By Maj Soueidan, Co-founder GeoInvesting

Eastern Company (The) (NASDAQ:EML) is firmly on our plate because we believe the company is on the brink of freshening up its product offerings and announcing an accretive acquisition. Our research has uncovered small doses of InfoArbitrage which include a development that has significantly improved (and will continue to) the balance sheet and EPS profile over the next several years. We currently do now own shares of EML, but will let you know if we do begin to establish a position. EML manufactures and sells industrial hardware, security products, and metal products in the United States and internationally.

Buying shares of stock in boring yet established companies that have been around for years on the verge of reinventing their operations is one of our favorite things to do. Peter Lynch was big fan of this tactic:

- The name is boring, the product or service is in a boring area, the company does something disagreeable or depressing, or there are rumors of something bad about the company--Lynch likes these kinds of firms because their ugly duckling nature tends to be reflected in the share price, so good bargains often turn up.

- The fast-growing company is in a no-growth industry--Growth industries attract too much interest from investors (leading to high prices) and competitors.

Here are a few ways the GeoTeam explores this angle.

Tracking Companies That Restructure And Emerge From Chapter 11 Bankruptcy

Companies that emerge from Chapter 11 bankruptcy often do so with less debt and better product/market focus. Buying the right target company can lead to enviable portfolio gains.

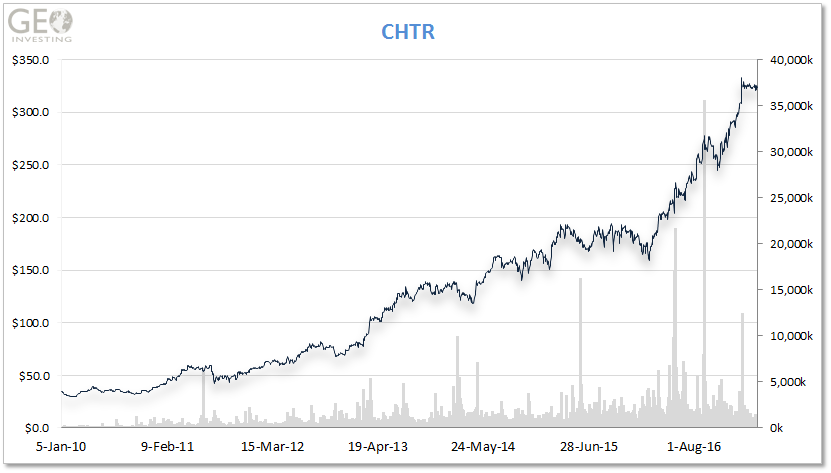

For example, on March 15, 2010 we bought and coded Charter Communications, Inc. (NASDAQ:CHTR) as a GeoSpecial at $33.00. The company had recently emerged from Chapter 11 bankruptcy. About a year later, we disclosed that we exited our position around $60, but that longer term the stock could reach $145. Currently, the stock is sitting at $327. CHTR is a multi-billion dollar top 5 cable operator in the U.S.

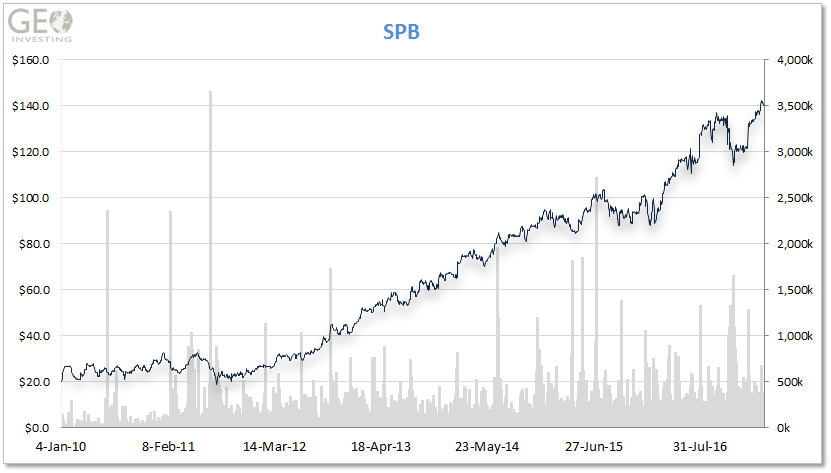

Spectrum Brands Holdings, Inc. (NYSE:SPB) is another Chapter 11 exit example. We coded this stock as a GeoSpecial on March 2, 2010 and closed out the position in August 2012 at $36. The stock is now trading near its all-time high of $143.20. SPB is a multi-billion-dollar leading supplier of batteries, shaving and grooming products, personal care products, specialty pet supplies, lawn & garden and home pest control products, personal insect repellents and portable lighting.

Reinventing Product Lines

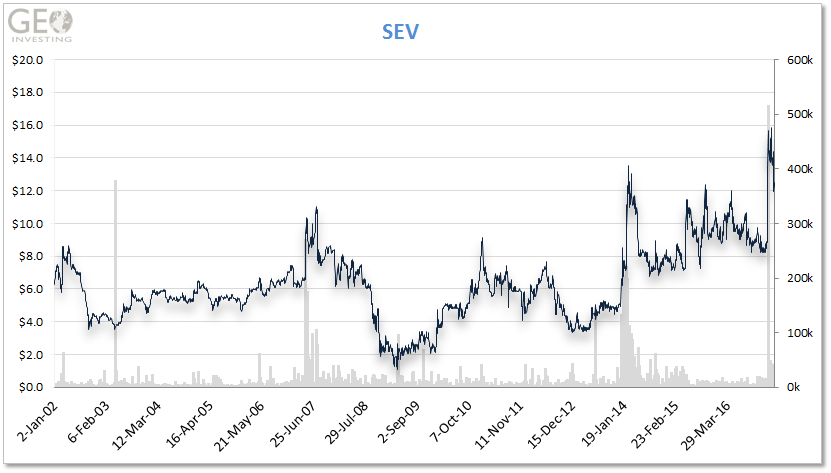

A recent example of a stock that falls into this category is Aptera Motors Corp. (NASDAQ:SEV), a 30 year old designer and seller of motor controllers with 276 employees and a current annual revenue run rate of about $40 million. The company has been struggling to profitably grow its business for several years.

This underperformance attracted activists to push for changes on the Board of Directors and called on management to find new areas of growth for its legacy product offerings/technology. SEV is currently losing money, but earlier this year shares briefly doubled to $17.54 in two days, after the company issued a press release discussing contract wins related to some of its product reinvention activities in the electric vehicle industry that are expected to impact revenue in 2018.

SEV is an example of investors looking past valuations when they are outstretched, due to an expectation that new revenue growth will be significant and will come with higher margins.

Acquisitions to Gain Market Share

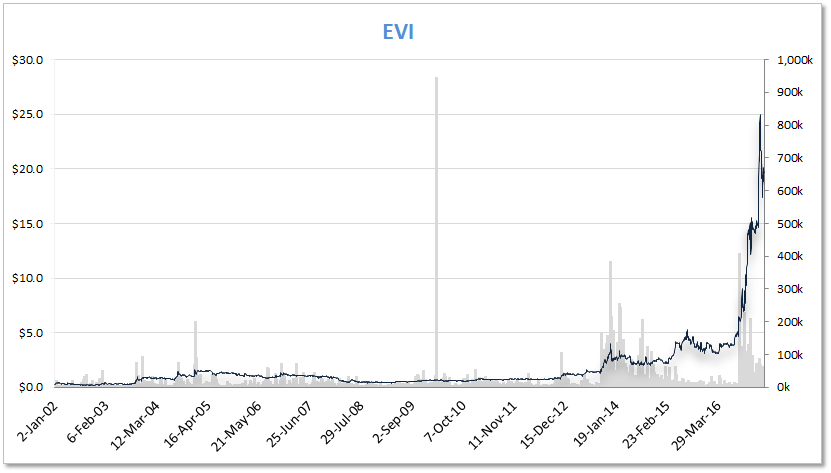

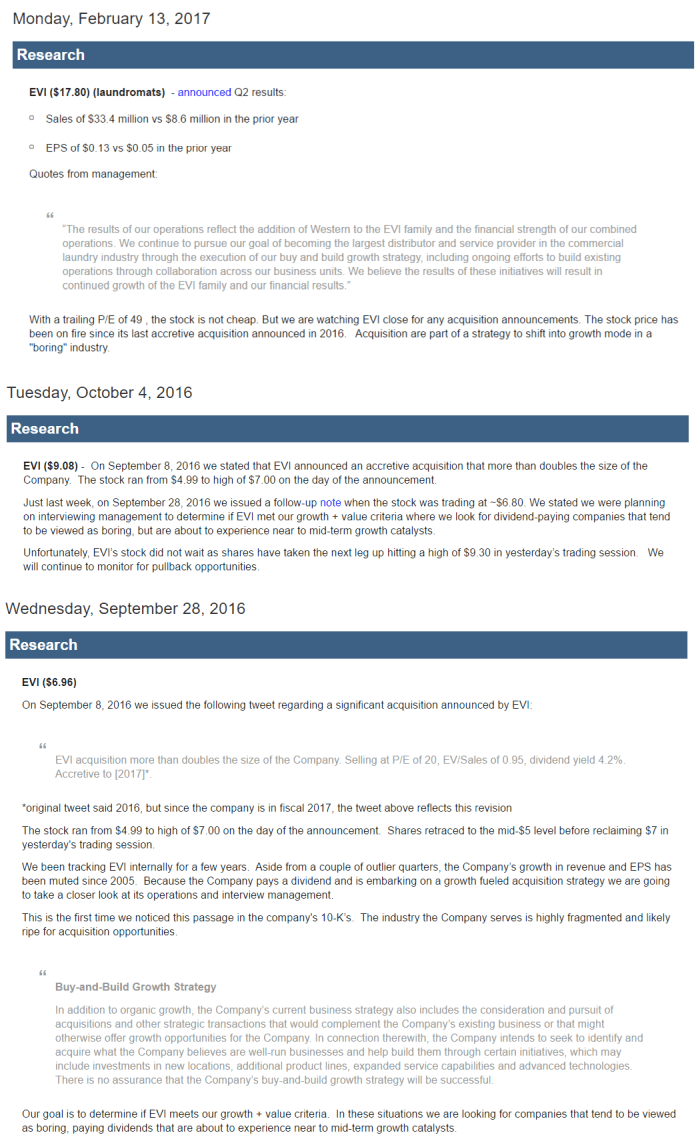

We think you would agree that Evi Industries, Inc. (NYSE:EVI) business of owning coin operated laundry facilities is as boring as it gets. EVI dates back to 1960 and went public through a reverse merger on November 1st 1998 under the name DryClean U.S.A. Revenues were around the $30 million mark between 2013 and 2016 and ~$20 million in 2012, basically equal to the revenue levels reached in 2000.

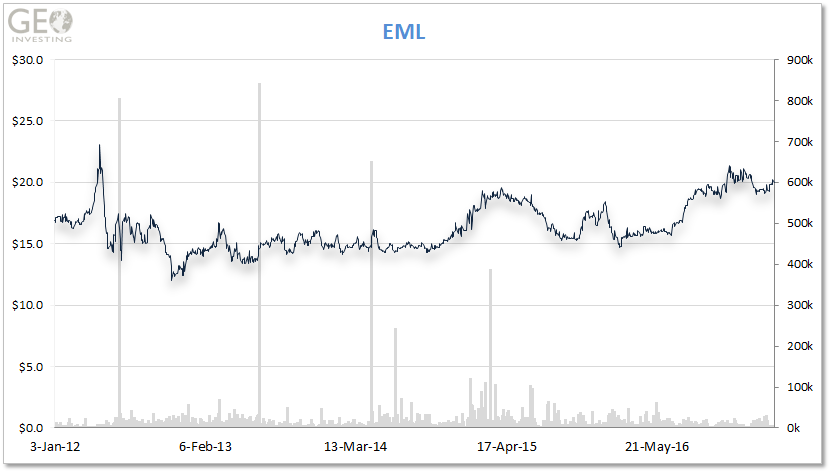

The long-term stock chart is just as boring:

Until the fall of 2016, when the company nearly tripled the size of its business through an acquisition of Western State Design on September 8, 2016.

EVI press releases and SEC quarterly filings have typically not provided commentary beyond the numbers. However, alert microcap investors who read SEC filings got glimpses of a potential growth inflection point (the company’s acquisition strategy). EVI’s 2016 10-K (year ended June) stated that management adopted an acquisition strategy to improve its growth profile:

“Buy-and-Build Growth Strategy

In addition to organic growth, the Company’s current business strategy also includes the consideration and pursuit of acquisitions and other strategic transactions that would complement the Company’s existing business or that might otherwise offer growth opportunities for the Company. In connection therewith, the Company intends to seek to identify and acquire what the Company believes are well-run businesses and help build them through certain initiatives, which may include investments in new locations, additional product lines, expanded service capabilities and advanced technologies. There is no assurance that the Company’s buy-and-build growth strategy will be successful.”

This was the first time that we noticed this type of commentary popping up in filings: clues, clues, clues!

We issued our first note to members when the stock was sitting at $6.96. Below is our research journal, which can also be found here.

Unfortunately, the stock got away from us during our due diligence, rendering us spectators of the stock’s quick rise.

The Eastern Company Is Next On The Docket

EML has three divisions:

The Industrial Hardware segment designs, manufactures and markets a diverse product line of industrial and vehicular hardware throughout North America. The segment’s locks, latches, hinges, handles, lightweight composite structures and related hardware can be found on tractor-trailer trucks, moving vans, off-road construction, farming equipment, school buses, military vehicles, recreational boats, pickup trucks, sport utility vehicles and fire and rescue vehicles, metal cabinets, machinery housings and electronic instruments. This unit also include a plastic injection molding operations.

The Security Products segment is a leading manufacturer of security products. This segment manufactures electronic and mechanical locking devices, both keyed and keyless, for the computer, electronics, vending and gaming industries, luggage, furniture, laboratory equipment and commercial laundry industries. Greenwald manufactures and markets coin acceptors and other coin security products used primarily in the commercial laundry markets, as well as hardware and accessories for the appliance industry. In addition, the segment provides a new level of security for the commercial laundry industry through the use of “smart card” technology. Argo EMS supplies printed circuit boards and other electronic assemblies to Original Equipment Manufacturers (“OEM”) in industries such as measurement systems, semiconductor equipment manufacturing, and industrial controls, medical and military markets. Greenwald’s products include timers, drop meters, coin chutes, money boxes, meter cases, smart cards, value transfer stations, smart card readers, card management software, access control units, oven door latches, oven door switches and smoke eliminators. Illinois Lock Company/CCL Security Products sales include cabinet locks, cam locks, electric switch locks, tubular key locks and combination padlocks. Many of the products are sold under the names, SESAMEE®, PRESTOLOCK® and SEARCHALERT™.

The Metal Products segment is the largest and most efficient producer of expansion shells for use in supporting the roofs of underground mines. This segment also manufactures specialty malleable and ductile iron castings. Typical products include mine roof support anchors, couplers for railroad braking systems, support anchoring for construction and couplers/fittings for utility (oil, water and gas) industries. Mine roof support anchors are sold to bolt manufacturers while specialty castings are sold to original equipment manufacturers or machine houses.

It’s apparent that EML, no doubt, is a company with an impressive product line-up for the markets it serves. Unfortunately, EML’s share price performance has been just as boring over the past five years:

Our Reasons For Tracking EML Follow:

1. Established Business That Is Profitable

EML is a ~160 year old company. Revenue reached as high as $157.5 million in 2012 and averaged $139.9 million since 2006. Although the company has not grown its revenue for some time, we think it is somewhat encouraging that the company has remained solidly profitable since at least 1993 (SEC filing pages 71 and 72). Here is a snapshot of the company’s annual financial performance (revenue and EPS) since 2006.

|

2016

|

2015

|

2014

|

2013

|

2012

|

2011

|

2010

|

2009

|

2008

|

2007

|

2006

|

|

$137.7

|

$144.6

|

$140.8

|

$142.4

|

$157.5

|

$142.8

|

$130.1

|

$112.6

|

$135.9

|

$156.3

|

$138.5

|

|

$1.25

|

$0.92

|

$1.23

|

$1.11

|

$1.38

|

$0.89

|

$0.90

|

$0.17

|

$0.73

|

$1.68

|

$1.67

|

Part of the challenge to grow the business is that EML’s legacy target markets are experiencing their own growth challenges. EML’s new CEO (and activist) is beginning to pave a way to a new future:

“August Vlak, President and CEO added that “our businesses have executed well in the face of a significant and sustained downturn in the class 8 truck market and a secular decline in the mining industry by expanding into new markets and building a sustainable pipeline of new business opportunities for 2017 and beyond.”

2. Growth Value

As you become familiar with our research process, if you have not already, you will notice that we often look for stocks offering “growth value” propositions. See more about this here. The value part of the equation can arise from:

- Low valuation because a stock is being priced as a boring company with no perceived growth opportunities

- Companies paying dividends

- Not only can you get paid while waiting for a growth catalyst to materialize, but an increasing dividend yield that occurs when prices fall can establish support levels for a stock.

- Misunderstood pieces to company financial statements that, if made more clear, can lead to an expansion of valuation multiples.

Unlike, SEV and EVI, EML has an added benefit in that its valuation is not outstretched. EML currently pays an annual dividend of 44 cents, yielding 2.2%, while shares trade at a trailing twelve-month P/E of 15. EML has a paid a dividend for 77 consecutive years and given its strong free cash flow standing of about $9.0 million and current ratio of 6 to 1, we don’t see the dividend being in jeopardy.

We could see EML’s P/E expanding to 25 rather quickly if the growth part of the growth value equation undergoes a catalyst(s).

Potential valuation multiple catalysts EML management is hinting at include:

- New growth markets for legacy products

- New products

- Acquisitions

A change in dividend policy could also result in a “win/win” scenario where EML:

- Increases its dividend if growth prospects improve

- Suspends its dividend if reinvesting capital back into business makes more sense

3. Activists Keeping Management In Check

A 2016 Financial Times article talks about the significant increase in activist involvement in microcap stocks. Eight years of broad underperformance in growth value microcap stocks is partly responsible for this trend. Placing bets alongside the right activists can be a rewarding strategy. Activists can force management teams of underperforming companies to consider ways to maximize shareholder value. We believe the EML situation meets this threshold.

In fact, we briefly talked about EML on February 10th 2015. We noted that two activist investors had filed recent 13D’s discussing their dissatisfaction with EML’s reluctance to pursue growth initiatives. Here is a quote from activist investor Barrington Capital:

“the Reporting Persons have become aware of a reluctance on the part of the Issuer to engage in constructive conversations with potential business partners relating to strategic alternatives open to the Issuer. Issuer’s dismissive response to the recent 8-K filed by Synalloy is the latest example of such reluctance. Given the Issuer’s lack of meaningful growth and lack of any clear management succession plan, the Reporting Persons believe it is time to engage in an energetic review of strategic alternatives including hiring an investment banking firm to consider the sale of the issuer or substantial changes to the Issuer’s capital structure.”

One day later, $SYNL sent a letter to the CEO offering to buy the company for $21.00. We are glad EML rejected this offer, but what we are really excited about is that legendary investor Mario Gabelli owns a 16.6% of EML through several of his entities. Gabelli was one of the activists who lit a fire under SEV’s management. Gabelli pops up in many other small undervalued, boring microcap stocks that we follow.

4. Management Heeding Activist Warnings

We think management got the message, loud and clear, that they need to take action to improve the growth profile of the company. The company has taken the following investor friendly moves since 2015:

- Removed of an outdated poison pill agreement established in 2008 that we think could make the company a more attractive acquisition target.

Mr. Leonard F. Leganza, Chairman, President and CEO, stated, “The Company’s Board of Directors, after extensive discussions, has determined that the termination of the Rights Plan is in the best long-term interest of all of our current shareholders. It is also a positive step forward toward modifying our governance policies looking into the future.”

- Potentially making the Board of Directors more accountable for their performance

“On January 13, 2016, the Board of Directors of the Company approved amendments to the Certificate of Incorporation and the By-Laws of the Company which will eliminate the classification of the Board of Directors in a phased in manner and will provide for the election of directors by a majority of the votes cast at the Annual Meeting of Shareholders. ”

- Replaced the 85 year old Chairman and CEO with two members of Barington Capital Group (Activists) with extensive “Boardroom” and company turnaround experience.

“Mr. Mitarotonda, 61, is the Chairman, President and Chief Executive Officer of Barington Capital Group, L.P., an investment firm. He currently serves as a director of A. Schulman, Inc., OMNOVA Solutions Inc., The Pep Boys - Manny, Moe & Jack and Barington/Hilco Acquisition Corp. He is a former director of a number of publicly traded companies, including The Jones Group Inc., Griffon Corporation, Gerber Scientific, Inc., Register.com, Inc. and Ameron International Corporation.” Barington Capital is known for Mr. Motarotonda’s brash open letters to management, and an aggressive activist style. Many of the companies he has been involved were consequentially acquired.

“Mr. Vlak, 49, has been a management consultant and, most recently, a Senior Advisor to Barington Capital Group, L.P. He was previously a Partner at Katzenbach Partners, a Senior Advisor at Booz & Company, a consultant at McKinsey & Company and an investment banker at Lehman Brothers, and has worked in Cleveland, New York, Hong Kong and London. Mr. Vlak’s consulting work focused on growth strategy and operational performance improvement at more than 50 companies − including leading domestic and global industrial enterprises − where he has worked directly with numerous senior management teams and boards of directors.”

- Added commentary in press releases and SEC filings (InfoArbitrage) that the company is actively pursuing an organic and acquisition growth strategy.

- Information arbitrage only present in its 2016 10-K filed on March 15th 2017 stating that EML:

“continues to develop new customers in the industrial casting business and is close to producing several new products for the gas, water and energy industry.”

5. Freezing the Pension Plan

On May 16, 2016, management announced that it was freezing its pension plan. Basically, the company will be phasing out its pension by paying out its remaining pension obligation over the next several years. While EML will still have to pay out benefits through 2026, the amount it is on the hook for is fixed. Estimated future benefit payments to participants of the Company’s pension plans are:

- $3.8 million in 2017

- $4.0 million in 2018

- $4.2 million in 2019

- $4.5 million in 2020

- $4.7 million in 2021

- $26.2 million from 2022 through 2026.

Since pension benefits will not accrue past the “frozen” amount, this move is accretive to EPS and will strengthen the balance sheet with each incremental year as the liability makes its way off the books. The remainder of the balance sheet is in good shape with almost $3.70 per share in cash. Of the overall $110m in tangible assets, less than 2m is interest bearing debt. The remainder is working capital related liabilities, so the company has only the pension as a meaningful liability on its balance sheet.

‘In addition, our decision to freeze our pension plan effective May 31, 2016 not only strengthens our balance sheet but also contributed $0.11 and $0.17 per diluted share in the third quarter and the nine-month period ending October 1, 2016.”

In addition to being good for the company’s financials, we think freezing the pension puts EML in a better situation to be an acquisition target.

We also think that when combined with everything going on to jump start growth, that EML will eventually experience a significant expansion in its valuation multiples.

Investors who want to place a bet in EML probably need to do so ahead of a positive tangible announcement on the company’s progress. The stock has 6.2 million outstanding shares and a float of only 5.5 million.

Caveats

- There are certainly risks to the story. There is no guarantee that the company will be able to find the right acquisitions or develop new products that will be adopted by its existing and/or new customers.

- The company has been talking about exploring growth opportunities for over a year, with still nothing to really show for it.

- Quarterly financial disappointments are a risk until the company completes an acquisition or introduces new products into growth markets.

We want to interview the company to get a better handle on how it plans to attack new growth opportunities. Regardless, it is hard not to get excited about the path EML is on, since it is a path other microcap companies in similar situations have successfully taken to maximize shareholder value.