By Maj Soueidan, Co-founder GeoInvesting

On February 8, 2019, we disclosed a long position in RWWI. For reasons discussed later in this report, we are now adding the stock to our “Acquisition” model portfolio. Please note that we have also added our GeoNugget financial snapshot table in this report, something we will be doing in future reports.

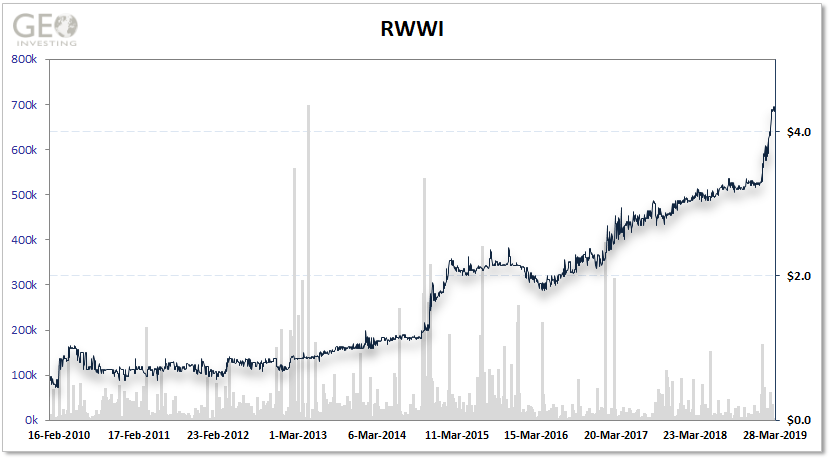

RWWI’s chart is one you probably wouldn’t mind seeing for every stock in your portfolio.

$5,000 invested in the stock in December 2010 at $0.53 (the average of the high and low for the month) would now be worth $40,550, which equates to a compounded annual return of 26%.

On its website, Rand Worldwide states it is a reseller of engineering and design software and describes itself as:

“one of the world’s leading providers of technology solutions and professional services to organizations with engineering design and information technology needs. Delivered through our different divisions, we provide comprehensive solutions that enable companies to better leverage technology, improve workflow processes, and enhance the skills of their people for increased competitiveness, productivity and profitability. At Rand Worldwide, we recognize that our future lies in delivering services and products that solve corporate mission critical problems, drive organizational efficiencies and increase profitability for our clients.”

More simply stated, from its website:

“Rand Worldwide is a leading provider of technology solutions and professional services to innovative engineering and design companies around the globe.”

When I perform research, I categorize stocks in lists, with related notes. These lists span more than 20 years. One of my personal lists, labeled “Tier One OTC Maybe Buy Later”, represents OTC stocks that may appeal to me at a later date. RWWI was on this list.

I came across the stock a few years ago and passed it up because I am not a huge fan of resellers (typically low margin businesses) and I believed the stock was trading way ahead of its valuation, since earnings per share growth was inconsistent and revenue fell sharply in 2009 and 2010. If I would have dug deeper, I may have realized that the company had a long operating history, is a top respected player in its industry and may have multiple recurring revenue streams.

These are instances where paying up for a stock may be appropriate, since at some point the earnings engine rapidly accelerates as revenue grows. Furthermore, the “Management, Discussion & Analysis” section of the company’s 2009 10-K points out that the global recession was the main culprit for the weak top line growth performance.

Total revenue for the year ended June 30, 2009 decreased by $14.2 million or 28.6% when compared to the prior fiscal year primarily due to the effects of the national recession on the Company’s customers. The business slowdown experienced by its customer base in the manufacturing, engineering and building sectors resulted in reduced purchases of the products and services that the Company offers.

Similar verbiage was present in the 2010 10-K.

Like the last “dark” OTC stock we profiled, TCOR, which stopped reporting with the SEC in 2003, RWWI ceased SEC reporting in 2015. However, RWWI does report limited financial data at OTCmarkets.com. Referencing past SEC filings, we can get some idea about what the company does, although it has made acquisitions since 2015.

“Rand Worldwide, Inc. is a leading supplier in the design automation, facilities and data management software marketplace. Rand Worldwide also provides value-added services, such as training, technical support and other consulting and professional services to businesses, government agencies and educational institutions worldwide.”

RWWI resells software owned by engineering software firms, such as:

RWWI’s relationship with the market leader, Autodesk, seems to be the main source of its revenue. The software RWWI resells helps customers design products, organize design workflow and manage assets. Per SEC filings, aside from providing training to customers, RWWI products are grouped into four categories:

- Design Automation

- Data Management

- Facilities Management

- Computational Fluid Dynamics

Design Automation

In the design automation market,

“Rand Worldwide focuses on providing enterprise solutions to small- and medium-sized businesses with under one billion dollars of annual revenue, primarily in the architecture, engineering, and construction (“AEC”) market and the mechanical design and manufacturing (“MFG”) market. The AEC market is comprised of design services focused on the construction of large physical assets such as buildings, roads, factories, utility companies, and commercial infrastructure projects. The MFG market is primarily focused on the design, tooling, assembly, and testing of instruments, electronic devices, machines, mechanical devices, and power-driven equipment.”

Here is how Javelin describes their design automation software:

“DriveWorks design automation software works in tandem with the very popular SOLIDWORKS 3D modeling and design software package. SOLIDWORKS is used to design just about any custom product with a wide range of features and functionality. It provides a platform for designing parts, assemblies and drawings, giving manufacturers an impressive ability to visualize product designs upfront. DriveWorks enables engineers to automate and standardize the tool design process.”

Data Management

From Autodesk:

“Helps design teams track work in progress and maintain version control in multi-user environments. It allows them to organize and reuse designs by consolidating product information and reducing the need to re-create designs from scratch.”

Facilities Management

This area focuses on tracking and managing the physical assets of a company:

“Integrated Workplace Management Systems (“IWMS”) and Computer Aided Facilities Management (“CAFM”) systems enable organizations to make informed strategic and business decisions that optimize return on investment, lower asset lifecycle costs, and increase enterprise-wide productivity and profitability. Organizations of all sizes, spanning the financial, educational, governmental, healthcare, and manufacturing industries, use these solutions to deliver timely, relevant facilities information as part of their strategic business plans.

Geographic Information Systems (“GIS”) permit users to link together disparate data files (maps, aerial photos, tax records, marketing data, etc.) and provide the user with a unified image and knowledge base of a specific geographic location or building location. When combined with information from a facilities management system, information from GIS applications provide an integrated facilities view that allows enhanced analysis in various spatial contexts for professionals responsible for asset tracking, maintenance, emergency preparedness, space allocation, and construction planning.”

Computational Fluid Dynamics

In the CFD market, the Company provides CFD analysis consulting and thermal simulation services to businesses primarily in the AEC and MFG markets. Here is what we learned about CFD:

“Computational fluid dynamics (CFD) is the use of applied mathematics, physics and computational software to visualize how a gas or liquid flows -- as well as how the gas or liquid affects objects as it flows past. Computational fluid dynamics is based on the Navier-Stokes equations. These equations describe how the velocity, pressure, temperature, and density of a moving fluid are related. Computational fluid dynamics has been around since the early 20th century and many people are familiar with it as a tool for analyzing air flow around cars and aircraft.”

GeoNugget Criteria Set

Year End : June 30

Data Ended 12/31/2019

- Price = $4.30

- Fully-Taxed Trailing EPS = $0.19

- P/E based on Fully-Taxed Trailing EPS = 23.1

Criteria Check List

RWWI Meets 8 out of 10 of our most important requirements for growth and risk-based quantitative data.

* See more on GeoPowerRanking

**The company has historically operated at a current ratio of under 1.

The changing industry landscape that RWWI is playing in has got us excited, and we believe it makes the company an ideal acquisition target. We see potential for over 100% upside, but we need to interview management to confirm some of our research. Multiple attempts to contact the company have been unsuccessful, but we will keep trying. In the meantime, as we disclosed on February 8 and March 14, we have taken an initial position. Our “Reasons for Tracking” are:

- RWWI easily debunks negative microcap stereotypes

- Recurring revenue aspect to RWWI’s business model

- Strong relationship with Autodesk

- RWWI could be an ideal acquisition candidate

- Operating leverage

Reasons for Tracking

1. RWWI is a Beautiful Example of Debunking OTC Microcap Stereotypes

You are probably aware of many of the negative stereotypes surrounding microcaps, including the assumption that they are all pump and dumps or development stage companies with barely any revenue. RWWI proves those stereotypes wrong:

- It has been around for over 20 years

- It is one of the largest resellers of Autodesk products

- It employs over 400 people in almost 50 locations across North America

- It has served over 25,000 customers

- It has an extensive sales database that contains several hundred thousand point-of-contact names collected over its history

RWWI's going public history began in October 1996 when, with about $9.5 million in revenue, Spatial Technology completed its initial public on the American Stock Exchange under the symbol SIY (prospectus not available online). SIY was a:

“…leading developer of three dimensional proprietary modeling software. The Company licenses its 3D modeling software to software developers, enabling them to incorporate advanced 3D modeling functionality into their applications. The Company's 3D modeling software is designed as an open, component-based software technology that is compatible with a variety of platforms. The Company's ACIS 3D modeling software products provide core 3D modeling capability for numerous commercial CAD software applications. In addition, the Company's 3D modeling software is licensed by leading universities and research institutions.”

In November 2000, SIY sold its proprietary modeling software business for $25 million to Dassault Systems in order to focus on its new PlanetCAD software reseller online platform that allowed manufacturing and design engineers to access and apply third party software to their needs. The stock symbol was changed to PCD. Then, in 2002, PCD completed a merger with software company Avatech to strengthen its Autodesk relationship and product offering breadth.

"This merger will allow us to continue our solid commitment to Autodesk (Nasdaq:ADSK) by strengthening the R & D efforts including an Autodesk platform-based product."

The name of the company was changed to Avatech Solutions, and it was listed under the symbol AVSO. Finally, in 2010, Rand Worldwide completed a reverse merger with AVSO:

“With little geographic overlap between the businesses today, the combination of Rand Worldwide and Avatech allows us to leverage the full range of selling and technical resources of each of the companies to enhance the service delivered to our clients," commented Dulude. “We believe that clients in all of the geographies we serve will reap the benefits of the very deep bench of technical service capabilities that will result from combining the two companies. Also, the ability to deliver the additional products and solutions that each company has to its respective customer bases represents an attractive cross selling opportunity.”

Steve Blum, Autodesk’s senior vice president of Americas Sales said, “Autodesk has been very pleased with the performance of these two significant channel partners and we look forward to the increased capabilities available with this combination.” All Autodesk related services and sales activities for the two companies will be combined under the IMAGINiT Technologies brand worldwide (IMAGINiT, purchased by Rand in 2000, is the largest North American value-added reseller of pre-packaged software product offerings developed by Autodesk).

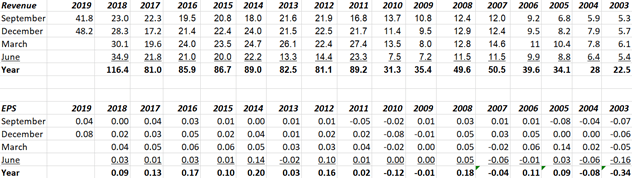

The new company is named Rand Worldwide, trading under the symbol RWWI. Throughout its history, the company has grown considerably, generating substantial revenue, while generally maintaining profitability:

Its revenue growth performance has certainly been lumpy and has hit periods of little, or no, growth. This has also been the case for the company’s EPS performance. With software companies, however, I am more interested in revenue growth and the level of recurring revenue.

The jump in 2011 revenue was due to an acquisition (merger), but it then flattened out until 2018 and 2019, due to four acquisitions made dating back to 2016. Without the luxury of SEC filings since 2015, it is going to be hard to determine what type of organic growth the company has been experiencing. However, we believe that recurring revenue, recent industry trends and an increased pursuit of M&A could be setting up RWWI for new elevated base-level EPS, and possibly a period of accelerated growth.

2. Recurring Revenue Stream

Here are RWWI’s sources of revenue:

- Product sales: revenue derived from licensing fees from the sale of third party software products

- Service revenue: Rand Worldwide provides services in the form of training, consulting services, software development, custom courseware development and technical to its customers.

- Support services are sold either in prepaid blocks of hours which typically expire in one year, or as annual contracts for unlimited support for a specified number of users and products supported. Prepaid support service revenue is recognized monthly based upon usage with unused balances recognized in full upon expiration. Annual support contract revenues are recognized ratably over the contract period

- Commission revenue: the Company offers Autodesk’s subscription programs, which entitle subscribers to receive software upgrades, web support and eLearning lessons directly from Autodesk.

- RWWI receives a commission from Autodesk. The Company earns a rebate from its primary supplier, Autodesk, for its qualifying renewal subscriptions, which increase gross profits and the corresponding commission revenues on such sales. The rebates on renewal subscriptions are paid monthly and are accrued in accordance with ASC 605-50.

I still need to dig into the recurring revenue components of the business, but from what I have figured out so far, service and commission revenue appear to be recurring (~50% of total revenue). As far as product sales go, it looks they have historically been generated through reseller arrangements through the sale of Autodesk perpetual licences. However, as of January 31, 2016, Autodesk stopped offering perpetual licenses for most individual Autodesk software products, in favor of a recurring subscription/SaaS model:

“For Autodesk products worldwide, we have phased out perpetual licenses of our software. Our current subscription offerings allow you to access multiple products and to share licenses just as you could with perpetual licensing. The way we design and build is changing rapidly, which also changes the tools we use and the ways companies and individuals buy and access software.

By subscribing, you receive a simplified customer experience, enjoy lower upfront cost, and have the ability to pay for Autodesk products and cloud services for the amount of time that is right for you: monthly, quarterly, annual, and multi-year term lengths (availability may vary depending on region or access type). Your subscription makes it easier to access your software and stay up-to-date. You will be able to subscribe to an individual product or a collection of products that can be used by a single-user or shared by multiple users. Providing subscription offerings with flexible packaging and licensing options protects the value of your existing investment in our technologies.”

Key questions we would like to get answers to, relating to product sales, are:

- Does RWWI only receive one initial payment from product sales, or also on renewals?

- Also, is it possible that Adobe will have its customers lean on its top resellers, like RWWI, for maintenance and support?

More importantly, the move by Autodesk to go to a subscription/SaaS model carries some potential benefits for RWWI:

- Retapping revenue from legacy customers who want to move to the cloud or who want to receive updated software on products no longer being supported by Autodesk, that may have been purchased through a perpetual license

- The opportunity to keep generating product revenue when Adobe’s new subscription model agreements end

- Autodesk could attract more customers and expand its market reach due to more flexible pricing inherent in a subscription model

3. Strong Relationship With Autodesk / Not Just A “Reseller”

70% of Autodesk’s revenue arises from its reseller relationships. One of things you might be asking yourself is: “Why does Autodesk need resellers?”

This is a relevant question, now that Autodesk is beginning to put more effort into direct to customer and online sales initiatives. However, this seems to be more of an issue for smaller resellers that can't give Autodesk scale. RWWI is much more than a reseller.

The company also develops intellectual property and add-ons that extend further functionality of Autodesk’s software. These types of resellers are known as Value Added Resellers (VARs). Regardless, Autodesk has stated that it is still going to rely heavily on its resellers moving forward. Autodesk’s 2018 10-K reinforces this:

“We anticipate that our channel mix will continue to change, particularly as we scale our online Autodesk branded store business and our largest accounts shift towards direct-only business models. Importantly, we expect our indirect channel (resellers) will continue to transact and support the majority of our future revenue.”

The effect of Autodesk abandoning its larger resellers could be devastating. Over the years, customer relationships have been developed through its reseller relationships. Furthermore, resellers also absorb a lot of costs, such as training and customer service. For example, take a look at these passages I found on the web:

“Would you like to talk to a human easily when you have a licensing hiccup, or upgrade? Then go for a reseller.”

“Are you very sure which of the products from Autodesk is the best for you/your company? They have a lot of products for different branches, but you can't call them and ask which one is the best for your workflow(s).”

“Also for AutoCAD (and AutoCAD based verticals) there exist a lot of plugins and applications, which might bring you additional value ... Autodesk does not sell 3rd party applications. Could be an important difference.”

Our opinion that RWII’s position with Autodesk is strong has been confirmed by their consistent receipt of top reseller awards from Autodesk, especially in recent years.

G2Crowd provided its list of top 47 Autodesk resellers for 2019. Two of RWWI’s major offerings, Ideate and Imaginit, showed up on the list. Ideate was acquired by Imaginit in 2017. Both of these companies are serial Autodesk award winners.

Ideate, Inc., an Autodesk Platinum Value Added Reseller,

“…announced today that it was named the 2017 Autodesk North American Platinum Award winner in the New Subscriptions Sold category. Autodesk announced Ideate as the selection for this award at a celebration at the Autodesk One Team Conference in Las Vegas on February 2017.

“I was honored to receive this award, especially in this inaugural year of Autodesk’s subscription model,” said Bob Palioca, president of Ideate, Inc. “It indicates that our team achieved its goal of clearly conveying the benefits of this new model to customers and that customers trust us to help them get the most out of their Autodesk software investment.”

Ideate has been an Autodesk reseller since 1992. Since that time, it has received many Autodesk Platinum Awards, including the 2016 Channel Marketing Partner of the Year award, the 2015 Reseller of the Year award. Raymond Savona, vice president of America Sales, Autodesk said, “Ideate demonstrated its commitment to providing Autodesk solutions to its customers in the architecture, engineering, construction communities. We are happy to recognize their FY17 accomplishments with this award.”

For the fifth year in a row,

“IMAGINiT Technologies has been awarded a coveted Autodesk Platinum Club Award at the Autodesk One Team Conference in Las Vegas, Nevada. For the 2018 Autodesk fiscal year, IMAGINiT has been named Top Reseller in New Subscriptions Sold in the US and Canada.”

“The Autodesk Platinum Club Awards recognize an elite group of global partners for top sales performance and customer service,” says Ken Manoff, senior director, Americas Channel Partners, Autodesk. “We’re excited to see IMAGINiT’s consistent value to customers. Thanks to the entire IMAGINiT team.”

The big takeaway from the recent award wins is that RWWI is leading the way to converting and/or on boarding new customers to Autodesk’s new subscription offering. Here is a quote from RWWI’s 2015 third quarter press release:

“As evidenced by our year to-date results, our businesses are doing well and our revenues and profits continue to grow,” stated Lawrence Rychlak, president and chief executive officer at Rand Worldwide. “We continue to invest in the future growth of our Company as well as in preparation for the anticipated changes in the Autodesk marketplace. Due to the competitive advantages that our size and our breadth of sales and technical talent across North America provide for us, we are very well positioned to prosper as Autodesk moves through its business transformation over the next few years.”

Finally, this quote from RWII’s 2014 10-K highlights that the company is a top sales generator for Autodesk:

“Through a disciplined approach to sales and a heightened attention to customer satisfaction, the Company’s renewal rates on its Autodesk subscriptions are among the highest in the sales channel.”

4. Industry Tailwinds Positioning RWWI as an Ideal Acquisition Target

Overall, the moves that Autodesk is making should benefit larger resellers. Smaller resellers are going to shut down or be gobbled up by leading resellers, likely at attractive valuations. The bigger the reseller, the better "moat" it will have with Autodesk. This is leading to an increase in the acquisition activity going on in the space.

“At one point, the Autodesk VAR channel was the envy of all its competitors. Over time and changing its business model, Autodesk now goes more direct at the enterprise level and online for subscriptions. The net result of this has been VARs shutting down or selling off to larger, resellers that have more diverse incomes. With smaller resellers like ourselves coming under continued margin pressures, we became concerned that longer term we wouldn’t be able to continue to deliver the specialized resources and solutions that our customers across the UK need,” explained Peter Hurst.”

Oleg Shilovitsky (Twitter handle: @olegshilovitsky) published an excellent article on his blog, “Beyond PLM (Product Lifecycle Management)”, that discusses the future of resellers due to the changes Autodesk is making. This quote sums it all up:

“Here my prediction. VAR (Value Added Resellers) consolidation process can end up by the event of CAD vendor acquiring resellers network. Can Dassault Systemes buy all its Solidworks VARs? It might be not as crazy as you might think about. Historical example – acquisition of IBM channels by Dassault Systemes back in 2009. Check this old article by Dasault Systemes – PLM Consolidation Continues—Dassault Systèmes to Acquire IBM PLM.”

“What is my conclusion? We are going to see future centralization and consolidation of resellers. Existing resellers will have to live in a new word of CAD online services and digital transformation. We might come to the situation in which companies like Autodesk or Dassault Systemes, will buy a small group of consolidated resellers (one big reseller per country). At the same time, we can see an increased amount of resources and digital services provided by new digital marketing and digital resellers channels. Just my thoughts…”

Autodesk has a network of approximately 1,600 resellers and distributors worldwide (Autodesk transacts directly with resellers or through distributors), with about 50 that rank high.

When we think of potential suitors aside from companies like Autodesk, a case could be made for some type of deal with large competitors, like those that RWWI mentions in past SEC filings, that could fill in gaps of customer coverage. For example, Tata is a larger firm than RWWI, but its Autodesk business is less than RWWI. Also, Mensch und Maschine Software (M M) might benefit from RWWI’s North American exposure.

“Tata is a systems integrator for design automation products with offices located in 25 countries and has headquarters in the United States, the United Kingdom, India, and Singapore. While the Company believes that Tata has greater revenues than Rand Worldwide, the Company estimates that the Autodesk portion of Tata’s business is less than the Company’s Autodesk business.”

“M M is one of the leading European providers of computer aided design and manufacturing solutions with more than 50 offices located across the world and headquarters in Germany. M M is the largest European Autodesk value-added reseller; however, the Company believes that M M’s Autodesk-related business in Europe is comparable to the Company’s Autodesk-related business in North America.”

The M&A activity that has made RWWI what it is today clearly shows that scale and size are important and that current and legacy management probably anticipated a day would come when Autodesk would make changes that would threaten smaller resellers.

Now, it looks like they're once again aggressively pursuing acquisitions, completing four acquisitions since 2016. Opportunities will continue to arise, as many “VARs can’t or don’t want to transition to a subscription world.”

Here is a snapshot of the company’s going public and acquisition history, on its way to becoming a VAR leader:

- September 1996 – Registration of shares as 3D Software company, Spatial Technology, IPOs

- 1999 - Spatial sells proprietary software division to focus on building its reseller platform, PlanetCAD (new company name)

- October 2002 - PlanetCAD completes a merger with software company, Avatech (new company name)

- On April 8, 2005, the Company acquired all of the assets, and assumed certain defined liabilities, of Comtrex Corp. Comtrex, that had developed a similar strategy by emphasizing service offerings in connection with the sale of Autodesk products

- May 30, 2006 - Acquisition of Sterling Systems & Consulting. (pg. 5 10K)

- August 2010 - Becomes RWWI when Rand Worldwide goes public through reverse merger with Avatech, making the combined company Autodesk’s largest VAR

- March 2012 - Acquires certain assets of Virginia Beach based Inlet Technology. Inlet Technology is an Autodesk technology integrator, channel partner and services provider primarily focused in the architecture, engineering and civil industry and as such will be incorporated into the IMAGINiT Technologies division of Rand Worldwide.

- August 2012 - Acquires certain assets of Charlottesville, Virginia-based Informative Design Partners (IDP). IDP delivers computational fluid dynamics (CFD) analysis consulting and thermal simulation services that provide design insight allowing customers to make better informed design decisions without distractions to their current development processes.

- November 2016 - IMAGINiT Technologies division acquires the Autodesk subscription customer base of Eagle Point Software

- March 2017 - IMAGINiT Technologies division has acquires PacifiCAD, an Autodesk Gold Partner headquartered in Spokane, Washington.

- April 2017 - IMAGINiT Technologies division acquires Advanced Technologies Solutions (ATSI), an Autodesk Gold Partner headquartered in Jacksonville, Florida.

- April 2018 - IMAGINiT Technologies and Ideate merge their Autodesk businesses resulting in one company offering many solutions to their combined customers.

5. Operating Leverage

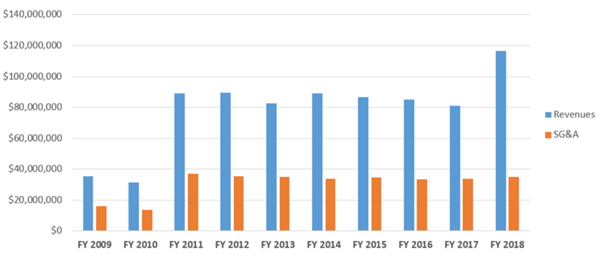

Operating leverage in a business occurs when Sales, General & Administrative (SG&A) expenses grow at a slower rate than revenue. It looks like the company has been experiencing the benefits of some nice operating leverage in recent quarters.

Looking at the past ten years, the existence of operating leverage is not clear, since revenue levels were pretty flat through most of the period. However, 2018 provides us with a hint that RWWI does exhibit some operating leverage, since SG&A remained flat as revenues rose nicely.

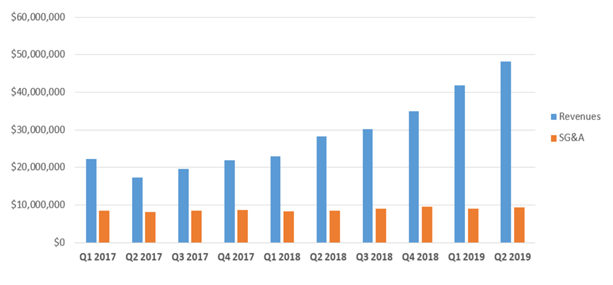

Moving over to quarterly financial trends since Q1 2017, it’s clear to see that a good deal of operating leverage does exist.

Caveats

- A pressing caveat to consider is the margin pressure that resellers are feeling as they compete for business to reach or maintain their market dominance needed to be valuable to Autodesk.

- Gross margin has been falling from ~51% in 2016 and 2017 to ~35% in 2018, confirming this (as does the sharp fall in operating margins since Q1 2017).

- However, as we mentioned, it also looks like SG&A may be flattening out which is part of what has been driving earnings per share growth in recent quarters, which is driving operating margins back to 2017 levels.

- We would like to understand how Adobe’s business shift could impact RWWI gross margins.

- Regardless of our assumption that the company's position with Autodesk is strong, we can't ignore the fact that Autodesk is beginning to focus more on selling direct to the customer.

- We still need to gain clarity into how the company recognizes product revenues from Autodesk’s new subscription model.

- Has had outlier EPS quarters in the past

- Recessions can have a severely negative impact on the financials

- The company’s product sales are somewhat cyclical, and increase when the developer of a specific software product releases a new version, offers promotions or discontinues support of an older product.

- Something else we also want to dig into is if the company has plans to expand outside of North America. From what we can tell, it looks like the main focus of the company is the North American market.

- Current ratio is below 1, however the company has historically operated at a current ratio between .6 and 1.8.

Valuation

How do you value a reseller, where margins are typically low, compared to other software models? Because it appears that most revenue might be recurring now, and because of industry trends strengthen its competitive position, we think higher valuations than we would normally assume are appropriate.

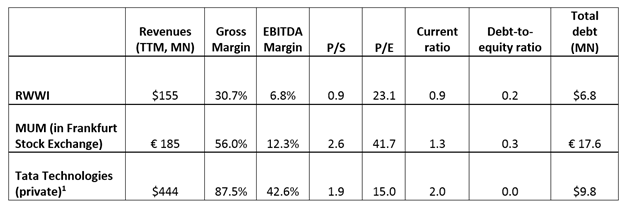

Here is a look at some of RWWI’s valuation multiples vs. some of its comps:

Note 1: Numbers for Tata Technologies are based on the disclosures from its website.

Currently, the company is trading at P/S of 0.9. We think a 2x multiple would be more appropriate. This would imply a price of $9.9 price, or 129% upside from current levels. Ultimately, we believe that RWWI is an ideal acquisition or merger candidate.