Firstime Design Limited (OOTC:FTDL) designs, markets and distributes home decor and sleep environment products. The company operates via its two subsidiaries – FirsTime Inc, which focuses on home décor and InnerSpace LLC, which is focused on commercial mattresses and bedding accessories. These products are sold through major national retailers and e-commerce channels. Here is a history of GeoInvesting’s coverage on FTDL:

- On January 21, 2014 – We offered a brief reason for tracking note.

- On January 27, 2015 – After a weak Q4 2014 results we removed FTDL from our radar

- On July 24, 2017 – The stock came back on our radar after it announced an acquisition of InnerSpace and a stock repurchase was announced.

- On October 20, 2020 - We covered its Q3 2020 results and posted a brief note on it.

- On November 3, 2020 - We added FTDL to our disclosed long list after a strong interview with management

Quick Facts – As of 01/20/2021

|

Share Information

|

|

Close Price

|

$15.00

|

|

MCAP (m)

|

$17.3

|

|

EV (m)

|

$20.4

|

|

Shares (Basic) (m)

|

1.15

|

|

Shares (Diluted)(m)

|

1.15

|

|

Trading venue

|

OTC

|

|

Financial YE

|

31-Dec

|

|

Key Metrics

|

|

TTM Revenues (m)

|

$18.1

|

|

P/S (x)

|

1.0

|

|

EV/S (x)

|

1.1

|

|

TTM EPS ($)

|

$1.39

|

|

TTM P/E (x)

|

10.8

|

|

Current ratio

|

1.6

|

|

Short- term debt

|

$3.1

|

|

Long – term debt

|

Zero

|

|

BV per share

|

$4.9

|

|

Tangible BV per share

|

$3.7

|

|

Business Activity

|

|

Description

|

Designer and distributor of home décor products

|

|

CEO

|

Christopher Bering

|

|

Headquarters

|

Pewaukee, Wisconsin

|

|

Website

|

https://www.firstime.com/

|

|

Catalysts & key risks

|

|

Potential Catalyst

|

Increasing penetration into online sales

|

|

Risk

|

Slowdown in consumer spending

|

We believe hat FTDL is poised to increase sharply in the near-term and provide multi-bagger returns over the long-term.

Brief History

Firstime Design Limited (OOTC:FTDL), formerly known as The Middleton Doll Company, was founded in 1980 and historically consisted of two business segments – consumer products and financial services. The consumer segment included designing and distribution of:

- collectible dolls

- wall clocks

- home décor products

During Q3 2009, the financial services business was sold. However, prior to the divestiture of the financial services business, the segment was “siphoning” cashflow away from the other segments. This made it difficult to compete in an increasingly challenging retail environment. In March 2010, FTDL sold the collectible dolls business and since then the company has been focusing on home décor products, leveraging its long history in selling quality wall clocks.

Today, FTDL targets two markets – the home décor market and the sleep environment product market. These markets are addressed via its two subsidiaries – FirsTime Manufactory Inc. and InnerSpace LLC.

FirsTime Manufactory Inc

FirsTime Manufactory Inc is primarily engaged in selling home décor products. FirsTime’s products are sold at major retailers including Kohl’s, Bed Bath & Beyond, Bon-Ton stores and more and outsourcing manufacturing operations in 7 countries including the U.S., China, and other countries in Southeast Asia.

FirsTime’s expansion of its product lines have resulted in increased sales and shelf space with its retail customers. Beyond the traditional brick and mortar retail channel, FirsTime is aggressively pursuing ecommerce channels and has had great success growing this channel over the last few years.

InnerSpace

InnerSpace is an online retailer of home décor products and a distributor of mattresses and other related products for the “Over the Road” Truck industry. We believe that both the home décor as well as the over the road truck division provide significant growth opportunities. FirsTime acquired InnerSpace in June 2017 with the aim of leveraging InnerSpace’s significant online presence in the home décor industry and de-risking its business outside the traditional brick and mortar retail channel. InnerSpace has now been fully integrated with the company and its home goods business has now been rebranded and positioned under the FirsTime brand. InnerSpace is generating ~$7 million in revenue split between mattresses and other categories, such as wall clocks, mirrors, wall décor, and armoires. We love investing alongside management teams that are keen on finding new markets for existing products and FTDL fits that bill. Historically, InnerSpace catered to the trucking industry, but FTDL quickly positioned InnerSpace to also market products to the motorhome industry, where the company is fortuitously benefitting from a higher demand for RVs as a result of COVID-19.

CEO and Board Member Become a Perfect Fit

“Businesses of FTDL’s size are shaped by the person at top”- Board member, Andrew Bass, on the CEO of FTDL

When Christopher Bering was appointed as CEO in 2011, the company was in the midst of a restructuring. At that time, the company had one product category, one outsourced manufacturer, and two customers. Bering described this period as “scary times”. Since then, over the course of ten years, FTDL has grown its presence to 7 countries, where it outsources manufacturing, boasts 25 product categories and leases a 200,000 square foot distribution center in the United States. Not only does diversifying manufacturing footprint de-risk the company from a supply chain perspective, but it also will allow FTDL to expand globally when the time is right.

Prior to working at FTDL, Chris was a senior marketing specialist at a graphic design company where he honed his abilities at strategic processes. After starting to work at FTDL, he spent 10 years focusing on improving product offerings and marketing. Bering’s experience at the company made him a perfect choice to be promoted to CEO, where he helped FTDL build a competitive advantage through placing focus on developing superior designed products that are sold at an affordable price. During our conversation with Bering, we were impressed with his obsession on stressing how important the company’s employees are to the business and their role on creating new products to stay ahead in a competitive environment where “copy cats” are prevalent.

Andrew Bass, chairman of the capital allocation committee and director of E-Commerce, has been on the board since 2010 when the company began its restructuring. He was recommended to join the Board by the largest shareholder of the company and has played a pivotal role in turning it around. He has prior experience working as a value investing research analyst for Oakmark funds and North Star Investment Management, where he focused on microcaps. Oakmark funds uses an analytical approach similar to Warren Buffet’s investment ideology where they try to understand the incremental returns of a business and its quality. This experience gives Andrew an edge in determining acquisition targets/pricing and how to optimize the ecommerce business.

Growth is Inflecting

Firstime believes one of its competitive advantages comes from its focus on design. Its distribution and manufacturing are outsourced, which allows it to focus heavily on its designs and costs. To compete in the home décor space on Amazon and other large ecommerce sites, a company is required to have readily available product stocking to avoid stockouts. FTDL’s strong balance sheet has allowed it to increase its inventory balance without needing additional funding. The plan seems to be working.

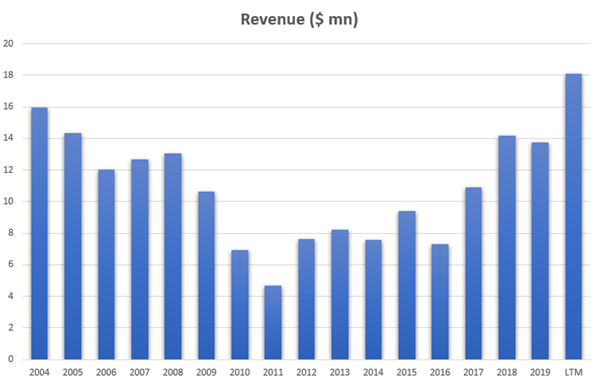

Source: Company data

As seen in the chart above, the company’s revenue had been on a downward trajectory since 2004 and started increasing since 2012 as FTDL’s restructuring initiatives started yielding results.

It now seems that the restructuring efforts plus the accelerated pace of online shopping is taking FTDL’s growth to new levels. The company has posted strong results for the second and third quarters of 2020:

- Q3

- Sales of $6.35 million vs $3.48 million in the prior year

- EPS of $0.67 vs $0.11 in the prior year

- Q2

- Sales of $4.3 million vs $3.0 million in the prior year

- EPS of $0.40 vs EPS of $0.06 in the prior year

FTDL also has significant NOLs comprised of $14 million Federal and $5 million state net operating losses. We do not expect the company to pay meaningful amounts of cash taxes for the foreseeable future, which significantly benefits its ability to generate free cash flow and maintain high returns on invested capital.

The company’s strategy to focus heavily on online sales is plays a big role in its accelerating growth. FTDL is a beneficiary of the shift in consumer purchasing behavior to online channels, which have been accelerated by the COVID-19 pandemic. Even though the company has been positioned to benefit from rising online sales, the pandemic has probably accelerated this trend forward by 2 to 3 years. Furthermore, focusing on the online opportunity has allowed the company to expand its product reach beyond traditional retailers. For example, while FTDL’s legacy products (mainly wall clocks) are well established in brick-and-mortar stores, getting new product categories shelf space within these retailers is not an easy task. However, selling products online gives the company instant access to consumers. Furthermore, FTDL’s management believes it has the infrastructure to provide quality products, at great prices, with fast delivery, which are all key ingredients for success in ecommerce.

Q3 Press Release Verbiage

"we are delighted with the organization's overall performance, both top and bottom line. These results come from years of strategic initiatives that have allowed us to take advantage of the shift in consumer spending patterns. The diversification of our customers, and the increase in our eCommerce presence, combined with our global manufacturing base with locations in China, Egypt, Italy, Vietnam, Taiwan, India and the USA, has allowed us to successfully overcome the supply issues from COVID-19. I am also very excited to announce the opening of our new West Coast distribution facility. This location complements our already diversified distribution capabilities in the Midwest and East Coast. This new facility allows us to get our products to market expeditiously which is critical to our continued success. I am enthusiastic about the Company's operational positioning, which has taken several restructurings over many years to complete.”

Large Addressable Market

Estimates show consumers will spend $20 billion this year on furniture items

The U.S. home decor industry generated $125.8 billion in 2019, and is expected to grow at a CAGR of ~8% during 2020-2027 to reach ~$159 billion, according to Allied Market Research. The home decor market in the US is experiencing a secular shift from brick and mortar to online. The pandemic has forced consumers to spend online and we think this trend will stick well beyond 2020. Customers love the ease and simplicity of online shopping and will continue to use it as their primary and preferred shopping method in the future.

Also, with the rising work from home trend, consumers are spending more time in their homes than ever before. This has resulted in a shift in spending from travel and entertainment to enhancing their homes. We see this trend persisting.

According to data released by the U.S. Census Bureau, there are ~69 million households in the U.S. with annual income between $50,000 and $250,000. Moreover, there are approximately 72 million millennials (individuals between the ages of 20 and 37) in the U.S., many of whom are accustomed to purchasing goods online. As millennials age, start new families, and move into new homes, we expect online sales of home goods to increase.

Regarding the trucking industry, the demand for related furniture is getting stronger as we move more to an online delivery economy. There are about 2 million semi-trucks in the U.S. and the market is growing in mid-single digits, where truck drivers drive about 140 billion miles a year. The market is dominated by several large players, but there are thousands of smaller companies involved in the less-than-truckload market. There were about 350,000 semi-trucks produced last year, and the average semi-truck needs to be replaced every 15 years. Also, $791.7 billion dollars in revenue was generated in the trucking industry in 2019. All told, there are over 3.5 million people working as truck drivers in the U.S and almost half of truckers work longer hours. Furthermore, the truck driver workforce is becoming younger and more educated which should lead to a greater desire to staying healthy and feel at home, while on the road.

Caveats:

- The stock has risen sharply in 2020, up over 320%.

- Growth prospects are tied to consumer spending. Any economic downturn or recession due to the ongoing pandemic could adversely impact the business.

- FTDL is exposed to the fortunes of the retail industry which is undergoing rapid change. Competition from specialty stores and by online retailers is increasing, with the rise in e-commerce. This could adversely affect business operations.

- Quarterly results may exhibit seasonality

- The stock is extremely illiquid

Valuation

We see multi-bagger returns over the long run. However, we believe that FTDL also has some nice upside in the near-term, even though the stock is up about 453% over the last year. We looked at 15 stocks trading in the U.S. in the furniture retail and manufacturing space of varying sizes. P/Es ranged from around 15 to 30, compared to FTDL selling at a trailing twelve-month P/E of 10.8. So, based on this observation, we believe that FTDL has some nice upside potential in the short run. When you also consider that FTDL has a clean balance sheet and is focusing heavily on its online business, we feel that FTDL can trade at the higher end of this valuation range.