GENERAL BACKGROUND INFO

$AIFS was founded in 1950 and first went public in 1969 as Auto-Graphics Inc. and traded under the ticker AUGR. In 2004, AUGR file Form 15 with the SEC and “went dark” – the company terminated the registration of its common stock and suspended its reporting obligations. This termination became final in August of 2004.

In 2010, Agent Information Software, Inc. was formed with Auto-Graphics Inc. as a wholly owned subsidiary. The company now trades over the counter under the ticker AIFS.

AIFS develops information and data management solutions that are standards-compliant. What does this mean? In addition to any laws and regulations related to data management, each industry has developed unique standards related to how business is done. AIFS largely serves the library and research community. Within that space there are certain standards that have been developed relative to information retrieval, re-purposing, storage, metadata, preservation, etc. The products that AIFS develops are compliant with all major library industry standards and in fact AIFS is an active participant in several NISO and ISO standards committees. The company has participated in the development, testing, and implementation of standards used today throughout the industry.

AIFS also offers other technological features; one of my favorites is geolocation IP authentication. This allows a user to access library or research materials instantly and remotely from anywhere within a defined geographic region, without the need for a traditional library card for authentication. What a cool feature. Additionally, AIFS products and services are 508 compliant -- they are accessible and have features that support accessibility. This is important for federal contractors.

PRODUCTS

Ok. So let’s talk for a little bit about the various products offered by AIFS. These products are offered under the Auto-Graphics name. All of the Agent software platform runs in a standard browser and doesn’t require client software to be downloaded or installed. This allows the user to access all tools from any internet-connected device.

Below are short blurbs about each of the main products offered by Auto-Graphics. FYI, this information came from the company website.

There are four pillars to the Agent software platform:

- SHAREit – a patron initiated, library managed, consortium administered resource sharing program. SHAREit’s open platform has provided a tremendous advancement over the past 25 years with the development of cloud-based resource sharing back in 1994. SHAREit facilitates the inter-connectivity of disparate systems, providing consortia the ability to simultaneously interface with multiple ILS and ILL systems. SHAREit interoperates with all major resource sharing systems, including OCLC WorldCat resource sharing, ILLiad, Tipasa, and Relais.

SHAREit helps libraries significantly reduce the amount of staff time spent on managing, borrowing and lending activities, greatly improving staff workflow, and patron satisfaction, while reducing acquisition costs. SHAREit supports and manages staff-initiated ILL transactions plus mediated or unmediated patron-initiated ILL transactions. Libraries with different local ILS and ILL systems have the ability to share resources with one another, regardless of their collection size or automation system.

- VERSO – a powerful integrated library system (ILS) for library management. The VERSO Integrated Library System is designed for library systems of all sizes and configurations, ranging from small, part-time, one-building libraries to multi-branch city or county systems, to multi-library regional and statewide consortia.

VERSO is part of Auto-Graphics’ library management platform, an integrated family of products, enabling libraries to manage, search, and share their resources. Serving over 6,000 library customers, the library management platform delivers proven, standards-based library automation solutions.

VERSO is built on a modular structure, allowing libraries to pick and pay for only the services they need to manage their libraries best. Rather than forcing libraries to fit into rigid system requirements, VERSO can be configured to meet every library’s unique needs.

- MONTAGEdc – a digital collection solution. MONTAGE is a fully hosted, affordable digital collection solution which is available on an annual SaaS subscription. This tool allows the user to: quickly create a custom digital collection landing page for public access; set up unlimited sub-collections; establish private-access digital collections; create institutional archives and multi-lingual collections.

- RESEARCHit – a robust federate search solution. RESEARCHit enables researchers to simultaneously search across multiple content resources and view a combined result set. Users are guided toward quality, authoritative resources, and away from the ‘unfiltered’ results obtained through the open web. Library staff can simplify searching for their end-users by configuring databases into category-based groupings to improve the speed and quality of information discovery.

RESEARCHit is available as a stand-alone tool or as an integrated module as part of the Agent Software Platform within VERSO or SHAREit.

THE LIBRARY MARKET

The Agent software platform is currently used by over 11,000 libraries in North America. Statistics on the number of libraries are surprisingly hard to come by, but based on surveys conducted over the last 10 years or so we can safely say there are somewhere in the neighborhood of 110,000 – 120,000 libraries in the United States. This includes all different types of libraries: public libraries (central buildings and branches), academic libraries (four-year institutions and others), special libraries (corporate, legal, religious, etc.), government libraries, armed forces libraries, and school libraries.

AIFS has penetrated approximately 10% of the total U.S. library market. There are huge numbers of libraries that have not implemented any sort of central ILS to manage their collection and interactions with outside institutions and are instead running off a disparate mix of outdated and home-brewed solutions. There are lots of reasons for this, not the least of which is budgetary as libraries are constantly fighting for dollars but suffice it to say that there exists plenty of opportunity to grow the current customer base for AIFS. For reference, the worldwide total number of libraries is somewhere around 2.6MM.

WHAT’S THE STORY?

AIFS has been providing standalone solutions for decades. Over the last several years, the company has not only focused its product line on library services (the firm had a subsidiary serving the legal industry until a few years ago) but has also modernized and upgraded the user experience. This allows AIFS to provide a simplified and streamlined user experience while also giving the company the necessary capabilities to scale and serve highly-complex institutions.

I went back and read shareholder letters from the past decade or so and it’s clear that the company has been focused on this transition. The letters also paint the picture of a company that recognizes changes that are happening or will be happening in its industry and is not afraid to make investments in order to remain competitive and try to stay ahead of the curve. Read on for some examples of what I mean.

In 2010 the company was actively working on upgrading software in order to be able to meet the needs of more complex and sophisticated customers and was selling a large piece of new business under the SaaS model. In 2013 AIFS made the decision to have the financials audited rather than simply reviewed as they had in the past. This meant that the previous year also needed to be audited. This obviously presented an increase expense in both dollars and time for the company but it was a good move as it demonstrated the boards commitment to driving shareholder value and improving the company’s position in the marketplace. That same year AIFS began converting the user experience software from Adobe to HTML5. Previous investments were also paying off as larger and more sophisticated clients came on board (Tennessee, Massachusetts, British Columbia). In 2014 the move to a SaaS model and the associated recurring revenue was starting to pay off: by the time the shareholder letter came out in March 2015, AIFS had already grown recurring revenue for 2015 by about 9.5% from year-end 2014. The move to SaaS and the newly upgraded platform and user experience helped AIFS make it through a tumultuous year for the industry (lots of M&A activity) and come out the other side stronger. During 2016 the company invested in the development of two new programs: a mobile app and SLIMS which is a small public library software system. In 2019 the company transitioned from a private cloud facility to Amazon Hosted Web Services and hired a new CTO, in addition to dealing with workers transitioning to work from home status due to the COVID-19 pandemic.

To my way of thinking the story is this: AIFS has been around for a long time and has always been private or very tiny. In recent years the company has taken steps to increase its competitive position, product mix, and refined its approach to customer service. By moving to a largely SaaS/recurring revenue model, AIFS has increased profits while containing and reducing costs and also improving the experience for the end user. That said, AIFS largely serves a somewhat niche industry with budgets that are always at risk of being cut.

WHAT ABOUT THE NUMBERS

Here’s the deal: AIFS is a small company. Tiny. At 2019 year end, there were 4,424,527 shares issued and outstanding trading at $2.25, giving AIFS a market cap of not quite $10MM.

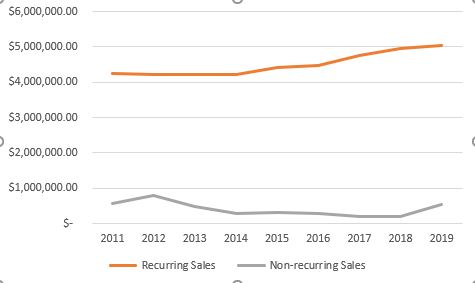

For the years 2011 – 2019, the below chart shows recurring revenue vs. non-recurring revenue:

Non-recurring revenue has been essentially flat over that period and will likely stay flat, relative to recurring sales. This represents items such as licensing fees, installation, training, etc. – income that is associated with the sale of software and often supports the initial onboarding of clients.

What we see from this picture is that recurring revenue really started growing in the 2014-2015 period and has continued to grow, from a little over $4.2MM in 2011 to just over $5MM in 2019.

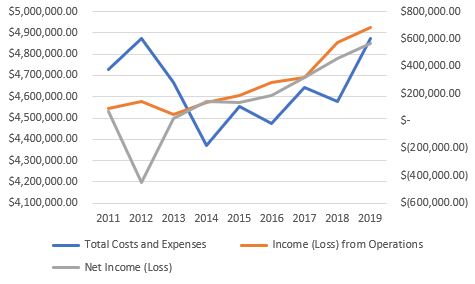

During that same period total expenses only grew by about $150,000 (from $4.72MM to $4.87MM), meaning that there’s been meaningful growth in income from operations and also bottom line net income. Income from operations and net income grew from $88,604 and $69,871 in 2011 to $687,715 and $564,420 in 2019. Here’s total expenses (left axis) and income from operations and net income (right axis):

As we can see for our period in question, expenses are generally flat (took a big dip and have climbed back to 2011 levels with the associated increase in sales), and income and net income are growing. In 2012 the company took a large charge in conjunction with shutting down the line of business supporting the legal industry. This was a money loser and as we can see, once that division was shuttered, income kept on chugging up and to the right.

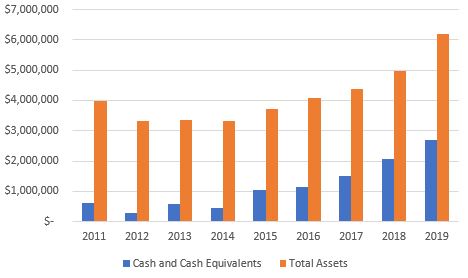

So what’s been happening with the increase in income? What’s the company doing? Well one thing is paying a dividend. AIFS paid out $110,614 in dividends during 2019. Additionally, the company has been beefing up the balance sheet. In 2011 there was $610,536 in cash on the balance sheet and at the end of 2019 AIFS had $2,678,652 in cash on the balance sheet. Here’s a chart showing cash and cash equivalents relative to total assets:

Total cash is growing. The only other major asset category is net software – management has classified software as an asset and amortizes the asset accordingly.

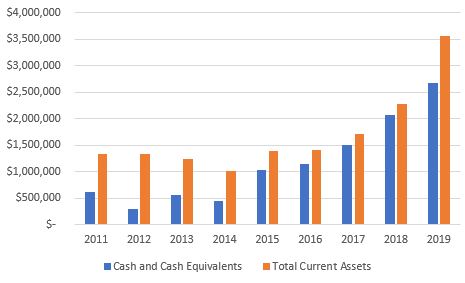

If we look at the same period and substitute current assets for total assets, this is what we see:

Cash is the dominant portion of current assets. In fact the only other components of current assets are A/R, which is meaningful but not huge given that most revenue is deferred as a result of the subscription model most customers are on, and income tax receivable which is not a huge number.

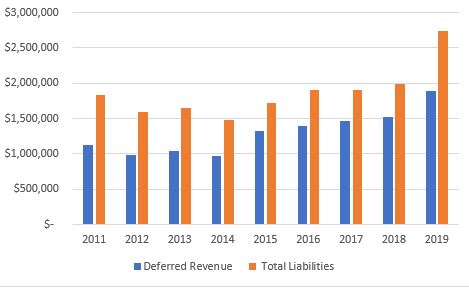

What’s more, the company has virtually no debt. The only long-term liabilities are for deferred taxes in the amount of $267,000. There are some minor short-term liabilities such as A/P, accrued payroll, etc. but really the bulk of the liabilities on the balance sheet represent deferred revenue. This is to be expected when a company derives much of its revenue from a SaaS model. In 2011 deferred revenue was right around $1.1MM and at the end of 2019 deferred revenue was almost $1.9MM. Take a look at deferred revenue relative to total liabilities:

Deferred revenue makes up the lion’s share of total liabilities and the balance consists of various items including accrued payroll liabilities, A/P, and deferred income tax liabilities. No line of credits due, no long term notes, etc. It’s a healthy balance sheet if I’ve ever seen one.

All told, EPS grew from around $.02 in 2011 to around $.13 in 2019 (6.5x). During that same period the price of the stock went from $.20 to $2.25 (11.25x). So perhaps the stock got a little ahead of itself, but still relatively cheap in my mind.

WHAT’S IT WORTH?

Now we come to the million dollar question, so to speak. How to figure out a reasonable valuation for this company? AIFS is certainly a software company, providing a SaaS solution and the bulk of its revenue as recurring revenue. Should they be valued like a high-flying Saas company, at something like 10x-30x revenue? No that doesn’t seem quite right. AIFS is growing but it’s unlikely that this company will ever see the kind of growth that Zoom or Shopify or Twilio has seen. Remember, AIFS operates in a rather niche market.

Should AIFS be valued purely as a function of earnings? 2019 EPS of $.013 vs. closing share price of $2.25 puts them at a P/E of 17.3. That seems sort of reasonable but maybe not a great way of valuing the company.

I think a hybrid approach makes sense. AIFS is expanding their client base and capturing more and more recurring revenue. This revenue, in this market, tends to be quite sticky. Once a library system or government entity or university adopts AIFS products and services, switching is not easy and the costs can be significant. That fact combined with the ease of use of AIFS’ products and the seamless integration into industry tools means that customers tend to stick around. I also anticipate more adoption of the mobile app and capabilities. Even as COVID restrictions are eventually lifted and people are more comfortable gathering in public places, I don’t anticipate that libraries will see the same traffic as they did in the past. That said, AIFS products are well-suited for the digital age and for supporting remote work and remote schooling and remote research. All of that to say, I think a conservative revenue multiple can make sense here, maybe something in the neighborhood of 3-5x.

If you found this company in 2011 and recognized the shift that was happened and bought in at $.20/share, then congratulations! You did great. You bought a growing company at something like .1-.2 EV/Rev. If you waited until 2019 and bought in at $2.25/share, you still did pretty good getting in at EV/Rev of less than 2. In my opinion, EV/Rev of something like 3.5x – 4x probably makes sense and I think we could see that in the next couple of years, maybe by the end of 2022. From the 2019 year end numbers, this would represent a share price in the neighborhood of $5 or so, maybe a little higher.

Will the market recognize that kind of a multiple? I’m not sure. This stock is quite illiquid and as I mentioned earlier that are only 4.4MM shares outstanding. Realistically I think this stock can run to $4 based on some reasonable revenue projections and then there’s a lot of grey area that will depend on management’s ability to execute and on how well the sales team does.

Here’s my disclosure: I do own shares in AIFS. I started buying in around $1.90 or so.