By Maj Soueidan, Co-founder GeoInvesting

Cas Medical Systems, Inc. (NASDAQ:CASM) ($1.90, $52.5M market cap) is a medical technology company which develops, manufactures, and markets non-invasive patient monitoring products worldwide. We first mentioned that CASM entered our radar after I spoke with the Company at the LD Microcap conference in early June. On June 25, 2018, we disclosed our long position and added the stock to our Mock Takeover Candidate portfolio. Some of you might appreciate that CASM has been trading with more liquidity than the typical microcap stock we discuss at Geo.

With its best in class solution, CASM is a $20 million company addressing an immediate $125 million and ~$1 billion long-term market opportunity. We are impressed with the CEO’s track record, the market potential of the product, the recurring revenue model and the fact that the company could be on the brink of profitability. We feel the company’s recurring revenue model has reached an inflection point that will lead to consistent and accelerated revenue growth.

The company is stealing market share from the leading player (~70% share of the market down from 100%), who is selling an inferior solution that had a first mover advantage. With ~20% of the market, CASM could displace the leader and capture a large piece of their revenue. It may take another year for the company to achieve profitability, but we are currently taking a longer-term view on CASM as a possible multi-year hold for some of our position.

Using a range of assumptions, we believe the stock has ~30% to ~100% upside from current levels over the next year and half, but these targets do not consider the very likelihood of upside revenue surprise and the long-term growth potential. However, we are prepared for and would welcome a near-term pullback in shares, given the recent strong run up. We also believe CASM may shape up to an interesting acquisition target as we enter 2019. There are only 4 major players in the space, and CASM, supported by independent research, appears to be best in class.

The company’s main product is called FORE-SIGHT (and FORE-SIGHT ELITE), a cerebral (tissue) oximeter medical platform, which provides non-invasive and quantitative measurement of oxygenation for cerebral tissue during surgery or critical care situations. CASM competes against other tissue oximeter and pulse oximeter companies.

“With a simple non-invasive adhesive sensor applied to the skin, tissue oximeters alert clinicians to the oxygenation levels of a patient's brain or other body tissue during medical procedures to avoid harm caused by insufficient oxygen (desaturation), otherwise known as hypoxia.”

FORE-SIGHT works by emitting Near Infrared (NIR) light into tissue to measure the saturation of oxygen in Hemoglobin being delivered to tissue.

“Hemoglobin is the protein molecule in red blood cells that carries oxygen from the lungs to the body's tissues and returns carbon dioxide from the tissues back to the lungs.”

Over 90% of revenue comes from FORE-SIGHT being used in cardiac (heart) surgical settings. Below is an image of the product (Monitor and Disposable Sensors) in action from the company’s June 2018 PDF investor presentation and an interactive presentation here.

Oxygen Levels (right and left side of brain)

The CEO’s Track Record

Before we get into more details about the product and the market opportunity, it’s important to discuss the successful track record of the CEO, Thomas Patton. As we stated in other articles/notes, especially microcaps, investing in good management teams is an essential ingredient for success. Our interviews with management and management’s backgrounds can make or break our investment decisions. In the case of CASM, it was the overriding factor in our decision, given that the company is losing money.

Tom's career began in Washington DC as a criminal defensive litigator. It turned out that a lawyer adjacent to his office was working on a leveraged buyout deal of some orthopedic assets out of Dow Corning. The company was called Wright Medical, now public under the symbol Wright Medical Group (NASDAQ:WMGI). Patton was recruited to be general counselor for Wright Medical in 1993. In 1998 he accepted an offer to be CEO. At 33 years old he thought “why not, the company was already screwed up because of botched restructurings attempts by three past management teams, how could I make it much worse?” Patton divested non-performing assets and laid off half the workforce. Wright ended up growing at two to three times the industry average and was sold to Warburg Pincus in 1999.

Warburg Pincus specializes in private equity investing. Established nearly 50 years ago, Warburg Pincus has invested more than $50 billion in more than 720 companies in more than 35 countries around the world. The Chicago Tokyo Group currently manages Wright Medical Group, Inc. Japan on behalf of Warburg Pincus.

Pincus then took the company public in 2001.

Patton’s next stop was at a public company, Novametrix (old symbol: NMTX) that specializes in cardio-respiratory monitoring equipment. Novametrix had about $55 million in revenue. Patton ran the company for 2 years, before selling it to Respironics (a sleep apnea focused company, old symbol: RESP) in 2002 in a stock deal valued at $85 million. Patton fought for a stock deal since at that time, Respironics stock had taken a hit on a weak quarter. But, Patton and his team really liked Respironics, it was growing 20% per year for some time, as was its industry. Five years later, Koninklijke Philips (NYSE:PHG) acquired Respironics for $5.1 billion. Patton commented that Novametrix shareholders who held their shares would have experienced a 6x return.

He later worked as a consultant for a private equity firm as an advisor in the healthcare space and started (self-funded) a new medical device company in 2003, QDx, with a couple doctors who had developed a medical device in the hematology space. They sold the company to Abbott Laboratories (NYSE:ABT) in 2008 for a large upfront payment plus a royalty stream.

Given Tom’s past success, we think the chances are high that he will eventually reward patient CASM shareholders with a sale of the company at higher valuations.

Tom Finds a Hidden Gem and Divests of Money Losing Divisions

CASM came calling in 2010 and at first, Tom was unimpressed and hesitant to join the company. Although CASM was generating revenue, sales had fallen from $38 million to $24 million in 3 years and the company was losing money, selling low margin, commodity medical products. After a deeper look, Tom noticed that the company owned some cerebral tissue oximetry technology (FORE-SIGHT) that could be a homerun for CASM. At that time, FORE-SIGHT was a tiny portion of overall revenues and underdeveloped. FORE-SIGHT was essentially still in the R&D phase, not user friendly and too expensive. Tom decided to take the challenge. The Company redesigned the FORE-SIGHT first generation monitor and introduced a much lower cost next generation monitor in late Q3 of 2013. The redesign eliminated expensive laser-based technology and substituted LED technology instead with improved performance and additional user features and benefits. After some failed attempts in the turnaround of dying legacy products (minimal capital was devoted to legacy), CASM shut down or divested of all the legacy assets over 5 years and focused on FORE-SIGHT:

- On October 26, 2015, the Company sold certain assets related to its 740 SELECT vital signs monitoring product line in exchange for $220,000 at closing and a one-year promissory note in the principal amount of $329,967.

- On March 28, 2016, the Company sold its neonatal intensive care disposables product line assets in exchange for $3,350,000, including $3,035,000 paid in cash at closing.

- In early January 2017, it finalized the divesture of its neonatal disposable product line.

- In July 2017, the Company sold its OEM non-invasive blood pressure business to a third party for $4,500,000 at close and an earn-out of up to $2,000,000 payable in the third quarter of 2019. The Company is confident that it will receive some or all of the earn-out payment.

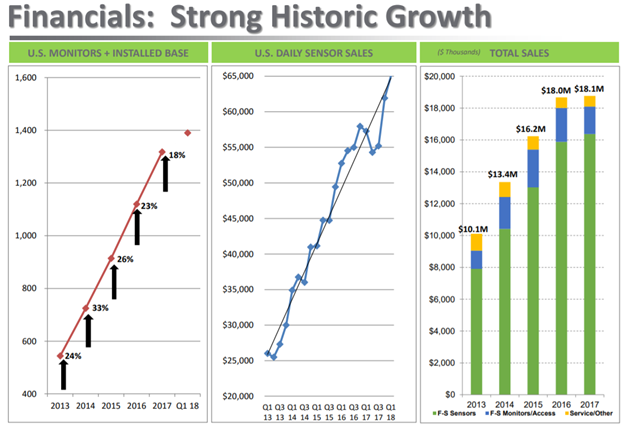

CASM positioned itself as a high margin, high growth, disposable product business. The next step was for the company to get more of its monitors into hospitals, so it could sell more of its disposable sensors. Each monitor averages about $12,000 in sensor sales per 12 months. So, with a new sales leader in place in late 2015, the company decided to revamp the sales organization, basically replacing the entire staff, 21 of 26. FORE-SIGHT’s growth rate basically went to zero, as it took some time for the sales reps to gain traction. However, it looks like the revenue inflection point has arrived.

CASM reminds me a little of “Run to One” selection TSSI that we profiled in June 2017. TSSI’s new CEO, Anthony Angelini, joined the company (in 2013) when he noticed that old management was not concentrating on driving its highest margin and most promising business unit. Like Tom, Anthony initially attempted to save TSSI’s low margin business units, but eventually sold them to grow its high margin, more predictable revenue business.

Sales Reach an Inflection Point

While overall revenues have been relatively flat over the last 4 years mainly due to the company’s dying legacy business, which masked the positive growth trends with FORE-SIGHT, the sales inflection point occurred in mid-2017, when FORE-SIGHT revenues bottomed and the new sales force matured. Since then, sensor revenues have resumed their historic uptrend.

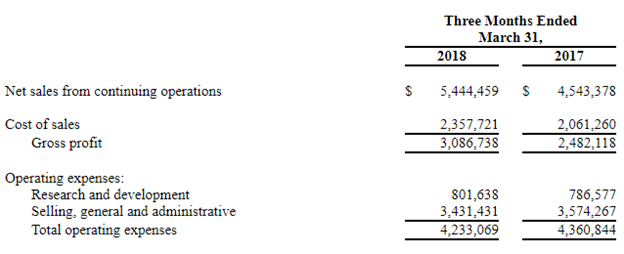

In early May, CASM reported strong Q1 2018 top line results with total sales of $5.4 million up 20% from the prior year of $4.5 million.

“Among the highlights, total FORE-SIGHT sales increased 22% from the prior year and featured a 21% increase in U.S. FORE-SIGHT sales. A record 111 monitors were shipped during the quarter, of which 72 were placed with U.S. customers. This follows a record 80 monitors shipped domestically in the fourth quarter of 2017. We ended the first quarter with a 25% increase in our domestic installed base over the prior year.”

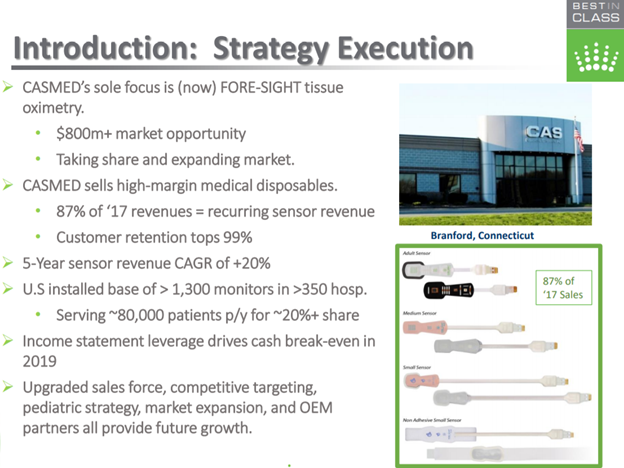

CASM Now boasts a 99% customer retention rate, with 87% of revenue coming from its recurring sensor sales which should enable sales to build on their historical momentum.

Nearing Profitability

One of the instances where we consider investing in companies that are losing money is when they are building a recurring revenue business. These companies can become very attractive to larger firms that can acquire revenues and eliminate costs through synergies with their own business. Still, we would prefer to find companies where recurring revenues are nearing a point where profitability can be achieved, and cash flow can support growth, reducing the risk of dilution.

CASM Appears to getting closer to cash flow breakeven:

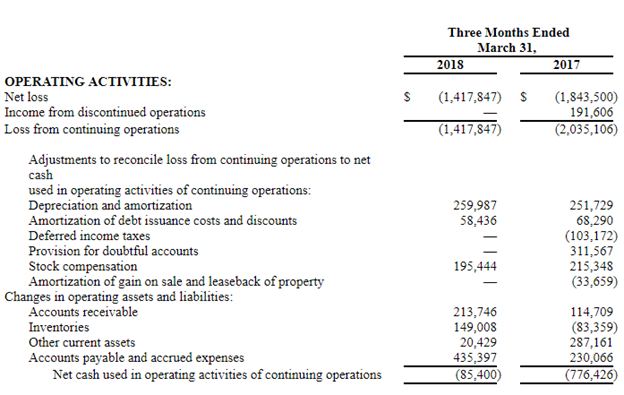

In its June LD presentation, management has stated it believes the company can reach EBITDA break-even by Q4 2018 and cash flow break-even in mid-2019. With the anticipated growth in the business and a recent debt refinancing, replacing a conventional loan (principle and interest payments) with an 18-month interest only loan (that then amortizes over 30 months), the company believes it has sufficient capital in place to support operations through at least May 2019. Management believes it is nearing cash flow breakeven as the business scales.

“With the divestiture of the Company's last legacy product line during the third quarter of 2017, CASMED is now singularly focused on its FORE-SIGHT tissue oximetry line of products. We believe that the transformation from a lower margin, commodity, capital equipment business into a high-growth, high-margin business is complete. Our FORE-SIGHT disposable sensor sales accounted for 87% of total sales for the first quarter of 2018. During the first quarter of 2018, the Company began to take initial deliveries of its lower cost FORE-SIGHT ELITE disposable sensors which are expected to substantially improve gross profit margins, the full impact of which should be recognized effective with the third quarter of 2018. Management believes that these improvements should accelerate the Company's path toward sustainable positive cash flow.”

We don’t think it’s unreasonable to assume that the company could breakeven on a quarterly basis at a revenue level of about $6.5 million which we think can occur by Q2 or Q3 2019. At scale, medical device companies can tend to carry favorable gross margins. Here is a look at the gross margins of the three major players that sell tissue oximetry product:

- Invos (before it was acquired by Covidien who was then acquired by )

- Masimo Corp (NASDAQ:MASI)

- MDT

We calculate that at $6.5 million in revenue, CASM would need to reach a gross margin of about 68% to breakeven. Given the gross margins of the comps , we do think 65% gross margins are within reach for CASM, sooner rather than later. Furthermore, we think SG&A will flatten out as sales increase. Notice that SG&A actually decreased in Q1 2018, even as sales rose sharply.

(Please note that Invos gross margins of 86.7% are unrealistic since at this time it was the only real player. Also, the gross margins of MASI and MDT are on a consolidated basis since the companies do not break out the margins of each product segment).

Reaching an inflection point with a recurring revenue model that is about to turn profitable could make the company a prime acquisition target.

Here is a snapshot of where CASM stands today:

The Importance of Monitoring Oxygenation Levels

Healthcare solutions that improve patient outcomes and save the system money get our attention.

Hypoxemia is a condition that occurs:

“when the level of oxygen in the blood falls below optimal levels—is a risk during surgery when patient breathing and ventilation may be affected by anaesthesia or other drugs.”

Hypoxemia is recognized as one of the most serious risks patients face during anesthesia and surgical care. A host of negative outcomes can occur if the level of oxygenation in the brain becomes too low during surgery (particularly urgent when a patient is under anesthesia), even for a short period of time. The most severe negative outcome is associated with cerebral hypoxia during surgery that can lead to brain damage or death that can begin to be a problem in less than 5 minutes.

Others side effects include:

- dizziness (vertigo) or lightheadedness.

- changes in vision including blurring or double vision.

- sudden falls (drop attack)

- slurred (or garbled) speech.

- numbness or tingling in the extremities or face.

- sudden uncoordinated movements.

- sleepiness.

- Stroke

For over 30 years the standard of care to monitor Hypoxemia has been the use of medical device called a pulse oximeter, typically placed on a finger, earlobe or a toe, and has become an essential component of operating room technology to detect, treat, and reduce the degree of intraoperative hypoxemia in the developed world.

“a non-invasive medical device that checks the level of oxygen in a patient’s bloodstream and sounds an alarm as soon as it detects the slightest unsafe change. A small probe, attached to a separate computerized unit, is clipped to a spot on the body with good blood flow – typically the finger or the earlobe.”

“A pulse oximeter is the most important monitoring tool in modern anesthesia practice.”

“Before the widespread adoption of pulse oximetry in the 1980s and the establishment of anesthesia monitoring standards in the 1990s, hypoxemia was the leading cause of anesthesia-related mortality.”

When oxygen levels get too low, physicians can act to reverse the condition during or after a surgery has been suspended (could be as simple as turning the head). To be clear, before CASM came along, the adoption of pulse oximetry technology has improved patient care as anesthesia-related mortality has dropped nearly 20-fold.

Other conditions that can occur due to low levels of oxygen delivery to the brain include:

- Ischemia, a decrease in blood flow to the brain caused by inadequate cardiac output, occlusion of cerebral vessels, or increased intracranial pressure (inadequate volume of supply), can lead to stroke

- Anemia: a decrease in the concentration of red blood cells in the blood (inadequate oxygen carrying capacity).

Why CASM’s Solution is Important - and Best In Class

Pulse oximeters have certainly done their part in improving patient care, but studies conclude that hypoxemia (even when oximeters are used) is still a significant problem in the operating room. One study concludes that a surprisingly high percentage of patients experience sustained hypoxemia during surgery:

- Even in highly advanced surgical settings, approximately one in 15 patients experienced hypoxemia for at least two consecutive minutes, and…

- …one in 64 patients experienced hypoxemia for at least five consecutive minutes.

- Given that approximately 234 million surgical procedures are performed annually worldwide, our report suggests that at least three million patients each year experience prolonged (≥ five minutes) and potentially preventable hypoxemia during surgery.

- Anesthesia providers strive to avoid hypoxemia because of the risk of irreversible damage to the myocardium, brain, and other end organs. Despite these efforts, hypoxemia continues to occur in the operating room at a surprisingly high rate.

More accurate solutions would lead to better patient outcomes and avoiding unnecessary costs associated with bad patient outcomes or stopping a procedure where there was no issue. While some of the problem related to the current incidence of hypoxemia is due to a lack of adoption of oximeters in the developing world, it’s not the entire story.

With pulse oximeters, clinicians largely must use data outputs to infer deoxygenation risk. Without getting too technical, compared to tissue oximeters, pulse oximeters have less “detectors” and don’t take into consideration all the factors that could impact oxygenation levels. For example, pulse oximeters readings are based on arterial blood flow, while tissue oximeters examine arterial and venous blood flow. (Arteries carry blood “away” from the heart, veins carry blood “toward” the heart. Generally speaking, arterial vessels contain oxygenated blood, and venous vessels carry blood that is low in oxygen). Basically, CASM’s tissue oximeter is more reliable than pulse oximeters by monitoring both the supply and demand of oxygen in the hemoglobin and provides clinicians with much more data.

Cerebral oximetry differs from pulse oximetry in that tissue sampling represents primarily (70-75%) venous, and less (20-25%) arterial blood. Cerebral oximetric monitoring is also not dependent upon pulsatile flow. Regional estimates of cerebral oxygenation in the vulnerable watershed region of the frontal cerebral cortex provide a sensitive method of detecting changes in oxygen delivery due to the limited oxygen reserve of this area. Cerebral oximetric monitoring thus may serve as an “early warning” of decreased oxygen delivery to the rest of the brain and other major organs.

From the company’s 2017 10-K:

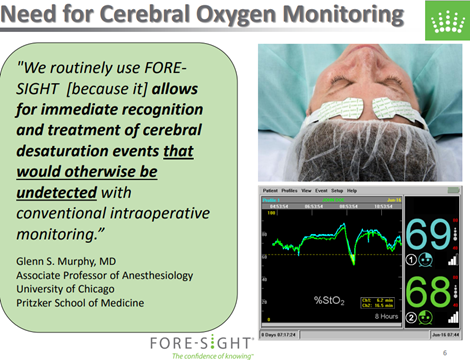

“We believe that our best-in-class FORE-SIGHT tissue oximetry products place CASMED in a unique position both to gain accounts from competitors and expand the clinical application for monitoring tissue oxygenation. Standard non-invasive parameters, such as pulse oximetry and blood pressure, provide only surrogate markers of tissue oxygen delivery. The indirect or systemic nature of these parameters forces clinicians to infer the adequacy of oxygenation in vital organs, including the brain, during medical procedures. However, data convincingly show that clinician inferences of cerebral oxygenation during medical procedures often do not correlate with actual tissue oxygenation levels. Therefore, potentially dangerously low levels of cerebral oxygenation often go unrecognized, correlating to high levels of patient harm. However, direct monitoring of cerebral oxygenation with FORE-SIGHT oximeters provides a unique and powerful tool that allows clinicians to recognize and treat potentially dangerous tissue hypoxia to avoid adverse clinical outcomes.”

Here is a 2012 article I came across that also talks about the importance of tissue oximetry and concludes that cerebral oximetry is superior than pulse oximetry.

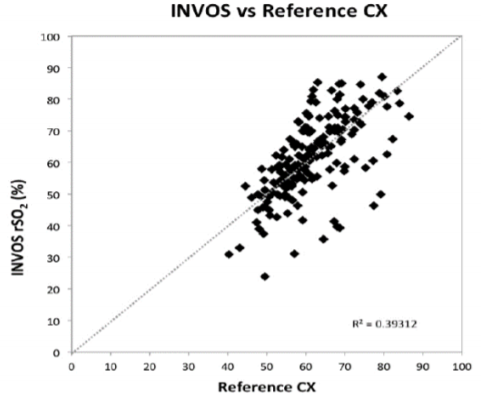

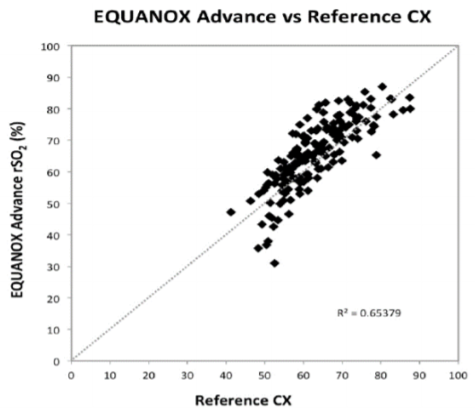

Not only does tissue oximetry have advantages over pulse oximetry, but FORE-SIGHT beats out its competitors in terms of accuracy and reliability of readings. This white paper by CASM is based on the “Bickler” study that compares 3 tissue oximeters:

- FORE-SIGHT

- INVOS

- NONIN EQUANOX1

The study concluded that:

“Performance among the tested monitors varied considerably. The FORE-SIGHT Oximeter demonstrated the greatest precision and accuracy.”

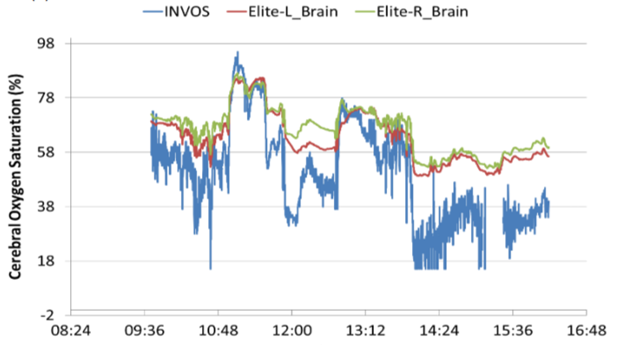

This CASM slide from its LD Micro presentation illustrates the FORE-SIGHT edge during a surgical procedure on a child. The blue is a competitor, which had extreme variability in its readings to levels indicating that child was suffering from desaturation events. However, FORE-SIGHT (red and green) indicated that this was not the case and that everything was normal. As it turned out the patient did not suffer any desaturation event and woke up fine.

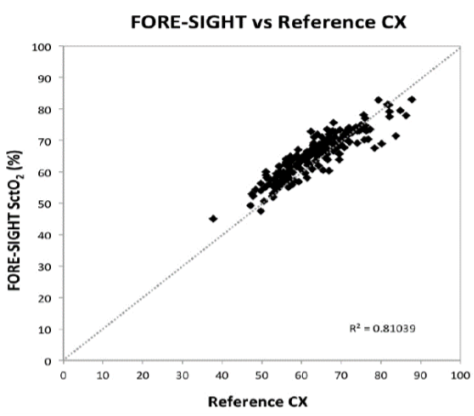

The following white paper image from slide #13 continues to illustrate the point that FORE-SIGHT is more accurate than the competition. The study compared three different tissue oximeters during several surgeries. The straight line represents the expected oxygenation levels that would be expected during various surgeries and the dots represent the readings from the oximeters. As you can see, FORE-SIGHT experienced the least deviation.

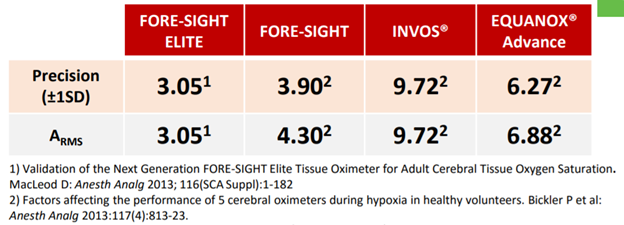

This slide image illustrates the same point by highlighting the average percent standard deviation from what would have been expected (the straight line). It also shows the improvement CASM made with its second generation, ELITE, product.

A very interesting competitive advantage that that Tom talked about was that the tissue oximeter of the market leader, INVOS, has severe issues when used on patients with darker pigmentation.

“In these patients, falsely low readings were found on relative oximetry (INVOS system), but were normal when measured by absolute cerebral oximetry (FORE-SIGHT). Because the accuracy in absolute oximetry is greater than that of relative oximetry in patients with darker skin, we now exclusively use absolute cerebral oximetry to guide us in ensuring adequate cerebral perfusion in darker skinned patients.”

These facts probably are likely a big reason why 50% of CASM’s growth in monitor sales is coming from stealing market share. The other 50% is coming from expanding the market.

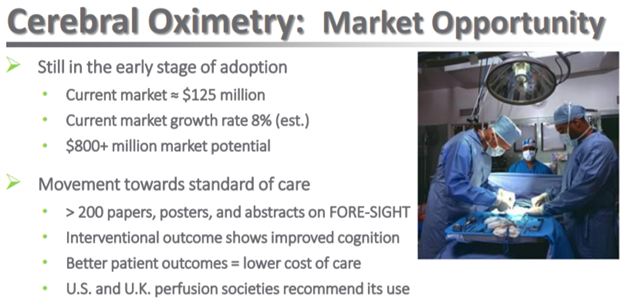

Market Opportunity

The immediate market potential for FORE-SIGHT is roughly $125 million with the total market opportunity nearing $1 billion, compared to CASM’s current revenue run-rate of about $21 million. The company believes it can grow by stealing market share from its competitors and by expanding market adoption. Below is a snapshot of the market environment:

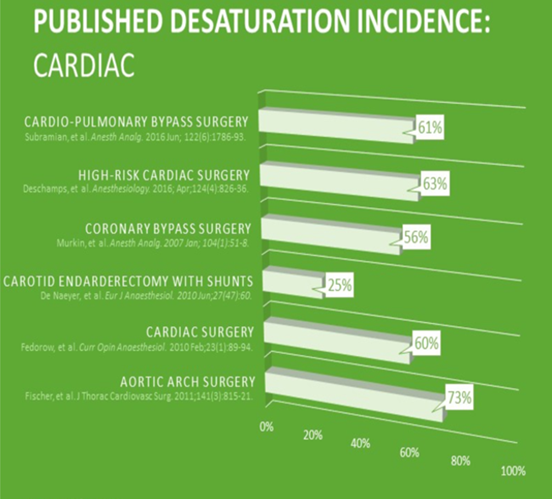

Of the $125M market estimate ($80 million in the U.S.), 80% is from cardiac surgical settings where deoxygenation risk is fairly high:

A $125 million near-term market potential may not sound like much, but CASM thinks it is only a matter of time before non-cardiac surgical settings will adopt tissue oximetry as a standard of care.

“Although the majority of published data have demonstrated improved outcomes among cardiac surgical patients, the studies performed thus far among non-cardiac surgical patients are beginning to identify its utility in other clinical scenarios. Future research to identify and validate the benefits of cerebral oximetry monitoring in improving patient outcomes among non-cardiac surgical patients (as well as cardiac surgical patients) represents an exciting and important opportunity to explore and utilize this recent technology.”

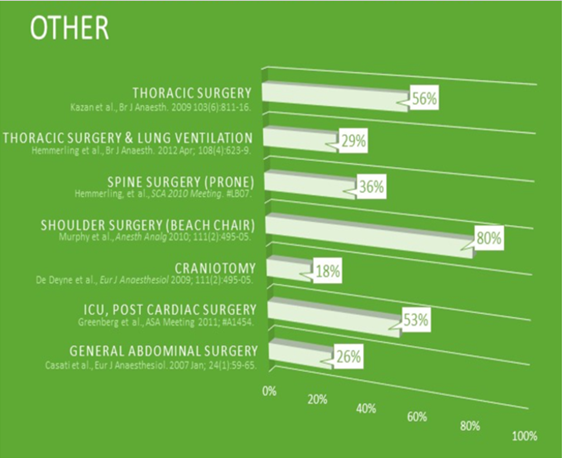

The following slide illustrates that deoxygenation risk is real and alive in an entire host of settings:

Another area of market expansion includes the use of tissue oximeters in post surgical settings (ICU). Tissue oximeters are mainly used in surgical settings, but as more data becomes available it is becoming apparent that a meaningful amount of hypoxic events occur post-surgery.

As far as CASM goes, with an estimated 20% market share, it’s in a great position to grow by

- stealing market share from the leader, Invos, which owns 70% of the market.

- expanding the market beyond cardiac

- increasing hospital penetration. CASM is in about 350 to 400 hospitals in the U.S. that have cardiac programs, compared to a total of 1500 to 1800.

- increasing penetration into cardiac pediatric surgeries which represent less than 10% of its sales, yet they are about one third of cardiac surgeries in the U.S.

- penetrating international sales that currently only represent about of 15% of its sales.

Upside Catalyst

As it stands on its own, CASM’s future looks bright. However, there's still more upside to the story. The company has created an “OEM module” which can be used with third party monitors. This is where CASM could get exciting - it’s a step in the door to get into a hospital, without having to pitch their monitors and the sensors and still allow customers to reap the benefits that FORE-SIGHT delivers. This will also allow the company to partner with larger sales organizations to get CASM solution into hospitals. The company has received FDA approval for one aspect of the product and needs to get one more approval before it can start marketing the product, which the company is targeting to occur in Q1 2019.

We think this is an incredible event that – if it becomes real, maybe by the end of the year - could really accelerate growth and a liquidation event through the sale of the company to a larger player.

Caveats

- FDA Recall

- Misses target on becoming cash flow positive

- Does not receive FDA approval for OEM Module

- Hits the wall on gaining market share

- Better technology arrives

- Stock dips since has had huge run

Valuation

As we stated, this is a longer-term play for us. Investors should note that the stock reacted strongly to Q1 2018 results. Shares have risen ~60% since the May 8, 2018 Q1 release and ~160% since it reported strong preliminary Q4 2017 results in early January (full year release here). A pullback from current levels of around $2.00 is certainly possible, and we hope it occurs.

CASM is stealing market share from inferior competitors and expanding the market, where there are only 4 serious players in the market.

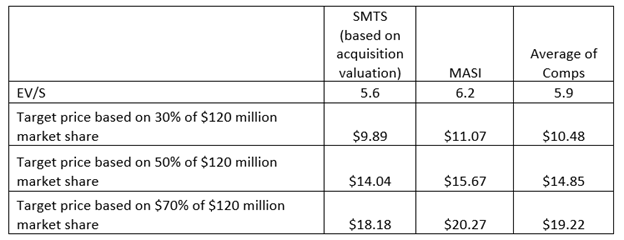

- Invos (Used to be public under the symbol SMTS. Later acquired by Covidien which was later acquired by Medtronic (NYSE:MDT)) – 70% market share

- CASM – 20% market share

- MASI , Nonin (private) – 10% combined market share

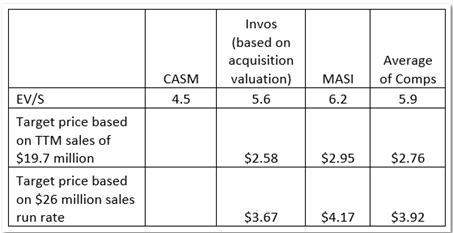

CASM is currently not profitable. Because of this, we need to look at enterprise value to sales (EV/S) as a valuation measure. If we look at CASM’s valuation based on a variety of EV/S assumptions, the stock appears undervalued. Here is a look at some valuation scenarios that use trailing twelve-month revenues and the run-rate based on where we with think quarterly revenues ($6.5 million) will be about a year from now.

Some investors will point to CASM’s $10.0 million in debt and debt to equity ratio of 5 as a negative. Normally, I might agree, but with Tom at the wheel and CASM’s recurring revenue model, I am willing to make an exception, especially when I am betting that profitability is around the corner. This should put the company in a position to start paying down its debt. It is also worth noting that Tom has had to deal with heavy debt burdens in some of his past turnarounds.

Ultimately, we think this story will end in an exit with the right company paying up for CASM. In 2010 Covidien (Old symbol COV) bought the market leader, Somanetics (Invos product, old symbol SMTS). Then in 2015, MDT bought Covidien.

Keep in mind that we did not assume any revenue contribution assumption from a possible final FDA marketing approval on CASM OEM module and any sequential growth from our $6.5 million revenue assumption, that we consider to be overly conservative. Thus, we think upside exists to our targets.

Here is a look at long-term valuation scenarios at different market share assumptions, only using $120 million as the base (so not even assuming expansion of the market):