By Maj Soueidan, Co-founder GeoInvesting

$IAIC is a provider of information technology services to the private sector as well as government clients. The company generates its revenue from selling third party software and fees from programming/project services performed by its employees.

A recent video pitch I did on IAIC touched upon the company's tier one characteristics, the company's momentum, catalysts and caveats to the story, as well as GeoInvesting's coverage history on the company, outlined in the bullets below:

- January 16, 2018 – We disclosed a long position in IAIC and concurrently added it to our Run to One portfolio a price of $0.47

- August 17, 2020 - We pointed out information arbitrage contained in the company’s Q2 2020 SEC filing hinting that the company could be at inflection point of sustained revenue growth and profitability. This sentiment was based on a 7-year government agency contract award that is expected to add meaningful annual revenue and boost profitability.

Quick Facts – As of 10/19/2020

|

Share Information

|

|

Close Price

|

$0.67

|

|

MCAP (m)

|

$7.5

|

|

EV (m)

|

$7.1

|

|

Shares (Basic) (m)

|

11.2

|

|

Shares (Diluted)(m)

|

11.2

|

|

Index: Public

|

OTC

|

|

Financial YE

|

31-Dec

|

|

Key Metrics

|

|

TTM Revenues (m)

|

$12.1

|

|

P/S (x)

|

0.6

|

|

EV/S (x)

|

0.6

|

|

TTM EPS ($)

|

-$0.04

|

|

TTM P/E (x)

|

NM

|

|

Current ratio

|

2.4

|

|

Debt

|

$0.5

|

|

BV per share

|

$0.1

|

|

Tangible BV per share

|

$0.1

|

|

Business Activity

|

|

Description

|

Information technology services

|

|

CEO

|

Sandor Rosenberg

|

|

Employees

|

21

|

|

Headquarters

|

Fairfax, Virginia

|

|

Website

|

https://www.infoa.com/

|

|

Catalysts & key risks

|

|

Potential Catalyst

|

Increase in IT spending on modernization of legacy IT and database structure

|

|

Risk

|

Delay in projects and cut in government budgets

|

Brief History

Founded in 1979, IAIC uses software and its full-time programmers to modernize legacy/outdated IT systems. Most of the company’s revenues are generated from the U.S. federal government and state and local governments, but commercial markets are also being pursued.

IAIC specializes in:

- Converting mainframe and on-premises IT solutions to modern solutions (Windows, Unis7, Linux) and to the cloud

- Helping customers adopt electronic forms solutions

- Upgrading data base infrastructure and data gathering / analytics capabilities using Oracle’s software and database solutions

- Staffing services to the Government

The first two items above appear to account for most of IAIC’s revenues.

IAIC entered GeoInvesting’s radar during one of our December 2017 earnings press release research sessions, when we noticed that the company reported strong EPS growth. Shares were trading at $0.38 back then, but fell to as low as $0.08 in October 2019 due to the delay in the receipt of some government contracts.

On par with many Tier One microcap turnaround stories we’ve focused on in the past, IAIC boasts a long operating history. The company was founded in 1979 by Sandor Rosenberg, who has served as its CEO during IAIC’s 41-year history. Other members of the senior management team have also been with company for a long time (nearly 20 years or more). The company has kept a relatively low profile over the last few years, rarely issuing press releases, giving investors a chance to find information in its SEC filings before the crowd.

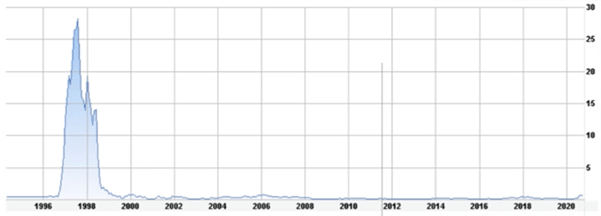

IAIC has mainly focused on securing government contracts, which as you might know, can experience commencement delays and lumpiness (a risk that we are willing to accept with an investment in the company). As a result, IAC’s growth has been unexciting and the stock has underperformed for most of the company’s tenure as a public company, barring the 1999/2000 dot.com pump period where software stocks rocketed, before coming down to earth when the bubble burst.

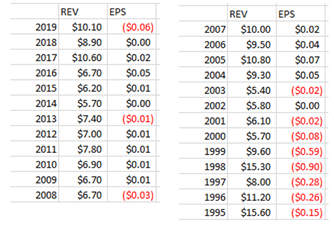

IAIC has been struggling to grow revenue and net income for years However, during the last couple of years, the company has experienced a minor uptick in revenue. The company’s revenue has generally been in the range of around $5 to $10 million since 1995, while EPS has been dancing around break-even since 2008.

Tides Are Turning

Now, we believe the story is poised to improve. IAIC reported Q2 2020 revenue of $4.8M, up 30% YOY, which is its highest quarterly revenue performance since 1998. The Q2 2020 revenue performance was also up 129% from Q1 2020 revenue of $2.1 million. This was primarily due to the company beginning to service a large federal government agency contract which had been delayed due to a protest from the incumbent who eventually lost the contract to IAIC

In April 2020, the incumbent withdrew the protest, paving way for IAIC to commence work on the contract. However, the changing fortune of the contact award news was initially only disclosed in the company’s Q1 and Q2 2020 SEC filings before eventually being disclosed in a Q2 press release.

The coronavirus pandemic had also impacted the commencement of services under the new contract for a few months, with IAIC finally starting project work on June 1, 2020. The new contract is part of a government modernization program to be carried out over a 7-year term and is potentially worth $25 million, which will enable the company to generate a healthy base of consistent profitable revenue for several years, serving as a basis from which it can grow.

Summary of Q2 filings indicating that project work is recommencing:

“IAI has been experiencing prolonged delays in the commencement of new professional fees contracts and subcontracts due to protests and now coronavirus. The largest of these contracts, originally delayed due to protest and subsequently delayed due to indirect effects related to coronavirus, commenced on June 1, 2020.

In April 2020, we were made aware that the incumbent withdrew its subsequent protest, thereby confirming the initial contract award to our prime contractor. The coronavirus pandemic indirectly impacted the commencement of services under this contract for a few months, but we finally commenced providing services under this seven-year subcontract award on June 1, 2020. We anticipate net income in the third quarter due to the increase of our professional fee revenue we are experiencing under the commencement of new contracts.”

Q2 Press Release Verbiage

“There is no doubt about it - 2019 was a tough year,” said Sandor Rosenberg, Chairman and Chief Executive Officer of IAI. “Contracts were expiring in normal course, but every material new contract and subcontract we won was delayed due to protests by companies competing for the business. Despite managing our offices and employees through ever-changing directives and regulations due to the COVID health emergency, we turned the corner during this second quarter, as the largest of these delayed subcontracts emerged from protest almost a year after it was originally won. In June we were able to commence a massive modernization effort at a federal agency that could be worth upwards of $25 million over the subcontract’s seven-year term. With the addition of this effort, we expect our third quarter to be profitable, and we should remain so for the foreseeable future.

Potential Margin Expansion

Gross Margins

The company has two main sources of revenue – third party software license revenue, and professional fee revenue. Software sales have 3 components:

- sales of third-party software licenses and implementation and training services

- sales of third-party support and maintenance contracts based on those software products

- incentive payments received from third-party software suppliers for facilitating sales directly between that supplier and a customer introduced by the Company

Professional services consist of “developing and maintaining IT systems for government and commercial organizations” (programming, database structure and project management).

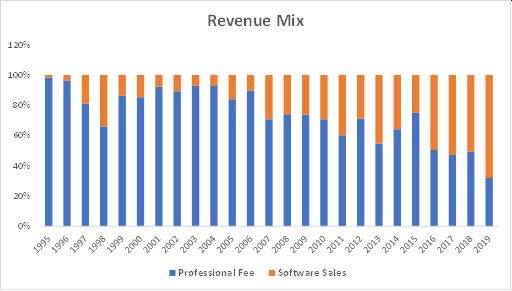

Typically, professional fees have accounted for the majority of revenue until 2016, after which they started to decline.

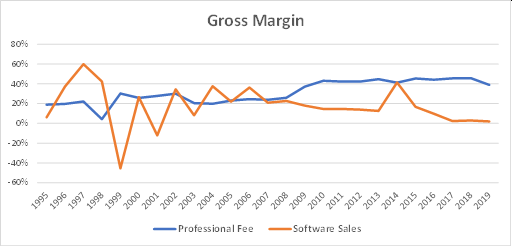

The gross margins on the software revenue have been quite volatile and are currently near historical lows, sitting under 3% since 2017. Compared to this, the professional fee gross margins are much higher and more stable, ranging from 20% to 45% range. It’s nice to see that professional fee margins have been holding at around 40% since 2009.

It appears that the new $25 million contract revenue will mainly consist of high margin professional fees which would give a big boost to overall operating margins and profitability.

“IAI has been experiencing prolonged delays in the commencement of new professional fees contracts and subcontracts due to protests and now coronavirus. The largest of these contracts, originally delayed due to protest and subsequently delayed due to indirect effects related to coronavirus, commenced on June 1, 2020.”

As such, we anticipate a profitability bump starting in Q3 2020 and for the company to remain comfortably profitable for some time.

Furthermore, I see the possibility that software margins could materially increase from the low range at which they currently sit if the company can start inking new contracts, which have higher margins than contracts in their later cycles of implementation. Imagine a double whammy, where IAIC generates more professional revenue and sees its software margins rise back to 20% for a period of time!

Overall Operating Margins

Aside from a potentially better gross margin profile as a result of the new contract win, Q2 highlighted that IAIC experienced a tremendous amount of operating leverage with expenses decreasing 25%, even as sales rose 30%.

Reduce Dependency on Third Party Software

If the company takes steps to develop and sell its own software solution, software gross margins could increase from the less than 3% range to well over 50%. I do not know if the company is going this route since Oracle plays a big part in their project work, but I did bring it up in a conversation I had with management.

Reduce Dependency On Subcontracted Work

A good deal of IAIC’s contract wins comes through subcontracted work. Going after contracts directly would allow IAIC to capture more margin.

Penetrate Commercial Markets

The company generates the majority of its revenues from government agencies. As of Q2 2020, US government agencies generated 79.3% of IAIC’s revenue, subcontracts under federal procurements generated 19.9% of revenue, and commercial contracts generated 0.8% of revenue. I need to gain a better understanding of the commercial market opportunity, but I presume it would come with more favorable and predictable margins.

I also need to learn more on the growth potential of the company’s staffing and electronic forms business and what that could mean for margins. I am also intrigued that the company mentions robotics process automation in its SEC filings as a potential market.

Government Agencies Will Have to Stop Dragging Their Feet

Another key driver of growth and profitability for IAIC is the increasing focus on the modernization of legacy IT systems by the U.S. government. For years, the sector has suffered from a lack of urgency by government agencies to improve and replace outdated systems.

In recent fiscal years, the federal IT budget has been over $90 billion annually. However, according to Government Accountability Office’s (GAO) 2019 budget document, over 80% of all IT spending is on the Operations and Maintenance of:

"aging legacy systems, which pose efficiency, cybersecurity, and mission risk issues, such as ever-rising costs to maintain them and an inability to meet current or expected mission requirements”

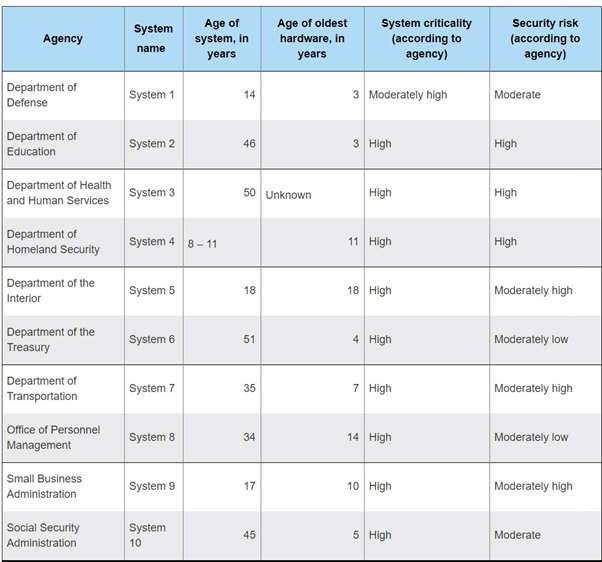

The table below shows 10 critical legacy government agency IT systems ranging from 8 to 51 years old, including those dealing with national security.

The 10 Most Critical Federal Legacy Systems in Need of Modernization

Source: US Government Accountability Office

When will government agencies wake up? I don’t know the answer to this question, but it’s worth noting that the coronavirus pandemic has exposed weaknesses in government agencies’ technology infrastructures like:

- Health care bottlenecks

- Procurement and distribution issues for personal protective equipment

- Processing unemployment claims

- Processing stimulus checks

- Processing SBA and disaster loan applications

Furthermore, trade wars with China and an increasing embracement of protectionism around the globe should help bring to light the importance of maintaining key technology government infrastructures.

Overall, I think that federal government agencies, state agencies, and the banking, insurance, and health care industries are quickly recognizing the need to modernize and migrate from their legacy systems.

Products and Services Advantages

“IAIC’s core competencies lies in modernizing legacy systems involving COBOL applications.” This includes migrating legacy assets into modern platforms (such as the Cloud), eBusiness solutions, Oracle Application Development, and custom software development. The revamping of legacy systems allows clients to reduce operational and maintenance costs resulting in yearly cost savings.

“With our recent large-scale modernization successes, especially with regard to aging COBOL-based systems, we are poised to pursue and win opportunities with the federal government, as well as efforts to modernize and enhance state and local data systems and large-scale commercial systems. We make an excellent teammate when tackling multi-faceted modernization efforts.”

So far, IAIC has performed IT modernization and electronic forms conversion projects for over 100 commercial and government customers, including:

- Department of Agriculture

- Department of the Air Force

- Department of the Army

- Department of the Navy

- Department of Health and Human Services (Grants.gov)

- Defense Finance and Accounting Service

- Defense Logistics Agency

- Department of Homeland Security (ICE, USSS, HQ, USCIS, CBP)

- Department of State

- Department of Treasury (IRS, FMS, FINCEN)

- Department of Veteran Affairs

- State of Maryland

- State of West Virginia

More importantly, it’s getting increasingly more difficult to find COBOL programmers, which plays right into IAIC’s hands.

"Many IT systems runs on COBOL, a programming language that is rarely taught anymore. It's not uncommon for old IT experts to be called in to deal with COBOL related issues, often at a premium."

You can learn more about some of the company’s modernization work here.

Valuation

IAIC is trading at 0.6x TTM sales which is not too lofty if the company can reach consistent profitability, especially when considering the positive growth outlook management has communicated for the remainder of its 2021 fiscal year and for the foreseeable future. The first valuation boost I see happening is the company’s P/S moving closer to 1x as the company continues to make progress. Eventually, investors should be able to value the IAIC on earnings. However, that time may come sooner than you think. Since the new contract appears to be a professional fee contract, we might be able to assume that associated gross margins will be at least 40%. That revenue alone could equate to annual EPS of $0.10. I think a P/E goal of 15 is a reasonable, leading to a potential price target of $1.50, with plenty of upside if potential new contract awards are received.

Caveats

- The stock has risen sharply over the past few weeks, up over 400%.

- A prolonged economic downturn due to COVID-19 or a more aggressive second wave of infections could delay contracts, thereby impacting sales.

- Growth prospects are tied to government funding for modernization of legacy IT systems. Any reduction in that could adversely impact the business.

- There is no guarantee that IAIC will earn the top end value of the new contract award

- The rising competitive intensity remains a risk. IAIC competes with many large players who are more established and have greater financial resources.

- The stock is extremely illiquid