SUMMARY

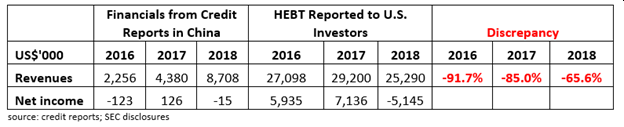

- According to filings in China, Hebron Technology Co., Ltd. (NASDAQ:HEBT) greatly exaggerated its legacy business financials in the past three years, with revenues 92%, 85%, and 66% lower than those reported by the Company to the U.S. investors, through SEC filings, in 2016, 2017 and 2018 respectively.

- Even with exaggerated financials, HEBT’s legacy business shows a big downtrend in the first half of 2019.

- We believe HEBT failed to disclose a $3.45 million debt-to-equity conversion transaction in 2019 involving HEBT’s main wholly-owned subsidiary in China. This could put the shares at an elevated of risk of being halted and delisted from the NASDAQ.

- Margin assumptions in a Valuation Report for newly acquired company, Fintech Shanghai, are too optimistic and have likely helped boost Fintech Shanghai’s valuation.

- In reality, HEBT’s current biggest shareholder, Bodang Liu, would essentially spend much less money than the proclaimed $9 million to obtain control of the company.

- HEBT’s market cap increased close to $70 million since the $7 million Fintech Shanghai acquisition. We believe this is a classic pump and dump scheme destined for near-term failure.

- Another company controlled by HEBT’s current biggest shareholder, Bodang Liu, attempted but failed to issue new shares and uplist itself from OTCQB to NASDAQ, instead it was downgraded to Pink Current from OTCQB in 2018

- If HEBT’s hyped stock price has anything to do with expectations of completing a merger with $SFHD, investors may be in for a big surprise! Aside from new regulatory risks pressuring the P2P industry in China, all SFHD’s 24 branches have been de-registered.

- According to a 13D filed by Apex Trading Group Inc. and Form 4 analysis, Apex has been acquiring HEBT shares at a cost of zero, which leads us to believe that HEBT has been issuing highly dilutive new shares to Apex without any explanation.

- The only other 13D filing we were able to find related to Apex was one that showed Apex had purchased an over 5% position in Helios & Matheson Analytics Inc (OOTC:HMNY) (aka movie pass)!

- Even if we generously ignore the exaggerated financials from HEBT’s legacy business, we believe shares are worth no more than $1.16 to $1.37, which are 80% and 76% lower than the December 18, 2019 closing price of $5.63.

We believe HEBT is a classic U.S. listed china pump and dump. We also believe that once investors become aware of all the issues and red flags we will point out in this report, that it is highly possible the shares could fall by approximately 80% from current levels.

Not only do we believe that the current stock price is way too high when compared to the company’s weak fundamentals as portrayed in its China filings. But also that HEBT faces a real risk of being halted and delisted from the NASDAQ due to:

- Failing to disclose $3.45 million debt-to-equity conversion transaction in 2019 involving HEBT’s main wholly-owned subsidiary in China.

- Financials portrayed in SEC filings not even being close to the lower sales and earnings disclosed in filing sources in China.

Legacy Business Exaggerated Financials and Trending Down

The company’s legacy business, which develops, manufactures and provides customized installation of valves and pipe fittings in industries such as pharmaceutical, biological, food and beverage, and other clean sectors, is not generating near the level of revenue that the company has depicted to the U.S. investors through SEC filings. Based on the credit reports obtained in China regarding the company’s two subsidiaries, Zhejiang Xibolun Automation Project Technology Co., Ltd. (Chinese name: 浙江希伯伦自控工程科技有限公司, “Xibolun Automation” thereafter) and Wenzhou Xibolun Fluid Equipment Co., Limited (Chinese name: 温州希伯伦流体设备有限公司, “Xibolun Equipment” thereafter), the consolidated revenues from credit reports were astoundingly 91.7%, 85.0%, and 65.6% lower than what HEBT reported to the Securities and Exchange Commission (SEC) and U.S. investors in 2016, 2017, and 2018, respectively!

Regarding the net profit, from 2016 to 2018, the credit reports indicate that these two consolidated subsidiaries were barely breaking even. Specifically, in 2016 and 2017, the HEBT reported to the SEC and U.S. investors profits of $5.9 million and $7.1 million, respectively, and representing a stark and shocking difference from the loss of $123 thousand and profit of $126 thousand in the corresponding years based on credit reports.

Regardless of our due diligence that has led us to conclude that financials reported to the SEC and U.S. investors are false, according to the company’s half year 2019 financials filed just days ago, sales decreased to $5.6 million in first half 2019, from $10.3 million in first half 2018. Net loss in first half 2019 was $677 thousand compared to net loss of $1.6 million in first half 2018.

Based on the comparison between the financials from credit reports we obtained in China and SEC disclosures, and the current reported financials for the first half of 2019, it is clear to us that the company’s legacy business should not be worth any more than what it was worth before a change in control event that was announced on April 16, 2019,or below $1.00 per share.

Where is the Disclosure Regarding the Wholly-owned Xibolun Automation’s $3.45 million Debt-to-Equity Conversion?

According to this December 9, 2019 article by the city government of Wenzhou, where both of HEBT’s wholly-owned subsidiaries are located, it seems that HEBT’s wholly-owned subsidiary Xibolun Automation completed a $3.45 million debt to equity conversion in 2019.

…根据外商投资企业债权转股权新政,企业债权股成为外资利用新方式。今年我市成功实现两家外商投资企业债转股,其中嘉利达(平阳)明胶有限公司债转股1500万美元,浙江希伯伦自控工程科技有限公司债转股345万美元。

Translation [Paraphrased]

…According to the new foreign investment company debt to equity conversion policy, ‘company debt to equity swaps has become a new way used by foreign capital (to invest). This year [2019] our city successfully completed two foreign investment companies’ debt to equity swaps. Jialida (Pingyang) Minjiao Co, Ltd.’s debt converted to equity worth of $15 million, and Zhejiang Xibolun Automation Project Technology Co., Ltd.’s debt converted to equity worth of $3.45 million.

However, based on the first half 2019 financials disclosed by the company, we did not see any convertible debt, nor did we see any meaningful debt/liability decrease that can be associated with the $3.45 million debt to equity swap. Also absent were any filings or press releases disclosing the event:

source: company disclosure

Red Flags Surrounding the $7 million Acquisition of Fintech (Shanghai) Investment Holding Co., Ltd (“Fintech Shanghai”)

Red Flag 1: Certain Assumptions in the Valuation Report Are Too Optimistic

In the Valuation Report, the appraiser, ValueLink, applied two valuation methods to value Fintech (Shanghai) Investment Holding Co., Ltd (in Chinese, 范太克 (上海) 投资控股有限公司; it’s worth noting that Fintech Investment holdings changed its Chinese name to 范太克(上海)数字科技有限公司 on June 28, 2019 per SAIC filings obtained in China. However, we will use “Fintech Shanghai” for reference purposes going forward). In the Valuation Report, there is introduction for Fintech Shanghai’s business:

汇晶社 is an innovative asset allocation service platform under 范太克(上海)投资控股有限公司 (hereafter referred to as “Fintech” or the “the target Company”) . As a third-party service platform for direct selling banks, 汇晶社 has connected several domestic commercial banks and rural commercial banks to provide asset allocation services, Internet traffic diversion services, IT business system construction services and transaction structure design and construction services. By integrating consumer financial assets, traffic, IT business system technology and big data risk control business experience, we will create an eco-finance technology platform for professional services direct banking.

According to the Valuation Report, Fintech Shanghai’s value falls within the range between RMB 54.374 million (~USD 7.9M) and RMB 59.737 million (~USD 8.7M).

Valuation Summary

Based on our analysis and the information provided by the Company, having regard to our work scope and limitations in scope of work, and subject to the significant assumptions as well as general assumptions and limiting conditions, the equity interest owned by Fintech has been estimated to be falling in a range from approximately RMB 54.374 million to 61.349 million as of the Valuation Date by Income approach, and a range from approximately RMB 57.162 million to 59.737 million as of the Valuation Date by Market approach.

We do not intend to scrutinize each assumption the appraiser used when performing its valuation of the company. However, there are certain points that we believe are simply unrealistic and worth pointing out.

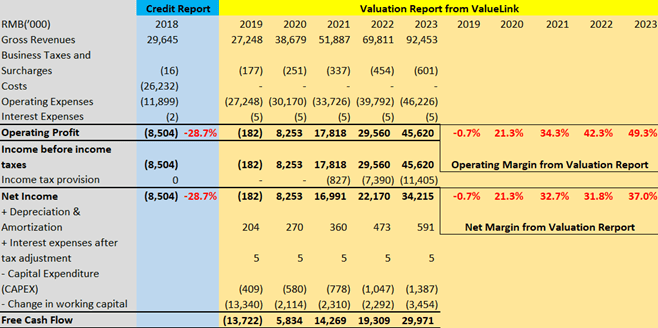

We believe the margins that the appraiser assumes from 2019 to 2023 are too optimistic. Based on the credit report (Blue column in table below) we obtained on Fintech Shanghai, the company’s operating loss is about RMB 8.5 million (USD 1.2M) on total revenues of RMB 29.645 million (USD 4.23M), which translates into a negative operating margin of 28.7%. However, the appraiser assumes that going into 2019, the company’s operating margin will turn slightly negative to -0.7%, and then in 2020, the operating margin would suddenly turn into a whopping positive 21.3%, and without fail continue to increase year over year until 2023, when its operating margin would magically land at 49.3%!

Regarding the net profit margin profile, in 2018, the credit report shows a net loss of RMB 8.5 million (USD 1.2M) with a net profit margin of -28.7%. Based on the Valuation Report, the appraiser assumes that in 2019, the company’s net margin would turn to be -0.7%, and it would be 21.3% in 2020, and up until 2023, the net profit margin would be 37.0%, a similar theme to that of the assumed growth in operating margins.

It is hard for us to believe that the company would be able to achieve these margin assumptions in the coming years, which makes us doubt the value derived from this Discounted Cash Flow (DCF) method.

source: credit report; HEBT’s SEC disclosures

Note: The company had no revenue in 2017

Red Flag 2: $7 Million Fintech Shanghai Acquisition Occurs Simultaneously with $9 million Company Controller Change Transaction

According to a Share Purchase Agreement filed on June 4, 2019, HEBT completed the $7 million Fintech Shanghai acquisition at the same time as when HEBT’s current controlling shareholder, Bodang Liu, paid $9 million to purchase the shares of HEBT’s previous controlling shareholder, the Sun Family.

As illustrated above, if we consider these two transactions together, we find that the current controller of HEBT, Bodang Liu, would have only needed to spend a net amount of $2 million while becoming the largest shareholder (47.8%) of HEBT. The company’s market cap increased from $15 million to over $90 million within months since the transactions.

To sum up, the Fintech Shanghai acquisition shows a couple of alarming red flags. First, even if the company stated that the $7 million acquisition of Fintech Shanghai was at a discount to the proposed valuation range between $7.9 million and $8.7 million provided by the appraiser ValueLink, we have doubt on at least some of the major assumptions that the appraiser used when conducting its DCF valuation. Second, HEBT’s current biggest shareholder, Bodang Liu, would really only need to pay $2 million to take control of the company and enjoyed an over $70 million market cap appreciation since he took control of the company.

SFHD’s Failed NASDAQ Listing and New Share Offering is a Big Red Flag, and Unlikely Adds Value if it Merges with HEBT

Hui Ying Financial Holdings Corp. (OTCQB: SFHD), through a contractual agreement with its VIE entity Benefactum Alliance Business Consultant (Beijing) Co., Ltd. (Chinese name: 惠众商务顾问(北京)有限公司, “Benefactum Beijing” thereafter), operates a peer-to-peer (P2P) platform to match investors with small and medium-sized enterprises (“SMEs”) and individual borrowers in China. The company went public on OTCQB through a reverse merger in 2016. The company intended to conduct a stock offering of 5.55 million shares at price of $5.85 and seek to list its stock on the NASDAQ exchange with a new symbol “HYJF”, according to the most recent S-1/A filed by the company in June 2018 (the original S-1 was filed on July 26, 2017, and there are a few S-1/As after that).

Bodang Liu, who is now the controller of HEBT, is SFHD’s largest shareholder, accounting for 93.25% of the total equity interest before the proposed offering. However, based on a filing by SFHD on September 12, 2019, the offering and the stock exchange uplisting was withdrawn, which means SFHD’s plan of offering new shares and uplisting to the NASDAQ exchange has failed. Instead, on May 23, 2018, SFHD on OTCQB was downgraded to Pink Current. The reason cited for the downgrade was “Filed to Cease Reporting”.

It is unclear to us if Liu plans to merge SFHD with HEBT, but we believe the price hype of HEBT this year might be due to this expectation. However, based on our research, the regulatory environment on the P2P sector in China is extremely harsh and SFHD’s current and future business prospects are not good to say the least. As a matter of fact, merging with SFHD would expose HEBT’s shareholders to tremendous regulatory risks.

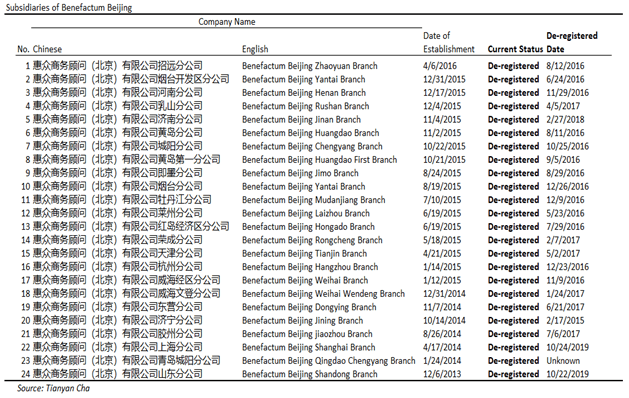

According to SAIC filings in China, the VIE company, Benefactum Beijing, that operates a P2P platform in China for SFHD has 24 branches, and surprisingly all of its branches have been de-registered (注销). The table below summarize those branches’ establishment and de-registered dates. It is understandable that while conducting business, certain new branches may be established and old branches may be de-registered, depending on how the business goes, but it is very rare to see a company have all its branches de-registered. This leads us to believe that the business of Benefactum Beijing is having some grave troubles and has possibly been shuttered.

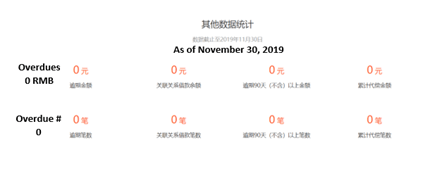

In addition, if investors go to the P2P website www.hyjf.com operated by Benefactum Beijing, under the information disclosure section, regarding its operating data, there are some metrics that are simply outrageous.

source: www.hyjf.com

For example, the website shows, as of November 30, 2019, the overdue amount in terms of RMB is 0, and number of overdue payments is 0. And the website also showed that the cumulative transaction amount has been RMB 30.8 billion (USD 4.4B) with 1.163 million transactions in total.

source: www.hyjf.com

This kind of operating data disclosed by the company on its website is simply too good to be true. We strongly believe that there are no financial institutions or any other P2P platforms in the world that would be able to achieve 0 overdues for over 5 years of operation with more than 1 million transactions for a cumulative transaction amount of 30.8 billion RMB (USD 4.4B).

Another big risk worth noting is that, according to the company’s disclosure on its website, the majority of the lenders (58.99%) on the platform are from Shandong Province. Lenders from Henan Province account for 3.84%, and lenders from Hebei Province account for 1.67%.

source: www.hyjf.com

According to a media report in China, regulators in Shandong Province stated on October 18, 2019 that thus far, there are no P2P platforms that have fully complied with the rules and regulations, and it plans to shut down all the P2P platforms that do not pass the review in the future. Also, this November the regulators in Heinan Province stated that since 2016 there are no P2P platforms that have fully complied with the rules and regulations. In addition, on December 13, 2019, according to another media report in China, regulators in Hebei Province stated that there are no P2P platforms that have complied with the related rules and it has shut down 35 P2P companies. This is the regulatory environment that SFHD is currently operating in.

With all being said, we strongly believe that, even if HEBT’s current controller, Bodang Liu, successfully merges SFHD into HEBT in the coming future, it will not add much value for HEBT’s shareholders; rather, it may bring with it tremendous regulatory risks (i.e. potential suspension of business or even shutdown of business).

Numerous Red Flags From the other 13D Filer, Apex Trading Group Inc., and its Purchase of HEBT’s Stocks

Apex Trading Group is a self-touted “worldwide financial service firm engaging in day-trading of U.S. and Canadian securities. We find the firm is mysterious for many reasons.

For one, there is extremely limited information on this entity.

According to Yi Huang, the group’s COO,

Apex Trading Group was founded in 2007, and has long been recognized in the worldwide financial community as a financial service firm engaging in day-trading of US. and Canada securities.

Apex Trading Group company owns more than 100 trading floors which are distributed worldwide. Working together the monthly trading volume typically reaches up to one billion shares traded.

Apex Trading Group cooperates with a large clearing company, not only providing a high quality payout rates but satisfying all service requirements for our clients. We offer the best trading platform accessing the stock exchanges directly while also accessing various dark-pool routes; all at extremely low transaction costs and commission which gives customers an advantage on trading with large volume. We offer the largest capital leverage, allowing you to multiply revenue to the highest extent, and the most humanized and reasonable management considering the benefits and risks of your trading.

In addition, Apex Trading Group also offers technical support and training service back by years of working experience and knowledge to help with creating and managing their own company team of traders. On top of it all, Apex Trading Group has a number of high-quality, professional, experienced service team members proficient in Chinese and English languages.

The most detailed description of the company’s business we could find on the internet was from the COO’s LinkedIn profile, not what you would really expect from a “worldwide-financial-community-recognized” financial service firm.

In addition, despite Apex Trading Group claiming to hold 100 trading floors, we could only identify one location on Google Maps, corresponding to the address 181 Spadina Rd, Richmond Hill, Ontario, Canada, of what appears to be a residential house.

This address is validated by one sec filing.

Moreover, the company alleges that it has a number of high-quality professionals. Yet, we could only identify three individuals on LinkedIn connected to Apex Trading. A Sylvia Yang, manager, a Yi Huang, COO and an Alex Ye, CEO.

Secondly, the limited pieces of information out there are contradictory. For example, the Schedule 13D filed for the purchase of HEBT shares indicates that the receiving address for notices and communications is Room 1816, Zhonghuan International business building and Finance Counsel No.105, zhongshan north road, gulou district, Nanjing city, Jiangsu prov.

Our on-the-ground investigation team visited this abovementioned address in the city of Nanjing, Jiangsu Province in China. The left picture below is taken in front of the room 1816 in the building. The English name shown on the wall inside this office is AT TRADING, and the Chinese company name above the English name is 南京宏美投资管理有限公司 (Nanjing Hongmei Investment Management Co., Ltd.). Per SAIC information, this company’s legal representative and executive director is Zhou Ye (叶舟) and its supervisor is Xiaohong Yang (杨小红). The right picture below is taken outside of the building within which the 1816 office is located.

However, according to Legal Entity Identifier filings, the headquarters address of Apex Trading Group Inc. is 246 hao, C building, 4 dan yuan, 15ceng ,2 shi, Hua Yuan Street, Harbin CN 150001. We wonder why communications are not sent to the headquarter office instead. Also note that Google Maps renders a Canadian address instead. Lastly, according to this Schedule 13D, the company is a corporation incorporated under the laws of the People's Republic of China. However, the Legal Entity Identifier indicates its legal address to be Akara Bldg, 24 De Castro St, Tortola ,Road Town VG VG1110, and legal jurisdiction to be VG, which is the British Virgin Islands. This contradictory information leaves us scratching our head, trying to figure out where the company is really incorporated and operating.

Moreover, Apex has been involved with some pretty peculiar investments to say the least. We have only been able to identify them to appear in two Schedule 13Ds. One of which is for HEBT, and the other filed for Helios and Matheson Analytics Inc (now trading at OTC:HMNY). on August 16, 2018. According to the 13D, the company purchased 611,600 shares of Helios at 0.04658 dollars per share. This investment in the company was most likely due to Helios purchasing a majority stake in MoviePass in August 2017. In early August 2018, the company acquired the assets of Emmett Furla Oasis Films. Shortly following HMNY’s investment, the Attorney General of New York opened an investigation into Helios looking into whether it misled investors about the company’s financial situation. The company’s stock was delisted on February 12, 2019 and moved to OTC markets. The stock is trading at 0.0027 dollars per share as of the date of this report. This, to say the least, indicates that Apex has a bad taste for stocks, if not having red flags flying all over the place.

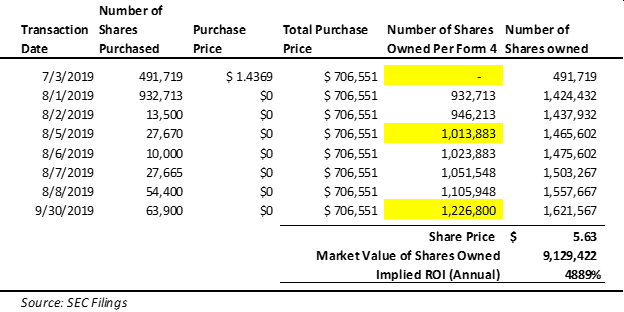

Finally, and most importantly, Apex’s dealings with HEBT are very unorthodox and raises many big questions. According to 13D, Apex initially purchased 491,719 shares from HEBT on July 3, 2019 at an average market price of 1.4369 dollars a share. However, shortly after starting on August 1st, it appears to us that Apex had multiple transactions where they purchased stocks from HEBT at zero dollars (or were these stocks granted/awarded by the company for free?). In addition, according to their Form 4 filings, they did not actually own any shares prior to August 1st, which is contrary to the 13D disclosure. Below is a table that illustrates all transactions, taking into consideration the 13D purchase.

There are several noticeable red flags related to these filings. First and foremost, number of shares owned per Form 4 do not equate to the total number of shares purchased on many occasions. Secondly, the form 4s share counts failed to take into consideration of the initial 13D purchase. We have made adjustments to both red flags and calculated what we believe to be the more accurate share ownership numbers. Most importantly, we discovered that all Form 4 filings had a purchase price of zero dollars. Apex is the only disclosed insider on Form 4, indicating that shares were not transacted between other insiders and Apex. It is also not plausible that Apex purchased these shares from the open market at zero cost. Hence, we believe Apex was issued these additional shares free of charge and HEBT erroneously filed as a purchase Form 4. Regardless, considering that Apex spent in total $706,551 and now holds equity worth approximately $12M, this trail of events paints them as either the next Warrant Buffet, or somebody benefiting from insider information and profiting off the absurd stock price. We calculate their implied ROI to exceed 4,889% per annum.

Reverse-Takeover Structure Indicates Minimal Valuation

In the previous sections, we discussed that Bodang Liu purchased 47.8% of all the company’s outstanding common shares for a total purchase price of $9M. Simultaneously with the sale and transfer of shares, HEBT will acquire Fintech (Shanghai) Investment Holding Co., Ltd (“Fintech Acquisition”) (a Bodang Liu entity) for $7M, which will be paid through operating profit or future capital raises over the next two years. Finally, the agreement also grants the sellers the option to purchase back the Company’s equity interest in Zhejiang Xibolun Automation Project Technology Co., Ltd., the Company’s 49% equity interest in Xuzhou Weijia Biotechnology Co., Ltd. and the Company’s equity interest in Wenzhou Xibolun Fluid Equipment Co., Limited, Chinese operating subsidiaries of the Company (collectively the legacy business) (“Purchase Option”).

We believe this convoluted chain of events is essentially a reverse takeover attempt by NiSun International Enterprise’s CEO Bodang Liu. The share purchase agreement allowed Liu to become the largest shareholder of HEBT. In addition, the Fintech Acquisition is allowing Liu to take his operating business and inject it into HEBT. Lastly, the remanence of the legacy business of HEBT could be effectively moved out of HEBT by the Purchase Option.

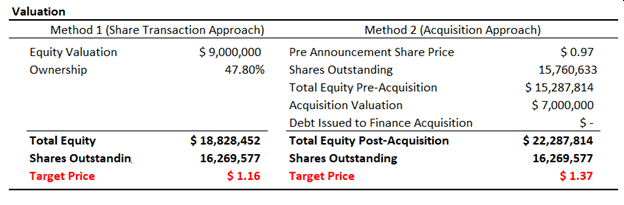

Additionally, we believe the agreement essentially indicated HEBT’s true intrinsic valuation. According to the initial purchase report, where 47.8% of HEBT’s total shares were acquired for $9 million, the total equity of the firm would be an abysmal valuation of less than $20 million. Notice the current market cap of HEBT is $91.6 million. This would imply either Liu purchased the company at 79% discount, or the market is valuing the company at 486% premium. Either way, Liu is getting a very sweet deal.

We’ve also generously considered the $7M acquisition to be accurate and calculated the implied equity value. We do not see synergy between the target company and HEBT. In which case, the stock today would still be over-valued by 410%.

In conclusion:

We believe HEBT is a classic U.S. listed china pump and dump that worth no more than $1.16 to $1.37, and it is highly possible the shares could fall by approximately 80% from current levels. Buyer beware!

Disclaimer

Please be advised that GeoInvesting™ is a research and publishing firm, of general and regular circulation, which falls within the publisher’s exemption to the definition of an “investment advisor” under Section 202(a)(11)(A) – (E) of the Securities Act (15 U.S.C. 77d(a)(6) (the “Securities Act”). GeoInvesting™ is not registered as an investment advisor under the Securities Act or under any state laws. None of our trading or investing information, including the Content, GeoInvesting™ Email, Executive Casts and/or content or communication (collectively, “Information”) provides individualized trading or investment advice and should not be construed as such. Accordingly, please do not attempt to contact GeoInvesting™, its members, partners, affiliates, employees, consultants and/or hedge funds managed by partners of GeoInvesting™ (collectively, the “Geoinvesting™ Parties”) to request personalized investment advice, which they cannot provide. The Information does not reflect the views or opinions of any other publication or newsletter.

We publish Information regarding certain stocks, options, futures, bonds, derivatives, commodities, currencies and/or other securities (collectively, “Securities”) that we believe may interest our Users. The Information is provided for information purposes only, and GeoInvesting™ is not engaged in rendering investment advice or providing investment-related recommendations, nor does GeoInvesting™ solicit the purchase of or sale of, or offer any, Securities featured by and/or through the GeoInvesting™ Offerings and nothing we do and no element of the GeoInvesting™ Offerings should be construed as such. Without limiting the foregoing, the Information is not intended to be construed as a recommendation to buy, hold or sell any specific Securities, or otherwise invest in any specific Securities. Trading in Securities involves risk and volatility. Past results are not necessarily indicative of future performance.

The Information represents an expression of our opinions, which we have based upon generally available information, field research, inferences and deductions through our due diligence and analytical processes. Due to the fact that opinions and market conditions change over time, opinions made available by and through the GeoInvesting™ Offerings may differ from time-to-time, and varying opinions may also be included in the GeoInvesting™ Offerings simultaneously. To the best of our ability and belief, all Information is accurate and reliable, and has been obtained from public sources that we believe to be accurate and reliable, and who are not insiders or connected persons of the applicable Securities covered or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such Information is presented on an “as is,” “as available” basis, without warranty of any kind, whether express or implied. GeoInvesting™ makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such Information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and GeoInvesting™ does not undertake to update or supplement any of the Information.

The Information may include, or may be based upon, “Forward-Looking” statements as defined in the Securities Litigation Reform Act of 1995. Forward-Looking statements may convey our expectations or forecasts of future events, and you can identify such statements: (a) because they do not strictly relate to historical or current facts; (b) because they use such words such as “anticipate,” “estimate,” “expect(s),” “project,” “intend,” “plan,” “believe,” “may,” “will,” “should,” “anticipates” or the negative thereof or other similar terms; or (c) because of language used in discussions, broadcasts or trade ideas that involve risks and uncertainties, in connection with a description of potential earnings or financial

performance. There exists a variety of risks/uncertainties that may cause actual results to differ from the Forward-Looking statements. We do not assume any obligation to update any Forward-Looking statements whether as a result of new information, future events or otherwise, and such statements are current only as of the date they are made.

You acknowledge and agree that use of GeoInvesting’s™ Information is at your own risk. In no event will GeoInvesting™ or any affiliated party be liable for any direct or indirect trading losses caused by any Information featured by and through the GeoInvesting™ Offerings. You agree to do your own research and due diligence before making any investment decision with respect to Securities featured by and through the GeoInvesting™ Offerings. You represent to GeoInvesting™ that you have sufficient investment sophistication to critically assess the Information. If you choose to engage in trading or investing that you do not fully understand, we may not advise you regarding the applicable trade or investment. We also may not directly discuss personal trading or investing ideas with you. The Information made available by and through the GeoInvesting™ Offerings is not a substitute for professional financial advice. You should always check with your professional financial, legal and tax advisors to be sure that any Securities, investments, advice, products and/or services featured by and through the GeoInvesting™ Offerings, as well as any associated risks, are appropriate for you.

You further agree that you will not distribute, share or otherwise communicate any Information to any third-party unless that party has agreed to be bound by the terms and conditions set forth in the Agreement including, without limitation, all disclaimers associated therewith. If you obtain Information as an agent for any third-party, you agree that you are binding that third-party to the terms and conditions set forth in the Agreement.

Unless otherwise noted and/or explicitly disclosed, you should assume that as of the publication date of the applicable Information, GeoInvesting™ (along with or by and through any Geoinvesting™ Party(ies)), together with its clients and/or investors, has an investment position in all Securities featured by and through the GeoInvesting™ Offerings, and therefore stands to realize significant gains in the event that the price of such Securities change in connection with the Information. We intend to continue transacting in the Securities featured by and through the GeoInvesting™ Offerings for an indefinite period, and we may be long, short or neutral at any time, regardless of any related Information that is published from time-to-time.