Summary

Quadrant 4 Systems Corporation (QFOR) is engaged in providing IT consulting services, cloud-based platform-as-a-service (PaaS) and software-as-a-service (SaaS) products to the health insurance, media and education verticals. The Company’s core platforms include QHIX/QBIX, a cloud-based health insurance exchange and benefits management platform; QBLITZ, a cloud-based digital media platform, and QEDX, a cloud-based education platform for K-12 students, each of which incorporates the Company’s Social Media, Mobility, Analytics and Cloud (SMAC) technologies. Its services include consulting, application life cycle management, enterprise applications and data management, mobility applications and business analytics.

Our elevator pitch on this uniquely speculative situation is as follows:

- Former CEO Nandu Thondavadi and CFO Dhru Desai were arrested in November 2016 over misrepresenting company financials starting in January 2013.

- On the announcement of the news, the stock dropped from roughly $0.20 to $0.03 per share; possibly an overreaction by the market depending on the future of the business.

- An analysis of the court documents indicates to us that the financial misrepresentation should not significantly influence the operating business going forward.

- With new management in place and the questionable characters out of the company, QFOR, trading at less than 3 times ttm EV/EBITDA, could have meaningful upside potential.

- The uncertainty surrounding the stock at this moment has caused the share price to be depressed. There are many caveats, mainly:

- The operating business could see significant customer migration

- The company has a history of not being transparent, related party transactions, and third party promotions

- The company is currently on default notice, and has to regain confidence with its stakeholders (customers, suppliers, employees, creditors, investors)

Background

Quadrant 4 was incorporated in Florida in 1990 as Sun Express Group. The company has been trading under the ticker QFOR since 2010, and has been led by CFO and Chairman Dhru Desai and CEO Nandu Thondavadi since 2010, when both joined QFOR’s management.

Let’s get as much of the ugly stuff on the record as possible, as an investment in QFOR here should only be made when and if the undesirable and relatively odious past of the company has been fully understood.

Dhru Desai has a poor track record of investing in public companies. Over the past 14 years, investors have seen Desai-related investments go to zero in Fastcomm, Solstice Resorts and eNucleus. Dhru and Nandu have been involved in litigation over the past 14 years with prior disgruntled partners. A quick dig into QFOR suggests that third parties like Red Chip have promoted the stock in the past. Those not familiar with Red Chip should know that the firm has a questionable track record when it comes to discriminating which companies to cover, and how it goes about doing so. We also noticed that there have been past pump campaigns exacted by third parties, the last one being noticed in March of 2015 by theotc.today (formerly d/b/a pumpanddumps.com). Whether the company paid for these campaigns is unknown, as these occurred under old management.

During Dhru’s and Nandu’s tenure, QFOR acquired a range of companies with varying success, and arranged for a complicated and messy capital structure. Among the acquired companies was EmpowHR, a web-based benefits administration platform company that Q4 Systems purchased in 2012. EmpwHR founder Robert Steele was brought on board to direct Q4’s global marketing team as part of this acquisition. Since January 2015, QFOR has acquired:

- Mobile education provider Brainchild Corporation for a total consideration of $2M

- IT provider DialedIn Corp. and DUS Corp for a combined consideration of $835k

- Business process consulting service company Stratitude Inc. for a $6.8M consideration in November 2016.

In November 2016 QFOR also acquired Great Parent Academy LLC for $2.7m in QFOR shares and an earn-out agreement. Many of the bigger acquisitions employ a combination of stock consideration, cash, and earn-out payments, which makes the company less transparent, enabling the former CFO and CEO to misrepresent financials for an extended period.

The Lawsuit

In November 2016, the FBI officially charged Dhru Desai and Nandu Thondavadi. The lawsuit alleges Thondavadi and Desai’s scheme involved misrepresenting and concealing the acquisition terms related to the Teledata and Momentum Mobile acquisitions, as well as misrepresenting the amount of and means of payment for liabilities associated with the Downtown Capital Partners. The lawsuit also alleges the concealment of related party transactions. The scheme’s alleged objectives were, among other things:

- To conceal and avoid publicly reporting all of Q4’s liabilities.

- To persuade investors through misrepresentations and concealment related to Q4’s cash flow and acquisitions that Q4’s profitability would continue to grow.

- To artificially inflate the share price of Q4’s stock.

Desai and Thondavadi had a strong financial incentive as owners of QFOR’s stock, representing ownership of 11.1% and 9.8%, respectively, of QFOR’s shares as of the company’s 2015 10-K.

On or around October 2016, the FBI began investigating Nandu Thondavadi and Dhru Desai, based upon information provided by the U.S. Securities and Exchange Commission (“SEC”).

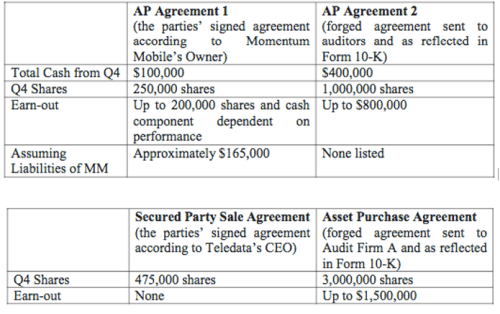

The lawsuit alleges that for the Teledate acquisition and the Momentum Mobile acquisition in 2013, CFO Dhru Desai sent materially different agreements to the auditors than were signed by the parties. Here is an overview of the differences between the actual agreement and the documents Desai sent to auditors.

In July 2011, lender Downtown Capital partners filed a breach of contract suit against Q4, Desai, Thondavadi and other individuals. Thondavadi and Desai subsequently entered into a Settlement Agreement with Downtown Capital Partners, requiring cash payments totaling approximately $1.75 million to settle the judgment and the attorney’s fees claims. The cash was wired by QFOR.

However, Desai sent a different Settlement Agreement to the company’s auditors, which purported to settle the judgment by providing more than 1.8 million shares of QFOR stock to Downtown Capital Partners. The provided Settlement Agreement made no mention of cash payments or wire transfers to Downtown Capital Partners, nor did it mention the approximate $1.2 million in attorney’s fees and costs that are part of the $1.75 million settlement.

The last thing that the lawsuit alleges is that Thondavadi lied in court in response to specific questions about whether he had ever possessed or exercised any financial or operational control over a company known as Core Information Technology Solutions, Inc. (CITS), a customer of Q4. Thondavadi has falsely stated under oath in SEC hearings in May 2016 that he has not exercised any control over CITS, while he in fact did. As a result, QFOR failed to disclose related party transactions.

Four months after Thondavadi’s hearing, QFOR issued an amended 10-K for 2015, adding over a page in disclosure of related party transactions, while there were no disclosures in the original document.

While reputational damages can be immense, the amount of misrepresentation is relatively small, given QFOR’s size. It is also important to understand that the misrepresentation only affected cash balance and share count. With roughly 108 million diluted shares outstanding, and $42M in revenue in the last 9 months (ending Sept 2016), the potential differences in share count of roughly 3M and cash and earn-outs of roughly $2M seem relatively small. New CEO Robert Steele is currently working through the paper trail of past acquisitions. In light of the lawsuit, the previously issued financial statements of the company cannot be relied on, and it is not clear what the exact adjustments will amount to.

Recent Events

On September 30, 2016, the company issued filings disclosing the intent to go-dark through a reverse-split that aimed at reducing the number of shareholders below the 300 threshold required by the SEC. This would enable QFOR to stop filing with the SEC. Under the 1for 10 reverse split proposal, all shareholders left with fractional shares would get bought out in cash equal to $0.50 per share pre-split. The board also proposed moving the company from Illinois to Delaware.

In October the company hired new auditors.

On November 30, Dhru Desai and Nandu Thondavadi were arrested and charged in a criminal complaint with wire fraud among other crimes. On the same day, QFOR received a Wells Notice from the SEC, which indicates that the SEC plans to bring an enforcement action against the company, but gives the company time to respond with information to avert enforcement.

Consequential to Desai and Thondavadi getting arrested, creditors of QFOR issued default notices. On December 1, BMO Harris Bank issued a formal notice of default and there was $17,847,316 outstanding at the date thereof. On December 3, BIP Lender issued a default notice, with $5,075,000 outstanding under their credit agreement with the company. The default notices increase the interest rates by 2% for the Harris Bank loan and by 3% for the BIP loan. Additionally, the default notices force QFOR to operate to budget and satisfy creditors’ conditions before they can get out of the default status.

In light of these events, all plans relating to a go-dark transaction have been dispensed.

On December 29, board member Eric Gurr resigned.

Getting out of the Mess

After the arrest of Desai and Thondavadi, QFOR appointed Robert Steele, formerly the President of the company’s Health Division, as Chief Executive Officer and Shekhar Iyer, formerly the President of the company’s Education Division, as Chief Operating Officer. Robert Steele was brought in to the company as part of an acquisition in 2012, and has been Chief Sales and Marketing Officer since June, 2013.

Steele immediately opened communication channels to give employees, customers, creditors, and other stakeholders to increase transparency on much needed information, and to resolve some uncertainty surrounding all of the recent events stated above. During December 2016, we reached out to the company to understand what was going on after Desai’s and Thondavadi’s departure. Employees at QFOR assured us that the situation has been difficult and that many employees temporarily feared for their job positions, but that the situation is improving day by day.

Mr. Steele shared in a recent interview with GeoInvesting three themes that should guide QFOR in 2017: transparency, accountability, and focus. Steele reiterated several times that he and Shekhar are capable of running the company, and that the QFOR is going to be run very differently going forward. According to Steele, Desai and Thondavadi kept the company close to their chest and lacked the appropriate degree of transparency and accountability a public company should have.

On the product side, Steele stressed that the operational focus for 2017 is on platform services in the segments of healthcare, education, and finance/IT services. The plan is to leverage QFOR’s expertise in creating cloud-based platforms for ecosystems. Mr. Steele was particularly excited about the new licensing agreement for the healthcare platform QHIX with a major software and service firm active in the healthcare sector. This agreement was signed in March 2016 and has been disclosed in previous filings.

Robert Steele made it clear that he does not agree with QFOR’s legacy growth strategy that was driven by acquisitions. He wants to concentrate on growing the business organically. We also voiced our opinion that we felt the share count was a little high vs. the company’s size. He seemed to agree with our assessment.

Steele has to assure customers and suppliers of QFOR’s reliability going forward. While we view the loss of customers as a main risk for the company, Steele feels confident about his ability to keep significant customers, and even improve these relationships going forward.

Steele also has to meet with creditors, mainly BMO and BIP, to get QFOR out of default status. The timeline to find an arrangement with creditors is about 6 months, and may involve a refinancing of the BMO facility.

Economics

The Company’s largest customer represented 14.9% and 13.7% of consolidated revenues for the years ended December 31, 2015 and 2014, respectively. The company sells to 22 strategic customers, the top ten of which make up approximately 50% of the company’s total revenue. While there is some customer concentration risk, Mr. Steele wanted to make clear in his interview with us that he feels confident about maintaining the important client relationships through improved communication.

Roughly 80% of the company’s revenue is from IT consulting services, and the majority of the remaining 20% comes from the education and healthcare platforms. While the IT consulting services are not considered recurring revenue, a majority of the consulting services are delivered to repeat customers. Expected EBITDA margins for the IT consulting segment are between 10% and 15%, while SaaS/PaaS margins are expected to be significantly higher. The company currently counts roughly 500 employees in India, and about 420 in the USA, with the majority located in California through the recent Stratitude acquisition.

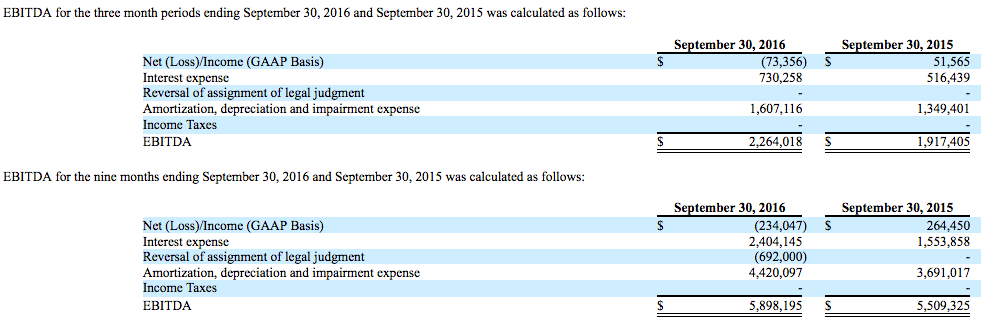

QFOR has significant write-offs and amortization expenses from previous acquisitions. Adding these back to calculate adjusted EBITDA gives the impression of a profitable business. For the nine months ended September 30, 2016, QFOR generated $42M in Revenue and $5.9M in EBITDA, implying an annual revenue and EBITDA run rate of approximately $56M and $7.9M respectively.

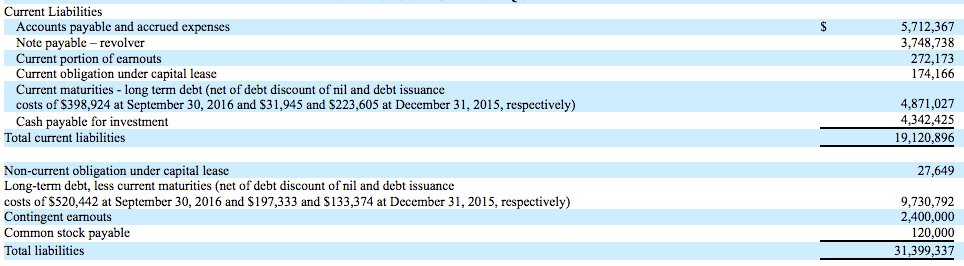

The balance sheet and capital structure is a little troublesome, mainly because of overambitious acquisition strategy by the former management team. As of September 30, 2016 about $30M of $47M on the asset side represent intangibles, goodwill, and capitalized software development costs. As of September 30, 2016, QFOR had about $26m in liabilities that it eventually must pay off. It also had roughly 108M diluted shares outstanding, which excludes 5.1M potentially issuable shares because the securities are currently deep-out-of-the-money and antidilutive.

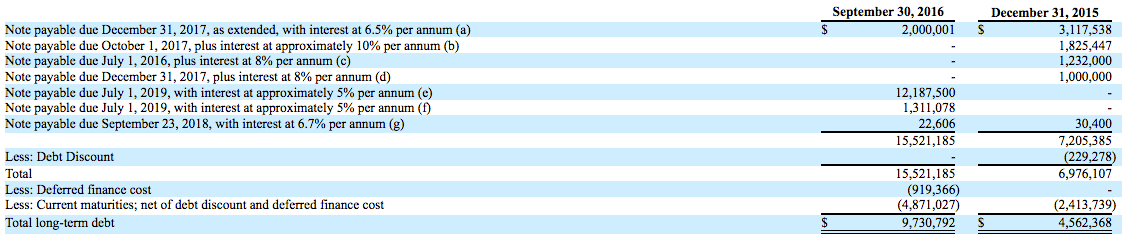

QFOR used to have a variety of credit lines and agreements, but repaid many of them after entering a financing agreement with BMO Harris Bank on July 1, 2016 under which QFOR is granted up to $25m under different credit facilities.

On November 3, 2016, Quadrant 4 entered into a $5,075,000 senior subordinated credit agreement with a creditor group led by BIP Lender, LLC to finance the Stratitude acquisition.

A SaaS/PaaS company with a gross margin around 40% would typically be trading at an EBITDA multiple between 10 and 15, with an industry average EV/EBITDA of 13.6. While we do not believe the company can be considered a “true” SaaS, we think an EV/EBITDA multiple of 6 should be at the low end of the valuation range for a profitable company, implying a stock price of $0.28 per share assuming 108m shares outstanding. This represents nearly 400% upside from the stock’s current $0.07 price.

Risk Factors

We want to reiterate that an investment in QFOR is a high risk, high reward situation. The following outlines the main risks that we see with the investment:

- QFOR might still suffer substantial operational repercussions from the departure of their leading figures. Suppliers, customers, and key employees could be turned off by the recent developments and leave the company.

- The company is currently in default with lenders and is therefore effectively under the control of creditors (in a default situation, the fiduciary duty of management shifts from equity holders to credit holders). If creditors decide to liquidate assets and close down the company, equity holders might be left with worthless shares.

- Because of the company’s default status, investors cannot expect too much communication until the situation is resolved, resulting in little visibility. The company was contemplating a go-dark proposition just before the lawsuits, and might end up never reporting financials again.

- Robert Steele and senior management are facing an extremely challenging situation and have to pull the company out of the mess it is currently in. Therefore there is a lot of execution risk involved.

- Warren Buffett is sometimes quoted saying “If you see one cockroach there are probably many”. The “Cockroach theory” may apply in this situation too.

- Going forward, it is not clear what the exact adjustments to past financial statements will be. It could be the case that Dhru Desai and Nandu Thondavadi committed other wire frauds that investors and regulators are currently unaware of or that the company engaged in other fraudulent acts that have yet to be discovered by regulators and/or the market.

Conclusion

We believe the extreme stock price reaction to the lawsuit might be an overreaction. The lack of certainty regarding the business’ future and lack of visibility contributed to investors fire-selling the stock. At the same time, we view the departure of Desai and Thondavadi as an opportunity for QFOR to reboot and emerge as a different, credible company.

We conclude that an investment in QFOR at current prices presents a favorable risk/reward situation, despite being extremely speculative in nature. We want to reiterate that this is a high-risk special situation and the total loss of capital is a very real and conceivable possibility.

---

Disclaimer

You agree that you shall not republish or redistribute in any medium any information on the contained in this report without our express written authorization. You acknowledge that GeoInvesting is not registered as an exchange, broker-dealer or investment advisor under any federal or state securities laws, and that GeoInvesting has not provided you with any individualized investment advice or information. Nothing in this report should be construed to be an offer or sale of any security. You should consult your financial advisor before making any investment decision or engaging in any securities transaction as investing in any securities mentioned in the report may or may not be suitable to you or for your particular circumstances. Unless otherwise noted and/or explicitly disclosed, GeoInvesting, its affiliates, and the third party information providers providing content to the report may hold short positions, long positions or options in securities mentioned in the report and related documents and otherwise may effect purchase or sale transactions in such securities.

GeoInvesting, its affiliates, and the information providers make no warranties, express or implied, as to the accuracy, adequacy or completeness of any of the information contained in the report. All such materials are provided to you on an ‘as is’ basis, without any warranties as to merchantability or fitness neither for a particular purpose or use nor with respect to the results which may be obtained from the use of such materials. GeoInvesting, its affiliates, and the information providers shall have no responsibility or liability for any errors or omissions nor shall they be liable for any damages, whether direct or indirect, special or consequential even if they have been advised of the possibility of such damages. In no event shall the liability of GeoInvesting, any of its affiliates, or the information providers pursuant to any cause of action, whether in contract, tort, or otherwise exceed the fee paid by you for access to such materials in the month in which such cause of action is alleged to have arisen. Furthermore, GeoInvesting shall have no responsibility or liability for delays or failures due to circumstances beyond its control.

Our research and reports express our opinions, which we have based upon generally available information, field research, inferences and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied.

See Full Disclaimer here - http://geoinvesting.com/terms-conditions-privacy-policy/