Business

Innovative Food Holdings is a fast growing provider of specialty food products. The company is structured as a holding company. Its largest subsidiary is Food Innovations Inc, whose business is to provide specialty food products within 24-72 hours to customers which includes restaurant, hotels, country clubs, national chain accounts, casinos, hospitals, and catering houses. Gourmet Food Service Group is another subsidiary whose business is to provide customers with gourmet food products shipped directly from their network of vendors within 24-72 hours. The last major subsidiary is Artisan who is a supplier of over 1500 niche gourmet products to over 500 customers such as chefs, restaurants, etc. in the Greater Chicago area and also serve as a fulfillment center for the company’s other subsidiaries.

Industry

According to the Specialty Food Association, specialty food sales hit $120.5 billion in 2015, and are expected to grow at double digits for the next few years which is more than every other type of food sales category. Foodservice grew 27% vs 19% for retail because more people are dining out and seeking high quality food. 58 out of 61 specialty food categories experienced double digit growth. 60% of distributors grew sales more than 10% and none experienced sales declines. You don’t have to read this report to know that this industry is growing. Most people have heard a lot about the increased awareness of health and food sourcing. I believe the trend toward healthy eating is a long-term trend that is largely responsible for the growth in the specialty food industry. The food distribution industry itself is very fragmented with the largest player, Sysco, accounting for about 10-12% of the industry based on my estimates and the second largest player US Foods accounting for 8%, based on their 10-K. The fragmented nature of the industry means acquisitions is a way for large players to grow, making IVFH a potential acquisition candidate.

Competitive Advantage and Business Model

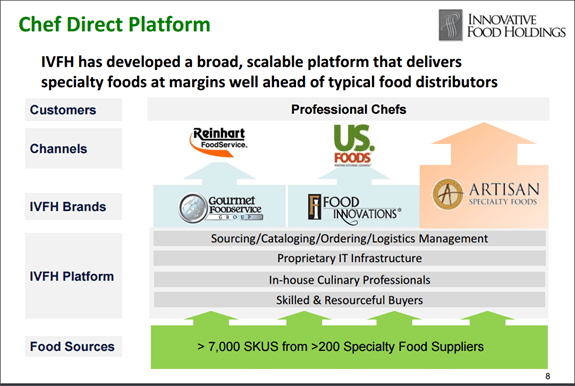

This is a fragmented industry so there are probably hundreds of competitors, but Innovative Food Holdings is differentiated by their broad range of specialty products (over 7000) and ability to deliver from the source in 24-72 hours. Below is from a page of their investor presentation. The way their platform is set up is itself a competitive advantage. Over 80% of the 7000 SKUs are delivered straight from the source. This is similar to drop shipping for those who are into ecommerce.

Most restaurants regularly order from multiple suppliers which can be a logistical nightmare at times, but with IVFH’s platform, they can just call IVFH and IVFH will coordinate with their suppliers and have it delivered straight to their customer. In case you’re wondering why customers just don’t go straight to the source and cut out IVFH, the logistics and coordination is the biggest reason. Innovative Food holdings carefully select suppliers based upon, among other factors, their quality, uniqueness, reliability and access to overnight courier services. This way, IVFH does not have to warehouse. Compared to a broad line distributor like Sysco or US Foods whose businesses are more suitable for delivering standardized food products, they are not ideally suited to carry small batches of niche products from small suppliers. The problem with most other distributors such as local or regional is that they just don’t carry such a broad range of high end premium product that IVFH has to offer, and if they do they can’t get it delivered on time.

In fact, IVFH is in such a strong competitive position that US Foods signed an exclusive distribution agreement to have IVFH distribute over 3000 specialty food to their customers. Currently US Foods accounts for over 70% of IVFH’s revenue. Some people see this as a risk but I see it as a testament to how effective IVFH’s model is. IVFH is a small company so they lack a large marketing and sales team, but their partnership with US Foods is a perfect complement to what they are lacking and probably a lot cheaper than hiring a large marketing team.

IVFH has been able to successfully diversify from US Foods from over 97% of revenue in fiscal 2008 to just over 70% in 2015.

The Fresh Diet Debacle

One of IVFH’s growth strategy is acquisitions. The Artisan group was acquired for 4.2x EBITDA in 2012. It was a successful acquisition which gave IVFH a part of the Chicago market. In August 2014, IVFH announced they were going to acquire The Fresh Diet, a B2C food company that is like Blue Apron. They bought the company for 0.6 sales and thought it was a good deal. After a year, they realized the Fresh Diet was a money sucking machine and had difficulty getting synergies out of it so they knew they had to get rid of it.

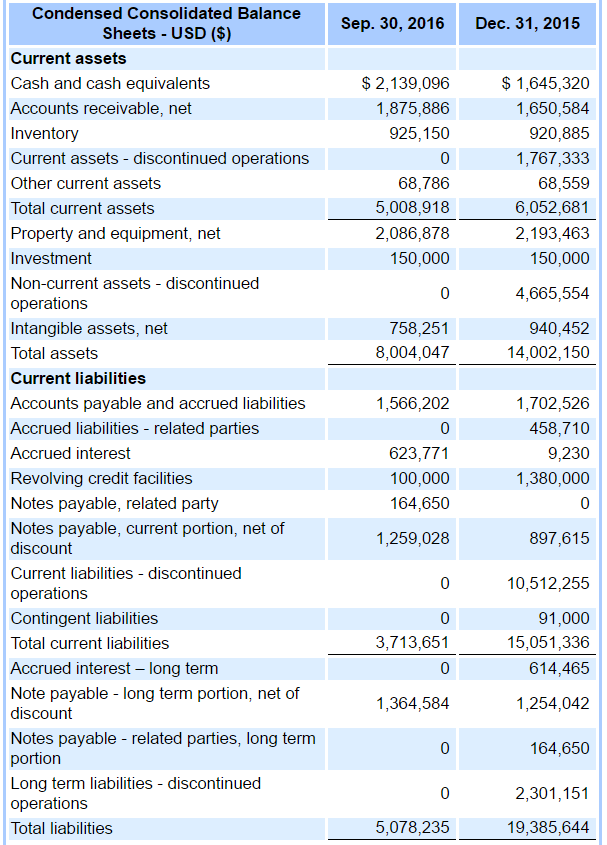

IVFH tried to spinoff the company, but that didn’t work so they sold it in exchange for debt restructuring and they got to keep 10% of the Fresh Diet. I was hoping IVFH would at least get a better deal than what they got, but at least they were able to get rid of The Fresh Diet from their balance sheet and it looks a whole lot better than before. The balance sheet literally went from bad to good overnight.

As a result of the restructuring, its current ratio went from 0.4 to 1.37 and long term debt decreased from 4.5 million to 1.3 million.

Financial Statements

(In millions)

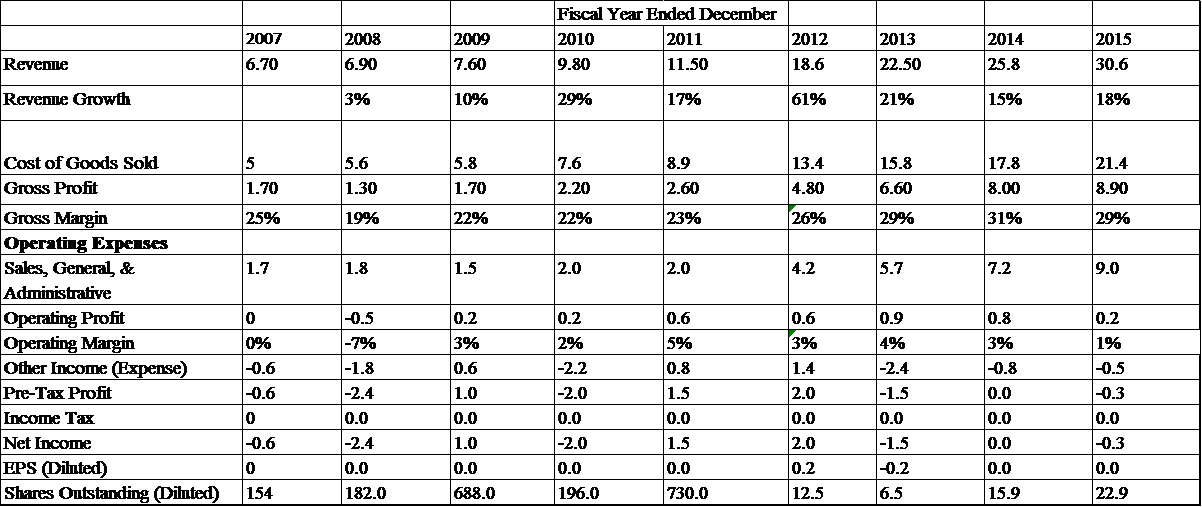

It’s interesting to note that the company actually managed to grow revenue by 3% in 2008 despite being in the worst recession since the great depression. It should be noted that adjustments were made to exclude Fresh Diet. The crazy share counts before 2011 were before the reverse stock split.

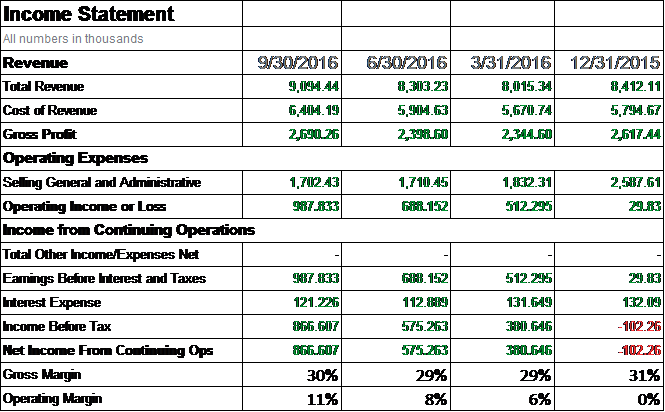

The company has managed to successfully grow revenue organically (Artisan acquisition took place in 2012) at a double digit rate for the past 8 years and I expect this trend to continue, albeit at a lower rate. I believe 10% is an achievable and conservative growth rate. The company has also manageded to maintain a high gross margin compared to its historical average as can be seen in the last 3 quarters after the spin off of Fresh Diet. There is significant operating leverage in the business as can again be seen in the last 3 quarters. A 12% change in revenue can lead to a 200% change in net income and given that management has stated that they can grow revenue without much increase in operating expense, there will be continual improvements in operating margins. If we assume that Q4 of 2016 will be the same as Q3 which is very conservative, the company will be trading for less than 7x PE. There is also 6.6 million in operating loss carryforward in the last 10-K, so the company shouldn’t have to pay any tax for the next 2 years. For a growing company, the valuation is way too low and there is at least a 50% upside from here.

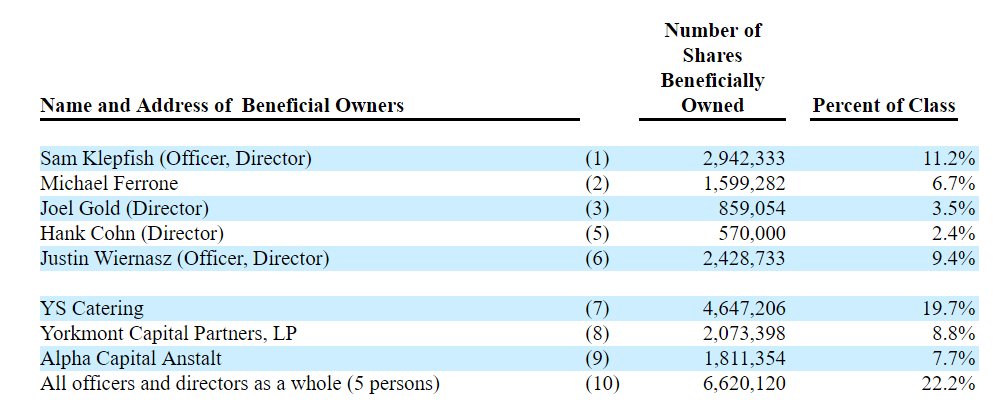

Inside Ownership

Looking at insider ownership, we can see that officers and directors own about a quarter of the company and institutions own more than 35%. It should be noted that Sam Klepfish, the CEO, got more than half of his stocks from restricted stock unit awards. Yorkmont Capital is quite well known in the microcap community so it’s good to see that they are holding a sizable stake in IVFH. I did found some interesting information about RSU when reading the footnotes:

“An additional 125,000 RSUs will vest contingent upon the attainment of a stock price of $2.00 per share for 20 straight trading days, and an additional 175,000 RSUs will vest contingent upon the attainment of a stock price of $3.00 per share for 20 straight trading days. The Company estimated that the stock-price goals of the Company’s stock price closing above $2.00 per share for 20 straight days have a 90% likelihood of achievement, and these RSUs were valued at 90% of their face value; the Company also estimated that the likelihood of the Company’s stock closing above $3.00 per share for 20 straight days is 70%, and these RSUs were valued at 70% of their face value. We recognized stock-based compensation expense of in a straight-line manner over the vesting period of the RSUs.”

I don’t often see companies claiming that their stocks are going to be 4 or even 6 baggers like this so I’m not going to take these statements too seriously at this point.

Conclusion

IVFH is a company growing at double digits in a trendy segment of the specialty food distribution industry with a strong competitive advantage and high operating leverage. It is trading at a very low multiple and with the upcoming earnings release, news sites like Yahoo Finance will finally show a positive TTM net income and PE which will attract investors and drive the stock up.

DISCLAIMER: GeoInvesting has no affiliation with the author of this report in any way and is not endorsing his research, nor has GeoInvesting vetted this information in any way. The GeoTeam does not attest to the accuracy of the information contained in this report and always urges investors to conduct their own due diligence. The GeoTeam has received no compensation for the dissemination of this report. The GeoTeam may or may not have a position in any stocks mentioned in this article prior to its publication.