By Maj Soueidan, Co-founder GeoInvesting

Agent Information Software, Inc (OOTC:AIFS) ($2.39; $10.7M market cap)

***We aded AIFS to our Favorite Model Portfolio on July 26, 2020 with a long-term horizon in mind***

Agent Information Software Inc. is a provider of cloud-based library management and resource-sharing solutions to mainly public libraries in the United States (15) and Canada (1). Here is a history of our overage on AIFS:

- April 8, 2019 – We disclosed that AIFS enters our research funnel

- May 1, 2019 - We disclosed a small starter long position at $1.80, impressed by the company’s recurring revenue model.

“While the company has had a slow growth rate, it’s the company’s recurring revenue model that has drawn us to follow the company more closely. We initiated a small starter position while we continue to try to arrange a call with management to determine if revenue growth can accelerate.”

- May 15, 2019 - We disclosed we added to our starter position based on strong Q1 2019 results.

- August 2019 – We interviewed management

We need to emphasize that even though we are long AIFS, we are currently treating the investment as a long-term play. Although we believe the company will experience consistent growth over the next few years, the growth could be a slow grind. However, we still believe the stock has multi-bagger potential for the patient investors, especially if AIFS surprises us by finding new markets for its software platform.

AIFS will probably not be for everyone. The stock has 4.5 million shares outstanding and float of 1.1 million. Its 6 months daily average trading volume is only 1585 shares. Yet, even though we have not been able to accumulate a large position in the stock, we are adding AIFS to our high conviction model portfolio with a long-term horizon in mind. Short-term performance my depend on how fast the company can penetrate deeper into new and current target markets. The base bullish case is contingent on the company consistently growing 5% to 10% with nearly 100% recurring revenue. The really exciting bullish case is one where the company finds new avenues into which to sell its database/enterprise management software platform.

The biggest caveats we see with the story are that contracts are tied to city, county, state and federal government budgets and that the market segment driving growth is not that large.

Quick Facts (as of 10/4/2020)

|

Share Information

|

|

Close Price

|

$2.90

|

|

MCAP (m)

|

$13.00

|

|

EV (m)

|

$10.90

|

|

Shares (Basic) (m)

|

4.5

|

|

Shares (Diluted)(m)

|

5.1

|

|

Trading Venue

|

OTC

|

|

Financial YE

|

31-Dec

|

|

Key Metrics

|

|

TTM Revenues (m)

|

$5.50

|

|

P/S (x)

|

2.4

|

|

EV/S (x)

|

2

|

|

TTM EPS ($)

|

$0.10

|

|

TTM P/E (x)

|

36.3

|

|

Current ratio

|

1.4

|

|

Debt

|

$0.00

|

|

BV per share

|

$0.80

|

|

Tangible BV per share

|

$0.30

|

|

Business Activity

|

|

Description

|

SaaS Library management services

|

|

CEO

|

Paul Cope

|

|

Employees

|

28

|

|

Headquarters

|

Rancho Cucamonga, California

|

|

Website

|

https://www.auto-graphics.com/

|

|

Catalysts & key risks

|

|

Potential Catalyst

|

Dominate niche market; Find new markets for software platform

|

|

Big Hairy Ass Fact

|

AIFS claims it only faces one main competitor in its niche market

|

|

Risk

|

Loss of customers in its niche market and government budgets

|

Brief History

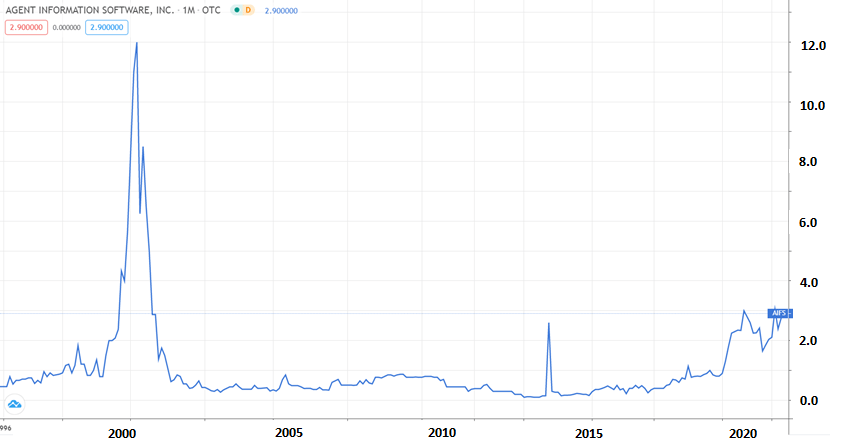

AIFS entered our radar during one of our September 2015 earnings press release research sessions, where the company reported strong EPS growth. Shares were trading at $0.36 and since then, the stock has gradually risen, hitting a high of $3.39 in September 2019.

AIFS, founded in 1950 by the current CEO’s grandfather, went public through a traditional IPO in 1969. Paul Pope has been the CEO since his dad passed the baton to him in 2005. The name Agent Information Software Inc. came about in 2010, but had previously operated under the name Auto-Graphics Inc: Auto, referring to automation and graphics, referring to type setting.

The company initially performed type setting services, but eventually exited the business because it became less specialized as the desktop computer gained popularity, creating more efficient methods of type setting solutions and less of a need for AIFS’ hands-on services. Basically, the industry became commoditized.

So, in the 1970s and 80’s, AIFS started moving into providing solutions for libraries. Initially, it focused on providing data conversion to libraries wherein it provided services to enter data from library card catalogues into databases. This move made sense as the company already had 150 people doing manual typesetting data entry tasks.

AIFS began performing data conversions into microfilm or microfiche, to CD-ROM and later into minicomputers. This gradually evolved to its current library SaaS, cloud based, management software business and helping libraries adopt on-line management and customer service solutions. As you can see, along with other software related stocks targeting the web, shares of AIFS rocketed during the 1999/2000 dot.com pump period, before coming down to earth when the bubble burst.

By 2003, AIFS had exited its non-core business to focus on public library SaaS product lines that I’ll discuss later in this report. The company voluntarily terminated its registration with the SEC in 2004, but began filing financial reports with the OTC in 2014. You might be thinking what I originally thought when I first stumbled upon AIFS in September 2015 and didn’t buy it at $0.35! Where is the growth in the library business? Looking at historical figures, that industry does not look very exciting. AIFS’ revenue has grown from $4.8 million in 2011 to just $5 million in 2019. However, cash and shareholder equity have increased nicely during that same period…

- Cash increased from in 2011 $610,000 to $2.7 million in 2019

- Shareholder Equity increased from $2.1 million in 2011 to $3.5 million in 2019

… and the company has remained solidly profitable, reaching a record EPS of 9 cents in 2019, albeit EPS growth has been a slow grind. The company also initiated an annual dividend in 2018. Finally, gross margins were a mouth-watering 79% in 2019.

Had I dug a little deeper, I would have found that the company has been providing library management and resource sharing software for nearly 50 years. It was also the first company to launch cloud-based resource sharing solutions that libraries use to share book inventories to reduce costs. Furthermore, the company operates a SaaS model, where almost 100% of its revenues are recurring, which ensures revenue predictability.

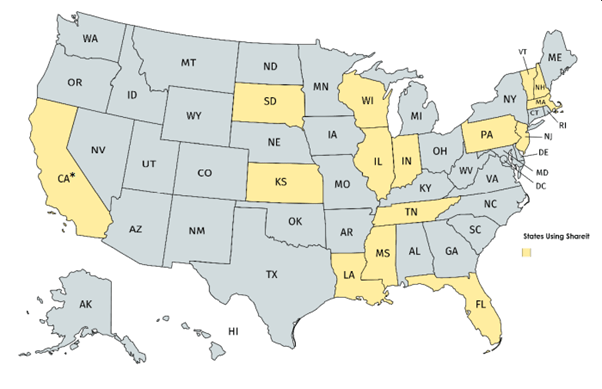

Revenue reached ~$5 million in FY 2019, the first time in company’s history. Around 7000 Libraries (mainly in the U.S.) use AIFS’ software solutions, but we are most excited about their inventory book sharing platform (SHAREit) that has been adopted by 15 states with a runway for the potential of near full penetration into the states that don’t currently use SHAREit. It is becoming apparent to me that even with little growth, AIFS might have some “moatish” type characteristics that give it long-term multi-bagger potential, especially if SHAREit can continue to dominate its market and if management can find new growth markets for its software platform.

Products and Services

AIFS software services help libraries save money. The company’s primary product lines include:

- VERSO, an integrated library system (ILS) that is like an enterprise resource planning system for libraries.

- SHAREit, an interlibrary loan (ILL) management system that allows one library to lend or borrow books to and from other libraries.

AIFS offers its platforms as either a SaaS or on-premises offering. However, most of its customers have switched or sign up to the SaaS platform. Management estimates that only a few legacy accounts are using AIFS as an on-premise solution. Learn about on-premise vs. SaaS solutions here.

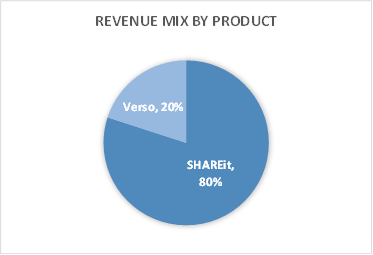

Currently, AIFS derives the majority of its revenue from VERSO and SHAREit

VERSO’s ILS back office solution, an inventory and enterprise resource planning management system, allows them to gain total control of all activities in a library such as:

- What books a library owns

- What books are being checked in and checked out

- Book requests

- Track who is past due

- Collection of fees

If you are old enough, like me, you might remember a time when card catalogues were the status quo for patrons to search for books, and for libraries to track inventory. Now, libraries are taking their management activities on-line and to the cloud. VERSO allows patrons and library staff to create user profiles and allows libraries to track physical books, tablets and audio books checked in/out directly at a library, on-line or through an application that patrons can install to their mobile devices.

In addition, it improves libraries’ abilities to collect fines through phone calls, payment due alerts and even through a credit card that gets dinged once a patron checks in with their library card. It can even accommodate libraries that have adopted bar code scanning technology at checkout, and RFID technology where borrowed material can be tracked as a patron enters or leaves a physical library.

Modernized ILS systems like VERSO that are collecting data and building user profiles also makes it possible to interact with the customer so that they become more active with the library. As great as all this sounds, the company has not been too successful in growing its ILS business.

The issue primarily centers around how the public library funding mechanism works. Public libraries are funded by their home state (although federal funding can also be available) and the state allocates a fixed amount of budget to public libraries that are free to choose their preferred ILS vendor

Let’s say a library is running an ILS system, paying ~$75,000 a year to use it, and that AIFS comes along with an offer to use its ILS platform for $35,000. You would think that the library would jump all over it. However, many libraries do not show any interest to make the switch. Why?

A library is working with a state budget that has to be applied to certain areas, potentially as much as $75,000 to ILS management services. The library is not permitted to apply the difference that could arise from paying a fee of less than $75,000 to other areas like staffing, payroll or large book acquisitions. So, there is no real incentive to switch ILS systems in an environment that is already sticky. You got to love the way government works!!!

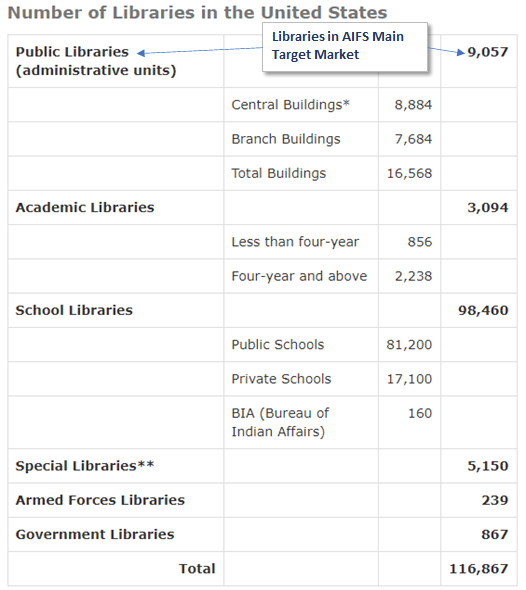

Additional reasons exist that have resulted in AIFS’ lack of growth in its ILS business. The ILS market is almost 100% penetrated. Almost every library has an ILS system in place, many of which are from large and more resourceful competitors. Thus, it is hard for AIFS to replace these very sticky relationships. Large competitors have more features, including the ability to customize services compared to VERSO that is more suited for smaller to medium-sized libraries that require less customization. Currently, VERSO serves around 500 public libraries compared a total addressable market (TAM) of about 5000 to 10,000 small to mid-sized public libraries in a playing field of about 116,000 potential libraries in the U.S.

VERSO generates around $1 million in annual recurring revenue and is growing in the low single-digits annually. Actually, I like that management understands where it stands in the ILS market, allowing it to focus on and retain its core customers, instead of wasting energy on aggressively going after the highly competitive ILS TAM. In fact, AIFS has customers as far back as the 1970s and has only about a 5% attrition rate!

AIFS admits that its attempts to differentiate its ILS offering and gain ILS market share have failed. For example, the company has been unable to gain the market share it had hoped for by lowering its prices, specifically because of the mechanics of the funding process.

Management is still thinking of ways to grow its ILS market share, but in the meantime is putting greater focus on growing its SHAREit’s market share, where it has a clear competitive advantage and where the average selling price for the platform is much higher than for VERSO.

SHAREit – The Big Moat Opportunity

SHAREit is an interlibrary loan (ILL) management system. ILL systems sit on top of ILS. It allows one library to lend or borrow books to and from other libraries and is also referred to as a resource sharing solution. This allows libraries to order fewer copies of each book (5000 vs. 1500 in one case study the CEO shared with me), thereby saving a huge amount of costs to them. The ILL market is where the big moat opportunity lies for the company. AIFS started to use the internet for ILL communication as early as 1994 and was the first company to launch a cloud-based resource-sharing management software solution like SHAREit, in 2000.

So far, 15 states have signed up for SHAREit:

Wisconsin, Kansas, Florida, Vermont, New Hampshire, Mississippi, Louisiana, New Jersey, Southern California Academic Consortia, Tennessee, Massachusetts, Pennsylvania, Indiana, South Dakota, and Illinois

*Southern California Academic Consortia

There are a few reasons I really like SHAREit:

- Moat Characteristic- Purchasing decisions are made by states and not the libraries

- Can save the public library system millions of dollars

- Moat Characteristic- One of only to real players in town

- Moat Characteristic- SHAREit can work with any ILS

How does the ILL system work? No library can afford to buy everything that its patrons might need and this is where an effective ILL system could be of great help. SHAREit allow libraries to search for books across the entire state library network. For example, let’s say you wanted to borrow “One Up On Wall Street”, by Peter Lynch to learn how to find your next multi-bagger stock. Powered by SHAREit, you would use the ILL system to search which libraries have the book. A request to borrow the book is then sent by the ILL to a library that has it in stock. The request could include shipping the book to your local library or directly to your house.

Don’t confuse SHAREit with services like the Libby APP. Libraries can have relationships with e-book services like OverDrive. Libby is an APP that allows you to download an e-book from OverDrive’s inventory. These types of solutions are not nearly as comprehensive as an ILL solution. First of all, it does not search the ILS or other content of the library’s inventory. It only searches the content that the library is getting from OverDrive. Secondly, you can only download content from libraries with which you have a library card.

As a case and point of the savings that a public library can achieve using SHAREit, consider that when the state of Connecticut had used SHAREit, it disclosed that that their annual savings were $3.5 million per year from using SHAREit. AIFS has published some case studies for all of their software offerings here. (Connecticut does not use SHAREit anymore, opting to take the ILL development task in-house)

Here comes the Moat

Unlike ILS and solutions like Libby, where purchasing decisions are made by libraries independent of each other, SHAREit purchasing decisions are made at the state level. Once a state chooses to adopt SHAREit, all public libraries in the state must connect to the system that AIFS helps facilitate, remotely.

But it gets better. I believe that AIFS, as one of the earlier entrants in the ILL market, is well positioned to dominate the ILL space.

AIFS’ major competitors are included in the following table:

|

Name

|

Type

|

Solution

|

Description

|

|

|

|

ILS

|

ILL

|

|

|

OCLC

|

Private

|

Yes

|

Yes

|

It is a non-profit organization which caters to academic as well as public libraries.

|

|

Innovative Interfaces

|

Private

|

Yes

|

Yes

|

Specializes in library management, discovery, and resource-sharing technologies for all types of libraries, It was run by private equity which exited when Innovative was acquired by ProQuest in January 2020

|

|

Ex Libris

|

Private

|

Yes

|

Yes

|

It is leading provider of cloud-based SaaS solutions to libraries, primarily academic. Though it has started to focus on public libraries as well.

|

|

Libsys Ltd

|

Private

|

Yes

|

No

|

Develops software solutions for libraries, academic campus and retail sector.

|

|

Axiell group

|

Private

|

Yes

|

Yes

|

Provides cloud-based library management platform. Its flagship product Axiell Quria which also offers cloud-based resource sharing services was introduced in the US in March 2020.

|

|

SirsiDynix

|

Private

|

Yes

|

No

|

Provides library management software to more than 23,000 libraries worldwide. It serves public, academic, K-12, and special libraries, worldwide

|

|

The Library Corporation

|

Private

|

Yes

|

No

|

Develops software solutions primarily for public libraries and school district library systems.

|

|

Agent Information Software

|

Public

|

Yes

|

Yes

|

It is a provider of cloud web-based library resource management solutions to libraries in the United States and Canada

|

All the major comps have an ILS product offering. Large companies such as Ex Libris, Innovative Interfaces and SirsiDynix dominate the ILS market for academic as well as public libraries. However, as far as the ILL market goes, most of AIFS’s competitors have stopped supporting their ILL systems, don’t target AIFS’ market or have been sold to OCLC, who is basically AIFS’s only ILL competitor. Furthermore, AIFS’ price tag to a state is typically much less than that of OCLC, partly because OCLC also requires libraries to pay annual membership dues on top of the fee they require a state to pay.

A big reason why the ILL public library market segment has not attracted as many players as the ILS market segment is because the vendor is only receiving ILS fees per state, not per library. This compares to a field of over 115,000 libraries in the U.S. that vendors can individually market to use their ILS platforms and other solutions.

Source: American Library Association

Furthermore, while It's harder for AIFS to compete in the ILS market because they would need to displace vendors in a near 100% penetrated market, the ILL public library market is highly underpenetrated or not served with the most optimal solution. About 30 states have an ILL in place, of which 15 use SHAREit. About another 15 utilize a competing resource-sharing platform (OCLC). And 20 do not have an ILL in place. When I spoke to CEO Paul Pope in August 2019, he mentioned that a few states would soon be void of an ILL solution because the vendor providing the service was exiting the ILL market. That is just beautiful and a perfect example of a market being too small to attract large competitors, allowing smaller niche players to potentially capture a leading share of their target market.

It’s also interesting is that even though AIFS has been offering ILL solutions for some time, it’s only been recently that public libraries have been aggressively adopting SHAREit. In fact, over the past two and a half years the company has on-boarded 10 new states to use SHAREit, bringing their total to 15 using SHAREit.

Furthermore, VERSO will cost a public library anywhere from $1,000 to $45,000 per year (average per VERSO customer is about $2,000) year compared to a price tag of $200,000 to $400,000 per year for each state that chooses SHAREit where contracts carry a three to five-year term.

Given the competitive advantage AIFS seems to have in the ILL market and the tough ILS market, it makes sense that AIFS is focussing on growing that business over VERSO. AIFS will have plenty of time to go after the ILS market after it has captured its share of the ILL market.

“Every monopoly dominates a large share of its market. Therefore, every startup should start with a very small market. Always err on the side of starting too small. The reason is simple: it’s easier to dominate a small market than a large one.” – Peter Thiel, Zero To One,pg. 53

So, what is the total potential value of AIFS’s target market?

If all 50 states adopt SHAREit, AIFS could generate $10 million to $20 million per year in very sticky revenue vs. the company’s total TTM revenue of around $5 million, of which $4 million belongs to SAHREit. But there is one small catch: Not all states (~20) have adopted a state-wide ILL system. Still, I am starting to believe that AIFS has a great chance of convincing most of states (15) that are using competing platforms to switch over to SHAREit, which potentially translates into an additional $3 to $5 million in recurring annual revenue. And over time, I feel there is a good possibility that the 20 states with no ILL in place will slowly adopt an ILL which translates into another $4 to $8 million in revenue potential.

However, because the growth per year may not look exciting, I can’t underestimate the likelihood that investors may have an issue buying shares in AIFS, even with all the wonderful long-term ILL revenue it is in position to capture.

So, it’s worth exploring potential catalysts that could convince investors to rerate shares of AIFS to a valuation of a tier one SaaS player, allowing it to trade at an EV/S in excess of 4x to 6x. Shares currently trade at around a TTM EV/S of 1.9x.

Opportunities to Accelerate Growth

To be clear, I do not think AIFS will see its revenue grow much more than 5% to 10% per year in the near term. However, EPS could grow faster. Overall, I think management’s decision to focus on capturing most of the SHAREit TAM is extremely tactical and could open some interesting growth opportunities.

- Canada – Only 1 province in Canada has adopted SHARit, compared to a TAM of 13 provinces, creating the potential for additional annual recurring revenue of $2.6 to $5.2 million.

- VERSO – Only around 500 U.S. public libraries have adopted Verso vs. a TAM of around 9,000 public libraries in its sweet spot and just over 115,000 total libraries. Because states that adopt SAHREit “forces” libraries to start using the platform, an immediate touch point is created with libraries that AIFS may have never had a relationship with. This warm handshake will be perfect for AIFS to market VERSO to them.

- Hardware, such as RFID book tracking devices and scanning technologies, that AIFS could sell into its current customer base.

One very intriguing thing claim that management makes is that AIFS’ software platform is very versatile in that it can easily be expanded to any market that requires the management of data and resource sharing needs. For example, MONTAGE is the company’s digital asset management platform that does not contribute much to revenue.

It is mainly geared to libraries and museums and allows them to share photos, digital documents etc. This is not a material part of AIFS current business. However, this passage in AIFS’s 2019 earnings report is extremely interesting and definitely a new development I need to explore”

“MONTAGE took Auto-Graphics outside the industry with an automotive business, who saw a new direction to use this software and validated our efforts for A-G to take this solution into new markets.”

I am not modelling for any growth from this possibility, but it is worth mentioning since any progress here could translate into a material expansion in AIFS’ valuation multiples. I could easily see a private equity firm getting very excited about this aspect of the story.

More Industry Insight - According to Acumen Research and Consulting, the global library management software market is likely to reach ~$2.2 billion by 2026. Cloud-based library management software is experiencing greater traction, slowly replacing on-premise or legacy software solutions.

The library technology industry has seen significant consolidation over the past decade and will continue to see more activity going forward. A lot of companies have been taken over by private equity, and had a similar revenue level as AIFS. Companies with limited offerings such as standalone ILS solutions will continue to attract capital and interest from larger top-tier players.

Recent M&A

- February 2020 - BiblioCommons acquired by Constellation Software in February 2020

- December 2019 - Ex Libris, a ProQuest company, acquired Innovative Interfaces

- June 2019 - OCLC sold QuestionPoint reference service through a sale to Springshare in a deal valued at $2.6 million in June 2019

- January 2019 - Axiell acquired Bibliotekenes IT-senter, better known as Bibits, and its Mikromarc automation system used by public, school, and special libraries in Finland, Norway, and Sweden (fyi, Axiell has been on an acquisition binge since 2013)

A 2015 article discusses smart library trends and gives a good deal of attention to AIFS’ history and solutions.

“Auto-Graphics, though a relatively small company, has been in business longer than any of the others in the library technology industry.”

“Increasingly libraries in consortia expect technologies that enable unmediated requests for materials by patrons of their partner libraries and automate the management. Without adequate technology support, high volumes of interlibrary lending can be cumbersome for library personnel and too slow for patrons.”

“The genre of resource sharing technologies has only a very small number of products available (only 4 as of 2015).”

Valuation

let’s recap some of the moat-type characteristics and customer stickiness that AIFS possesses in its target ILL market:

- Nearly all the revenue is recurring

- Gross Margins are near 80%

- Contracts are longer term

- Low attrition rate

- AIFS is expanding the market

- Once a state chooses SHARit, every public library in the state has to integrate and connect to the platform.

AIFS TTM P/E ratio is ~34, which is not cheap given that AIFS’s growth is not torrid.However, I have learned that P/S and EV/S are better valuation metrics to look at when dealing with high recurring revenue businesses, especially when a company is at least at break even.Still, with a price to sales and enterprise value to sales of 2.3x and 1.9x, respectively, one might expect AIFS to be fairly priced in a low growth scenario.

However, when we are deciding what we should pay for a stock, the question we should sometimes be asking is, what will investors pay for shares 3 years to 5 years from now, instead of what will they pay now? What looks expensive today might look extremely cheap in the future.That’s why I love buying quality boring SaaS stocks trading at low or even reasonable EV/Sales multiples before growth accelerates.

I could not find any pure play public library management software companies. But, what would you pay for a potential tier one SaaS company that seems to have a moat in a niche target market, where upside exists if any number of catalysts occur and where nearly 100% of its revenue is recurring?

What we do know is that a P/S of 2.3x and EV/Sales of 1.9x are lower than where tier one microcap SaaS stocks typically trade (well north of 4x). This offers the potential for an expansion in AIFS’ valuation multiples, given the solid momentum in its ILL business, the underpenetrated ILL market opportunity, extremely sticky revenue, and growth catalysts. So over time, I see considerable upside because I do believe management will find a way to unlock hidden value.

Furthermore, AIFS’ balance sheet is as clean as it gets. The company has zero long-term debt and a healthy cash balance that has been steadily increasing. Furthermore, the company has already paid two annual dividends, with presumably more to come.

Caveats:

- The stock has risen sharply in the last few months (since March 2020), up nearly 100%.

- A prolonged economic downturn due to COVID-19 or a more aggressive second wave of infections could delay new contracts, thereby impacting sales.

- Growth prospects are tied to government funding for public libraries. Any reduction in that could adversely impact the business.

- The rising competitive intensity remains a risk. Specifically, if some of the large players like Libris and OCLC begin focusing on the public library ILL space in the US.

- Even though SHAREit is sticky, customer attrition can still occur.

- Connecticut had once used SHAREit but then opted to build their own system using open source code.

- Oklahoma and Texas dropped SHAREit during the 2015 oil crisis due to budget issues.

- The stock is extremely illiquid