In our October 24th, 2018 email, we mentioned that we were ramping up our OTC pipeline and that we wanted to delve into Fitlife Brands, Inc. (NASDAQ:FTLF) a bit more to see if new the CEO, who joined earlier this year, has put the company on a path to consistent growth - something that has not occurred over the last several years.

We were are intrigued that the new CEO has been aggressively buying shares, even as the stock hits new highs. We are not huge fans of FTLF but a few members asked us to take a closer look at the company. You can see a comprehensive report by a GeoInvesting member Avram Fisher, who was slightly bullish on the company at one point in 2016, but did a good job highlighting the uncertainties surrounding its comeback story. The stock did experience a brief run-up and Avi eventually turned bearish on FLTF. You can see his latest update here.

Fitlife manufactures and markets nutritional supplements for health conscious consumers in the United States and internationally. FTLF offers various nutritional supplements for health conscious consumers marketed under the brand names NDS Nutrition Products™, PMD®, SirenLabs®, CoreActive®, Metis Nutrition™, iSatori™, Energize and BioGenetic Laboratories.

The company operates in a very competitive environment and the majority of its products are sold through $GNC. It has been carrying out a multi-year restructuring to address stagnant growth from the widely publicized challenges GNC has been facing growing its brick and mortar locations. Until FTLF expands its market reach, the uncertainty over whether GNC’s turnaround will be successful is the main caveat.

Despite GNC management’s vote of confidence, the company is still struggling to execute. GNC reported 2018 third quarter financial results on November 9, 2018 and the story seems to be not improving at all. Management is currently banking on a partnership in China to reignite growth. We don’t know what this means for FTLF and, to be honest, we don’t have a high confidence level that GNC is near solving its problems. Customer concentration risk is something we don’t like to normally invest in, unless certain criteria are met.

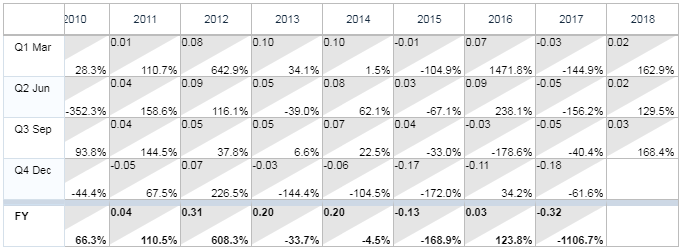

Here is a look at GNC’s share performance over the past several years:

And here is a look at FTLF share performance over the same period:

FTLF is also dealing with a product recall issue. However, we are still willing to take a look at FTLF and track its progress for a few reasons that could improve investor sentiment in the short-term:

-

New interim CEO in place

-

CEO loading shares in the open market

-

Profitability reestablished

-

Amazon.Com, Inc. (NASDAQ:AMZN) gives the company an on-line presence

Ultimately, we think the best scenario FLTF may want to take is to sell the company to a suitor that can immediately monetize its proven brands into a broader customer base. In our opinion, the reliance on GNC is just too large and will take significant time and effort to create a dent in the customer concentration risk.

Reasons for Tracking FTLF

1. Investor Becomes Interim CEO – But the Jury is Still Out

In February 2018, the company named Dayton Judd as interim CEO. As we have mentioned on several occasions, we are attracted to CEOs that come from an investment or private equity background. GVP and HICKA are two stocks that we own and have written about that fit this mold. We also need to be mindful that following this game plan will not deliver a 100% batting average, as was the case with CRTN. See our initial coverage on these three stocks:

Below is Dayton’s full company profile:

Dayton Judd has served as a director of the Company since June 2017, is currently the Chairman of the Company’s Board of Directors, and was appointed Interim Chief Executive Officer of the Company on February 18, 2018. Mr. Judd is the Founder and Managing Partner of Sudbury Capital Management. Prior to founding Sudbury, Mr. Judd worked from 2007 through 2011 as a Portfolio Manager at Q Investments, a multi-billion dollar hedge fund in Fort Worth, Texas. Prior to Q Investments, he worked with McKinsey & Company from 1996 through 1998, and again from 2000 through 2007. Mr. Judd serves on the Board of Directors of RLJ Entertainment (NASDAQ: RLJE). He graduated from Brigham Young University in 1995 with a bachelor’s degree, summa cum laude, and a master’s degree, both in accounting. He also earned an MBA with high distinction from Harvard Business School in 2000, where he was a Baker Scholar.

The jury is still out on Judd’s investment prowess. While RLJE did get acquired at $6.25 in July 2018, it looks like Judd first bought the stock at around $11.50 (adjusted for a 1 for 3 reverse split). Shares reached a low of $2.97 (split adjusted) since his first entry. To his credit, Judd was a consistent buyer, lowering his average cost. And, when Judd joined the board in 2015 to take a more active role in the company, the stock was around $3.00 (split adjusted).

2. Judd Backing Up the Truck

Investing alongside microcap insiders has been working remarkably well of late, even in lesser quality names. Because of this, we think it’s worth taking note of the insider activity taking place at FTLF.

Judd’s interest in FTLF began in September 2015 when his fund disclosed a 5.37% ownership stake in the company at a price of around $1.50. And like RLJE, shares went into a tailspin, reaching a low of $0.19 in December 2017. What has caught our attention is that after a 5-month hiatus, Judd is back in the market aggressively buying FTLF. Since late May 2018, he has purchased around 465,000 shares between $0.27 and $0.50 in several transactions, including 45,000 shares on November 15. He was also awarded 450,000 shares on July 31, 2018. Judd probably has no choice but to add shares, to lower his cost and justify his move to his investors. He now owns ~16% of the company and we would not be surprised if Judd eventually pushed for a sale of the company.

Furthermore, Judd also participated in a small raise to help fund the company through what is expected to be a tough Q4 2018.

“On November 13, 2018, the Company raised $0.6 million through the sale of preferred stock to a small number of investors, including two members of the Company’s board of directors.”

The deal is not horribly dilutive, but added about 13.7% more shares to the diluted share count.

3. Progress

Profitability

While quarterly sales growth has mostly been negative, the bleeding may have stopped, at least for now.

For its Q2 2018 the company reported:

For its Q3, FTLF reported:

FTLF has now reported positive EPS for 3 straight quarters.

It is a little concerning that after Q2 2018, management felt that the outlook at GNC was improving…

“the trends affecting GNC and the overall retail segment have stabilized, and, while no assurances can be given, the prevailing demographics suggest a growing demand for nutritional supplements.”

…but in its Q3 2018 release, the tone regarding GNC was not as bullish and FTLF noted that they expected to experience a challenging Q4, before seeing a rebound in 2019:

“We continue to face revenue pressures with our brick and mortar retail partners, driven by declining traffic and lower sell-through at retail. The fourth quarter is seasonally difficult in the supplement industry, and the Company will use the proceeds to strengthen its working capital and position the company for the seasonally strong first half of the year.”

FTLF is tracking at a P/E of 7.6x if you annualize the first 9 months of 2018 (which is probably an aggressive assumption since the company expects to experience a tough Q4). Its EV/S is 0.39x and its P/S is 0.45x.

Multichannel Vision

Management is attempting to lessen its reliance on brick and mortar by adopting an omnichannel approach:

Omnichannel -- also spelled omni-channel -- is a multichannel approach to sales that seeks to provide customers with a seamless shopping experience, whether they're shopping online from a desktop or mobile device, by telephone, or in a brick-and-mortar store.

Like many companies are doing, part of this strategy includes turning to AMZN. In its Q2 2018 report, management seemed encouraged with its e-commerce push through AMZN.

"I am particularly excited about the early success we have had on Amazon, which has shown impressive initial growth since launching early in the second quarter. In all that we do, we remain committed to growing shareholder value"

We do not see any detail in the 10-Qs regarding the relationship, but the products are being offered on Amazon which, over time, should be a nice added sales outlet for the company. However, AMZN is still an insignificant contributor to overall revenue right now.

"While significant challenges and uncertainties remain, I am encouraged by our return to profitability for both the three and six month periods ended June 30, 2018. We continue to work closely with our single largest customer to create value for FitLife and our distribution partners with a renewed focus on developing innovative products across all our brands. We are hopeful that this commitment, in concert with our new omni-channel approach, will return the Company to revenue growth," said Dayton Judd, Chief Executive Officer of FitLife Brands.

4. Liquidity Position Has Improved

FTLF’s liquidity position has been hampered by extended accounts receivable due to GNC. In order to alleviate this stress, provide the company with working capital and retire all its debt, management has been entering into factor agreements to sell these receivables:

From Q1 2018 Press Release:

“Second, we began factoring select receivables during the quarter, which has provided the Company with enhanced liquidity and, perhaps more importantly, enabled the Company to pay-off all remaining debt obligations and end the quarter debt-free,” stated Dayton Judd, Interim Chief Executive Officer of FitLife Brands.”

From various 10-Qs:

“In December 2017, the Company, through its wholly-owned subsidiaries, NDS and iSatori (together, the “Subsidiaries”), entered into a Merchant Agreement (the “Merchant Agreement”) with Compass Bank, d/b/a Commercial Billing Service (“Compass”). Under the terms of the Merchant Agreement, subject to the satisfaction of certain conditions to funding, the Subsidiaries agreed to sell to Compass, and Compass agreed to purchase from the Subsidiaries, certain accounts owing from customers of such Subsidiaries, including GNC. All amounts due under the terms of the Merchant Agreement, totaling up to $5.0 million, are guaranteed by the Company under the terms of a Continuing Guarantee.”

“On January 22, 2018, the Subsidiaries sold to Compass accounts receivable under the Merchant Agreement aggregating approximately $2.0 million, the proceeds from which were used to pay U.S. Bank N.A. (“USB”) all principal and accrued interest due and owing USB under the terms of certain promissory notes previously issued to USB (the “Notes”).”

And the recent financing combined with the product recall risk nearing an end should put less stress on liquidity in the near-term.

“As previously disclosed, during the fourth quarter of 2017, the Company established a reserve to account for the pending return of several iSatori products from our largest retail partner. Although the Company has not fully exhausted the reserve, the majority of those returns have occurred, resulting in the Company using substantially all of its cash generated from operations year-to-date to pay for those returns.”

We will look to interview management to learn more about the company’s transformation, how much more profitability can be squeezed out of the company at current revenue levels and the outlook for quarterly revenue levels beyond historical highs of around $6 million. It is worth noting that the company does experience some seasonality, as well, which we are cognizant of.