Energy Focus Inc. is a provider of energy efficient Light Emitting Diode (LED) lighting products and an industry-leading innovator of energy-efficient LED lighting technologies and solutions. Here is a history of our overage on EFOI:

- May 2015 - We disclosed a long position at $5.80, based on information arbitrage from the 2015 Q1 conference call transcript, as well as the award of a large Navy contract. The transcript available on Seeking Alpha was not entirely readable, but we were able to obtain a cleaner version from an alternate source. We entered the position with a short-term horizon due to the short-term nature of the contract and uncertainty over the sustainability of high margins attained in the quarter.

- July 2015 - We began locking in gains as the stock had run to $10, although shares eventually reached ~$24, even in the face of a hit piece by The Street Sweeper that echoed some of our concerns.

- February 2017 - James Tu resigned his position as CEO, as the board and James did not see eye to eye on the long-term growth vision.

- December 2019 - EFOI re-entered our radar after GeoInvesting Co-founder Maj Soueidan met Mr. Tu at the December 2019 LD Micro Conference and learned that he returned to the company as CEO after the Board realized that James’ original vision for growth was correct.

- January 2020 - We disclosed a long position in the stock at $0.72

- February 2020 – We added the stock to our Run to One Model Portfolio.

- May 2020 - We added the stock to our Buy on Pullback Portfolio #8.

At first glance, EFOI doesn’t look terribly cheap. The company has lost money for 17 straight quarters and revenues have fallen off the cliff since their record highs of $64 million achieved in 2015. In fact, a few months ago, when the stock was sitting at ~$.20, it could probably have been argued that the company was on the brink of insolvency. Now, at around $1.30, shares are trading at an EV/S of 1.4x, near most of its comps, some of which are making money.

However, we believe that the reappointment of James Tu as CEO in April 2019 has set the stage for a turnaround story that is already playing out, which includes the introduction of new differentiated products, a plan to get closer to customers, and moves that should meaningfully expand the company’s addressable market. The company also shored up its balance sheet by conducting a highly dilutive $2.75 million stock/warrant offering in January 2020. Of course, this occurred immediately after we had purchased the stock a few days earlier.

However, looking back, the company was lucky that it raised money just prior to COVID-19. It’s also fortuitous that EFOI recently secured a Navy contract to more than offset the sharp decline in its commercial LED retrofit business. Overall, we think EFOI is set up for a consistent and strong recovery across all of its product lines and market segments, especially when you consider that the LED retrofit industry is in the very early innings of a long-term growth trend and that a good deal of competitors have exited the market. You can learn more about James Tu and EFOI’s story by listening to a recorded Q&A session Maj conducted with James here.

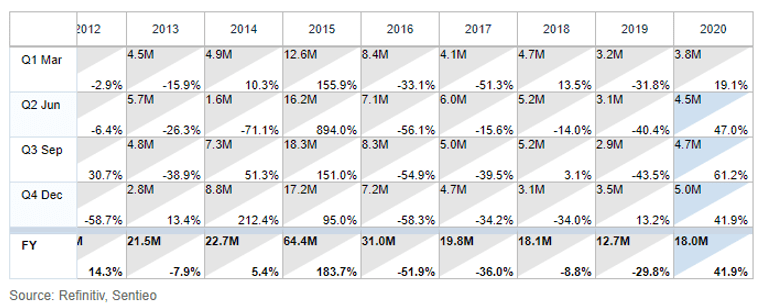

It’s worth noting that Mr. Tu personally invested in EFOI when he joined the company in 2013, just as he did when he joined the company in 2019. Interestingly, EFOI had a stellar run from 2013 to 2016 under his leadership James Tu. During these 3 years, the company experienced significant growth (revenues went up ~7x). This was reflected in the stock price which went up nearly 14x, $1.70 to $23.50, from the beginning of 2013 to August 2015. Here is a look at EFOI’s financial performance since 2012:

Quick stats and facts:

- Market Cap: $20.6 Million

- Shares outstanding: 15.9 million

- Potential dilution: 6.38 million (3.68 million from warrants 2.7 million from convertible preferred)

- TTM revenues: $13.6 million

- Analyst 2020 revenue estimate for 2020: $18.0 million (consensus)

- TTM loss per share: $0.51

- Analyst loss per share estimate for 2020: $0.18 (consensus)

- Current ratio: 1.8

- Debt: 1.64 million (Long-term debt line of credit current portion of long-term debt)

- Book value: $0.38

- CEO: James Tu

- Employees: 42

- Headquarters: Solon, Ohiio

James Tu’s History With EFOI

James first joined the company in late 2012 as its CEO and successfully led a restructuring process to improve the quality of the company’s products and strengthen its long-standing relationship with the U.S. Navy. Upon his arrival, he and some other investors infused ~$13 million into the company. Under Tu’s leadership, the company won a large short-term Navy contract that helped the company achieve peak revenues of ~$64 million in 2015. Still, James was worried that once the Navy contract ended that commercial business model was not set up to grow the company.

Around that time, James voiced his disagreement with the Board on the path the company should take to tweak its business model. He believed that the old way of selling products to its non-government customers through distributors was broken because the rate of change in the technology in the LED lighting industry was occurring at a much quicker pace than in the past.

Thus, distributors would not be able to do a great job understanding the products EFOI was trying to sell. Furthermore, Tu felt that EFOI’s product line-up at that time was not seen as that much different than the competition.

The end result was that the company did not have the brand presence that Tu felt it should have to capture market share. As he predicted, upon completions of the contract, EFOI suffered a significant drop in sales in 2016. Tu continued to argue that the company should think of ways to start building a more direct channel to its end customers, as well as speed up its product innovation efforts, so that distributors can gain a clear understanding of why EFOI’s products are better than its competitors.

Mr. Tu was eventually “relieved" from his position in February 2017. Post the resignation of Mr. Tu, EFOI’s performance fell further. Annual sales declined every year since then and the stock price was decimated from ~$4 in early 2017 to a low of $0.16 in March 2020, before recently rebounding to its current price of $1.29.

Well, amid this poor performance, the Board asked Tu to return to his position as CEO in April 2019. Just as he did in 2013, Tu invested money along with other investors in the company to basically avoid bankruptcy:

“On March 29, 2019, the Company closed a strategic financing from a group of investors (including certain investors that had filed a Schedule 13D with the Securities and Exchange Commission on November 30, 2018). The financing provided gross proceeds to the Company of approximately $1.7 million in exchange for subordinated convertible promissory notes that will convert into shares of the Company’s Series A Convertible Preferred Stock on either April 17, 2019 or the day following the Company’s annual meeting of stockholders, if stockholder approval is needed to allow full conversion of the notes under the Nasdaq market rules. In connection with the financing, the Board of Directors has appointed James Tu and Robert Farkas to join the Board, effective following the Company’s filing of its Annual Report on Form 10-K. Mr. Tu will also return to the position of Chairman, Chief Executive Officer and President and serve as its interim Chief Financial Officer effective April 2, 2019 and the Company is conducting a search for a permanent or alternative interim Chief Financial Officer candidate.

Mr. Tu was one of the parties that participated in the Schedule 13D filing and financing and served as the Company’s Executive Chairman of the Board, non-Executive Chairman of the Board, Chief Executive Officer and President from 2013 through 2017.”

Turnaround Plan Is Quickly Gaining Traction

Since taking over in April 2019, Mr. Tu has restructured the company and relaunched growth initiatives. The management has been able to reduce losses by 60% and started growing sales in Q4 2019. Q1 2020 sales grew to $3.8m, 19% YOY and 7% sequentially. Adjusted EBITDA improved to a loss of $1.1 million for Q120 versus a loss of ~$2.0 million in Q119. Net loss also registered an improvement to $0.5 million in Q120 compared to a loss of $2.9 million in Q119.

EFOI expects the growth momentum to continue in Q2 as well despite the COVID-19 pandemic. During EFOI’s Q4 conference call, Maj asked James where sales had to get to in order for the company to achieve break even ($7 to $8 million), liquidity needs and margin profile.

Maj Soueidan, GeoInvesting

Okay, great. And before my next question, I guess I know you can’t give guidance, but if you – could you give us an idea, like where your break-even revenue point might be.

James Tu

So, I would say that if you look at our current overhead, you’re probably going to be looking at, say, anywhere between $7 million to $8 million on a quarterly basis for profitability. On the other hand, if we see that we are not getting there very quickly, we will have to adjust our offerings. Right? So,it’s a dynamic situation. But if we can see that we have pretty aggressive growth plans and obviously, this COVID-19 is a –throws a monkey wrench. So we need to be dynamic. Our plan is not to raise equity capital in 2020.

Maj Soueidan, GeoInvesting

Hello, guys, thanks for taking the question. I have two questions for you. James, I just wanted a clarification now and earlier, I didn’t hear it quite clearly. It seemed like you said that maybe you might have to raise some money in 2020. I wasn’t quite sure I heard that right. Maybe clarify, what are your needs for 2020 above what you kind of have now on your balance sheet? And if you were to raise to finance growth in 2020 how would you maybe look to do that now?

James Tu

Yeah, I’ll answer and then Tod can add on. So our plan, we don’t have a plan to raise equity capital. What we are working on now, as Tom mentioned, is to expand our credit facility which we have been working on over the past few months. Our current credit facility is pretty low against our receivables and inventory. So we believe that there’s much more capital accessible for us from the credit facility standpoint.

We, as I mentioned the $2.7 million that we raised in the equity capital, give us a lot of room to maneuver this challenging time. I also emphasize that as I said in the earnings script that we stay on top of what’s going on. And if we see dramatic changes around the sales patterns and forecasts, we will have to make some operating expense adjustments as well. So just staying on top of what’s going on. And we’ll make sure that we take action in a timely manner. Tod?

Regarding Q2, EFOI expects net sales to be in the range of $4.5 million to $4.8 million, representing sequential growth of 19%-27%, and a year-on-year growth of 46%-56%. Midway through the Q2, EFOI has already booked more than 70% of the forecasted sales, and therefore we are confident that it will meet its Q2 sales guidance. So, EFOI is quickly approaching its targeted break-even revenue point.

EFOI is still early in its long-term growth trajectory. In its Q1 earnings call James Tu noted:

“We continued to grow from Q4 2019 into Q1 2020, and despite of the myriad challenges posed by the pandemic, we expect to continue to grow from Q1 to Q2, built upon the first arrow of our rejuvenated growth from our military business where we are now more competitive than ever. With the recent launch of EnFocus we also look forward to having this second arrow of growth propel our commercial business as well as our overall sales from the second half and especially 4th quarter on.”

With each quarter, we are gaining confidence that James Tu has put the company on the path to achieving sustainable and profitable growth. We think that the recent launch of a transformative new product line (En Focus) will accelerate EFOI’s path to reach profitability since it opens up new markets and may have a slight, but sustainable, COVID-19 angle.

Large Addressable Market with Less Competition

Less Competition:

The LED market is highly competitive and has largely been commoditized. EFOI’s competition, including The Big Three lighting players (GE, Philips & Osram) experienced the same pain EFOI experienced as the LED industry evolved. However, instead of adapting, a good deal of the competition chose to exit the LED business through spin-offs, asset sales or by just shuttering operations. This has left a leadership vacuum in the industry which EFOI intends to fill.

Long Runway for Growth

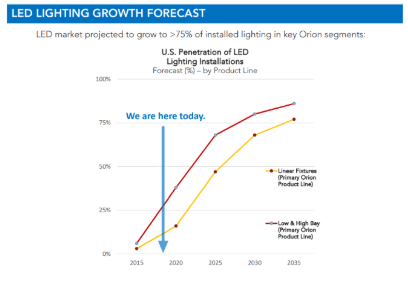

According to Grand View Research, the global LED lighting market size is expected to reach $128 billion by 2027 with a CAGR of 10.8%. LEDs are still in the very early phases of adoption in EFOI’s target markets. IBIS Industry Reports projects that by 2020, healthcare, education, commercial and industrial markets will still only be 17% to 18% penetrated, leaving a large opportunity for future growth. The increasing demand for LED lighting is being driven by energy and cost savings, environmental considerations and human health.

The same view was reiterated by the management during their Q120 earnings call where they talked about significant market opportunities for LEDs.

“Despite of all the buzz we might have heard about LED being everywhere and getting cheaper by the day, an overwhelming majority of the country’s and world’s existing commercial buildings today are still lit by fluorescent lighting. DOE’s latest estimate was that in 2017 only 11% of the country’s more than 1.1 billion linear lighting fixture were lit with LEDs. Today the penetration is likely to still be well below 20%, and % of lighting fixtures with controls are even lower. That represents tens of billions of dollars of opportunities in the coming years to upgrade these fixtures to LEDs and connected lighting, just in the United States.”

LED Lighting Solutions Save Customers Money and Improve Employee Productivity

The obvious benefit of LED is a 40% to 50% cost reduction compared to other sources of unnatural light. Additionally, up to an 80% direct cost savings can arise from adopting IoT applications that LED lighting solutions allow for, such as regulating lighting use through motion control and tracking assets. We don’t know about you, but we didn't connect the dots between lighting solutions and IoT. But, apparently it’s the perfect marriage:

“Generally, but especially for industrial locations, lighting is the ideal entry point for IoT data,” said Jamie Britnell, Director of Product Marketing – Lighting, Synapse Wireless (www.synapsewireless.com). “Because all these facilities incorporate lighting, an IoT communication network grid is essentially installed as part of an LED retrofit or in new construction. With this network in place, compatible sensors can be distributed through the facility to monitor various equipment and processes.”

Here are two examples of how IoT solutions are applied through LED solutions:

1.

“Dubbed Track & Trace and using its established Einstone Bluetooth beacons embedded in the luminaires, the system can monitor resources in real time and additionally provide data about movement and usage.”

2.

“Using a hospital as an example, Osram says medical equipment such as ultrasounds and portable ECG machines can be tracked in real time on an analytics dashboard. In order to be able to track assets, miniature radio transmitters called beacons are integrated into the lighting infrastructure. These form a Bluetooth Low Energy mesh network by means of which data can be transmitted and received.

The assets to be tracked are equipped with ‘asset beacons’ that also send out signals via Bluetooth. This signal data is transmitted via the mesh network and passed on to a gateway.

Analysis of the data allows the locations of the objects to be calculated and displayed on a user’s dashboard. In addition to identifying asset locations, it’s also possible to create heat maps or analyses of tool utilization, and perform temperature monitoring for sensitive objects.”

Employee Productivity Gains

There is also a growing awareness of the profound influence lighting can have on human health and well-being.

According to a2006 survey, the quality of a lighting solution can also have an indirect benefit to a reduction in costs through improved employee productivity:

“90% of employees admitted that their attitude about work is adversely affected by the quality of their workplace environment.”

...and some companies have seen...

"productivity gains of 6% to 16% and reduced absenteeism were achieved by converting to improved lighting."

Human-centric lighting (HCL) focuses on enhancing biological, emotional, and overall health of people. That is why human-centric LED lighting (HCL) is gaining significant traction. HCL allows control over the lighting level and color spectrums. This improves circadian wellness which significantly boosts learning effectiveness and worker productivity. A study has shown that the use of human-centric lighting improves worker productivity by up to 20%.

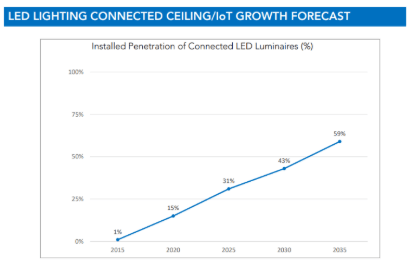

Combined with Internet of Technologies (IoT), HCL can open up a whole new opportunity for growth. IoT enabled or Smart lighting is an LED lighting system with integrated sensors and controllers that are networked, enabling lighting products within the system to communicate with each other and transmit data. According to Market and Research, the global smart lighting market is estimated to grow from $13.4 billion in 2020 and to $30.6 billion by 2025, at a CAGR of 18.0%.

Introduction Of EnFocus To Lead EFOI’s Foray Into Human-Centric Lighting

EFOI launched its breakthrough, patent-pending human-centric lighting control platform, EnFocus in May 2020. With this, EFOI transformed itself from an “energy-efficient” centric LED lighting company to one that caters to “total sustainable” solutions. EnFocus will significantly expand the addressable market for the company. EFOI is specifically targeting 5.6M existing commercial buildings in the US and many more globally.

“Since EnFocus is designed for universal electrical setting to replace fluorescent lamps, it is also well-positioned to enter the international markets that are several times larger than the US market. We are confident that building owners and occupants worldwide will be much more motivated to convert to LED lighting if significant human benefits such as dimming and circadian rhythm outside of energy efficiency are available and affordable. With EnFocus, we aim to maximize the financial, environmental and human—or triple-bottom-line—benefits from LED lighting, and capture a meaningful share of the coming retrofit opportunities as LED lighting move onto the next phase of accelerating adoption driven by human-centric lighting.”

EnFocus will provide dimming and color tuning capabilities for existing buildings. EnFocus LED lamps can replace existing tubes without the need to replace the whole fixture. This makes EnFocus far more affordable and accessible than any other lighting control solutions in the market, particularly for retrofit applications. An EnFocus DCT installation, which provides both a dimmable and color tuneable lighting solution, costs just $330, compared to other similar solutions in the market which range from $1,100 to $2,000.

Additionally, EFOI is expanding functionalities and applications built upon EnFocus, such as UV disinfection and autonomous controls. The demand for disinfection technologies and products is surging amid the COVID-19 pandemic which might not be going away any time soon. Thus, from niche markets such as those that deal in the healthcare fields, these disinfection products are now being used across industries, thereby further expanding addressable opportunities. EFOI is on schedule to launch its first UV disinfection production by early Q420.

“In addition to the fact that coronavirus is still impacting countries across the world and might not be going away anytime soon, the world’s sudden awareness and realization that the risk of pandemics is here to stay will likely push demand for air and surface disinfection to unprecedented heights and stay permanent and universal to a large extent going forward.”

Valuation

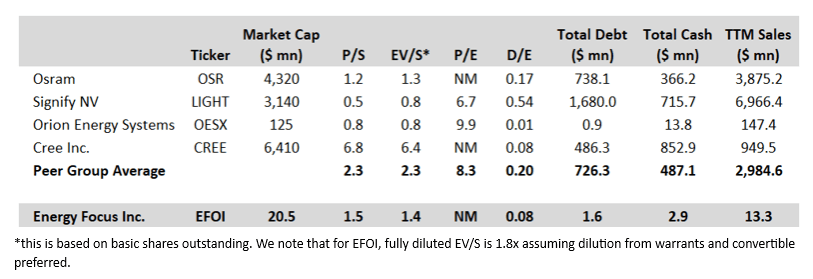

The peer group for EFOI is primarily comprised of companies serving the LED lighting market. As can be seen below, EFOI shares are trading at TTM EV/Sales of 1.4x, which is on par with most of the comps. However, given that the company is in the early stages of its long-term turnaround, we believe the stock is likely to get further re-rated and will eventually carry a premium valuation as management continues to execute on its growth plan.

Caveats

- The stock is up almost 3.5x in the last month or so.

- A prolonged economic downturn due to COVID-19 or a more aggressive second wave of infections could hurt the commercial business prospects.

- Growth prospects of EFOI are tied to successful launches of new products. Any delay or failure to launch these products could adversely impact the business.

- LED lighting is a rapidly evolving industry and as such, technology obsolescence remains a risk.

- Given some uncertainty on the speed at which EFOI’s turnaround plan will result in positive cashflow and profitability, we need to be a little cognizant of the risk of an equity raise. However, with the completion of the recent stock offering, we believe the company is in a good position to fund operations organically and through its balance sheet, which has $2.9 million in cash, ~$2.5 million from deep in-the-money warrants and $1.1 million left on its line of credit. The company also received $794 thousand from the COVID-19 Payroll Protection Program.

- We would like to dig into the competition to understand that, barring $CREE, why premium valuations are not being awarded to most of them. It’s our intention to determine why CREE is an outlier.