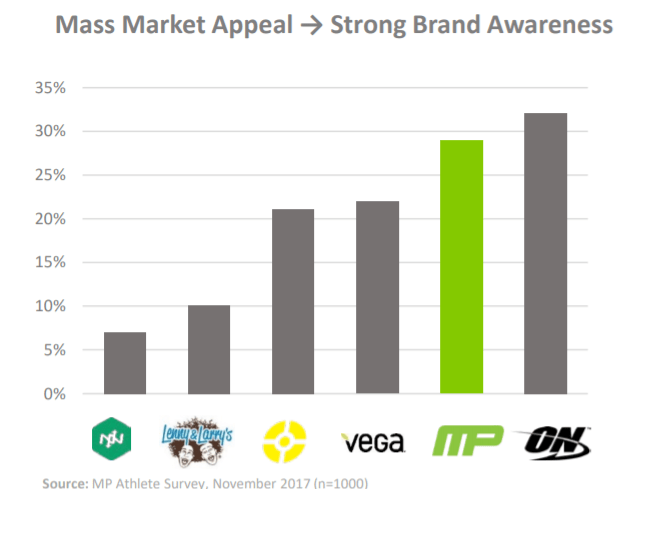

Strong brand equity: MusclePharm is among the most ubiquitous names in sports nutrition, with nearly 1.5 million social media fans (across facebook, twitter and Instagram). This is significantly higher than some of the other major brands in this category, such as CLIF, Musclemilk, and KIND. Also, MSLP boasts of much higher brand awareness compared to other peers (as shown in the figure below). This validates its mass market appeal.

Strong distribution network: MusclePharm products are sold in over 100 countries and available in major U.S. retail outlets that include Costco, GNC and Vitamin Shoppe, as well as overall major online stores, including Amazon, iHerb and Coupang Global.

Large market opportunity: There is a clear trend towards a healthier lifestyle among the people. The pandemic has highlighted the need for people to consume things which are nutritious and healthy. The global nutritional supplement market is expected to reach $241 billion by 2026, growing at a CAGR of 8.3% during 2019-2026. The market will be driven by the rising awareness of preventative healthcare, growing disposable income, and the availability of more dietary nutrition products.

Valuation

MSLP is trading at 0.4x TTM EV to sales which is not too demanding considering the turnaround in profitability and solid growth outlook for the nutritional supplement industry. Many similar businesses are now trading at premium valuations given their strong branding. MSLP might be able to recreate that. In general, the last decade has placed premium valuations on brands and MLSP is one of the few publicly traded pure play brands in its industry.

Caveats:

- A slower than expected vaccination drive could delay the return to normalcy and impact retail sales

- The stock is illiquid

- Due to history of losses and negative cash flow, there is doubt on the ability to continue as a going concern. There is risk of a dilutive equity raise if the company does not maintain profitability and/or if it has difficulty refinancing short-term debt of $6mm.