Introduction to Semler Scientific

Semler Scientific, Inc. (SMLR) (~$8.30; ~$50M market cap) aims to provide technology and software solutions to improve the clinical effectiveness and efficiency of healthcare providers. The company currently derives its revenue from selling its Quantaflo product to aid in the diagnosis of Vascular Disease and operating an online platform called WellChec that provides insurance companies with data analytics services.

We are intrigued by the progress the company has made since going live in 2011, its underserved market opportunity, and its recurring revenue model. This is one case where a new technology is replacing an inefficient “old school” solution.

We urge you to read the caveats at the end of this article. Specifically, we are still digging into the marketing material of one of SMLR’s competitors which talks about reasons that its product is superior to SMLR’s.

Putting this caveat aside for the time being, we feel SMLR may have reached a growth inflection point.

Reasons for Tracking

1. Steadily Improving Financials

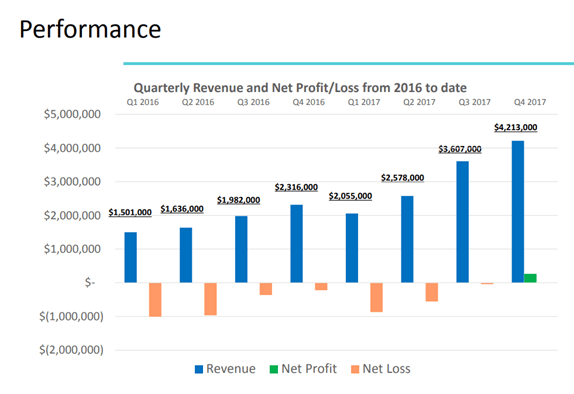

In late February 2018, the Company reported strong Q4 2017 results which marked the Company’s first profitable quarter.

- Sales were $4.2 million vs $2.3 million in the prior year period

- Non-GAAP EPS of $0.09 vs a loss of $0.01 in the prior year

- Gross margins of ~80%

Management offered bullish commentary for fiscal 2018:

“We expect revenues to continue to grow due to an increasing number of QuantaFlo™ installations resulting from new orders, higher average pricing as compared to its predecessor product and the recurring revenue business model that we employ. We expect to see continued annual revenue growth and continued profitability in 2018. We believe expenses will continue to increase as the business expands. However, it is our intent to continue to grow revenues at a faster rate than expenses and to remain profitable.”

The Q4 performance was the culmination of strong trends occurring over the past 8 quarters (per SMLR’s March 2018 Investor Presentation):

2. Addressable Market

The Quantaflo product, which is the Company’s main revenue generating product, is addressing a huge market. It tests for Peripheral Artery Disease (PAD), a type of vascular disease which nearly 20 million Americans suffer from. People who have PAD have a 21% increased risk of a heart attack, stroke, hospitalization or even death within one year. Management stated that the target market is over 65 million people, including anyone over 65 and those over 50 who have one risk factor for PAD. They also noted that a good deal of this market goes undiagnosed under the main alternative testing methods.

3. Superior Product

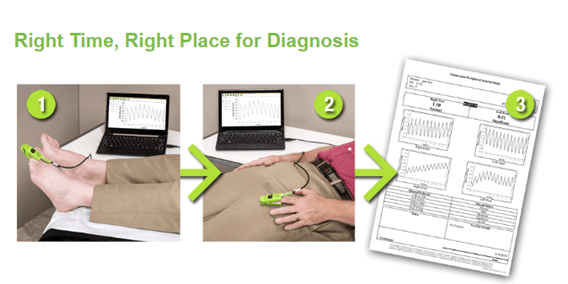

Management claims that its Quantaflo product, launched in 2011, is a more convenient and effective way to monitor blood flow obstructions to aid in the diagnosis of Vascular Disease than competing products.

The Quantaflo product simply clips on to your finger and toe and gives a reading within 5 minutes.

The test delivers faster, more accurate results (10% to 15% higher) than prior testing methods such as blood pressure cuffs and Doppler machines. For example, the Quantaflo test only takes 5 minutes to administer compared to 8 to 30 minutes for other methods.

The product benefits patients and doctors by helping detect and address early warning signs of PAD and reduce the number of undiagnosed cases, mortality and amputations of the leg.

WellChec houses data from various entities that perform PAD tests. In April 2015, it launched the WellChec multi-test service platform, to more comprehensively evaluate customers’ patients for chronic disease. WellChec remains a service platform which can be used to help risk assessment groups and home healthcare providers choose the right health care plan.

4. Expands Market Reach (Clinics)

SMLR’s solution is not only a preventive healthcare one which can help offset costs, but will generate additional revenue, due to an increase in PAD diagnosis, for those practitioners who switch to the Quantaflo. These patients will need to keep getting tested as part of a maintenance program.

Another added benefit to the primary care physician is that the test can be administered by a nurse or nurse’s aide. This is a big deal. Prior to Quantaflo, only specialized licensed technicians were allowed to administer the industry standard tests. Quantaflo expands the market of those that can administer Quantaflo to 350,000 primary care physicians compared to about 20,000 specialized technicians. Quantaflo becomes a revenue hub for primary care doctors, while it allows more at risk people to gain access to a test that 20,000 technicians just can’t support. The test can also easily be administered at home, opening the door to the growing home healthcare risk assessment industry.

There is also an opportunity to get health insurance companies on board to cover Quantaflo. Sure, insurance companies are looking for preventive health measures to help offset medical costs, but insurance companies will be able to receive more money from the government to treat PAD because Quantaflo will significantly increase the number of patients being diagnosed with PAD (the amount of money to potentially be received from the government goes up with increased diagnoses of disease).

An excerpt from SMLR’s 10-K on Quantoflow:

“We have placed our QuantaFlo™ product with healthcare insurance plans, integrated delivery networks, independent physician groups and companies contracting with the healthcare industry such as risk assessment groups, in addition to doctors’ offices. Our WellChec™ service platform is generally targeted to companies that contract with health insurance plans and other healthcare organizations, such as risk assessment groups and other home healthcare providers.”

In a nutshell, the revenue opportunity has expanded due to:

- More accurate diagnoses

- Ability to test more people by getting the test in hand of more doctors (and nurse’s aids) that can administer the test

- Insurance companies incentivized to cover more PAD patients

5. Recurring Revenue

An exciting part of the story is SMLR’s recurring revenue model. The company generates revenues from monthly software license fees and/or a per test fee. The company has developed a license model rather than an outright sales model for Quantaflo. Below is verbiage from the 10-K discussing the recurring revenue model:

“This license model eliminates the need to make a capital equipment sale. Consequently, we generally require no down payment or long-term commitment from our customers. QuantaFlo™ has an expected average lifetime of at least three years. We intend to reevaluate the monthly price periodically in consideration of the revenue generation associated with QuantaFlo™. To date, we roughly estimate that routine office usage of the QuantaFlo™ has ranged from a few tests per week up to 10 tests per day. We also offer contracts in which we invoice on a per test basis for use of QuantaFlo™.”

Basically, the idea is to give the product away to get it in the hands of its potential customers and then, let it pay for itself.

In addition to the licensing model, the company has contracts with a fee per test model, in which an invoice is generated on a per use basis.

For 2017, roughly 78% of sales came from the license model with the remainder coming from the fee per test model.

6. Marketing Approach

The company uses its own salesforce, as well as a co-exclusive distributor agreement with Bard Peripheral Vascular Inc., which is a large medical device company with a worldwide presence. The Bard partnership accounted for roughly 20% of revenues in 2017.

The company believes there will be some cross-selling ability within the insurance company dynamic, as the test can detect early warning signs that would lead to cardiovascular disease for people at risk of developing PAD including:

- Smokers

- Those with diabetes

- Those with high blood pressure

- Those with high cholesterol

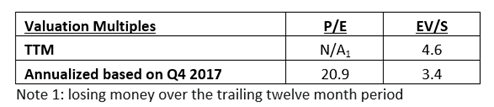

Valuation

At first glance, the stock seems to be overvalued or – at least - fairly valued. Here are the stats on the company’s trailing and Q4 runrate:

However, given the company’s expected growth trend and high gross margins (80%), the stock could wind up being undervalued rather quickly. The company has operating leverage, where it expects earnings to outpace revenue growth. The company also expects expenses as a percent of revenue to decline moving forward. It seems that the company has no intentions to raise additional capital in the near future and believes it will be able to satisfy debt repayments and other liabilities from cash flow from operations.

Assuming the company maintains its current growth trends, it would be on pace to nearly double revenues in 2018. SMLR is already sitting at 12% pre-tax margins, so we see a tremendous amount of potential for margin expansion.

Assuming $20 million in revenues for 2018 (assumes 60% growth) and using 15% net margins, EPS would equate to roughly $0.45. As far as valuation, if it becomes evident their growth plan is sticking, we could see SMLR trading at 30x this EPS, or $13.50.

Caveats

- Changes/regulation in insurance environment

- Margins expand at less than we expect

- Hard to forecast number of tests that will be administered

- The company was delisted from NASDAQ in August 2016 due to failure to regain compliance with the required $2.5 million stockholder equity rule

- We noticed that a competitor of SMLR (Newman Medical) published its reasons why it believes its device, simpleABI, is superior to Quantaflo.

- Newman also states the Quantaflo is not permitted to be covered by Medicare. You can see the page here. We are digging into Newman Medical’s claims.