The sports nutritional supplements industry is a crowded space of undifferentiated products, with a history of dilution and capital destruction. If the thought of investing in the space doesn't make you uneasy, you might need to check your smell test-ometer.

Fitlife Brands, Inc. (NASDAQ:FTLF) is a bit different.

FTLF sells sports nutritional supplements, primarily to GNC franchise stores and it ...

- operates to be profitable and cash flow positive

- experienced temporary not terminal issues last year that investors misunderstood

- those issues anniversaried, so comps are low

- combined with the acquisition of a distressed competitor should result in 60% y/y sales growth for 2016 and EPS in the $0.20-$0.25 range for the year.

- Longer term there’s an add’l boost from GNC's "refranchising strategy" but also a lot of uncertainty around this core customer, which has some “warts”.

... if these attributes hold steady there is an opportunity for investors to earn a potentially high return in less than a year's time.

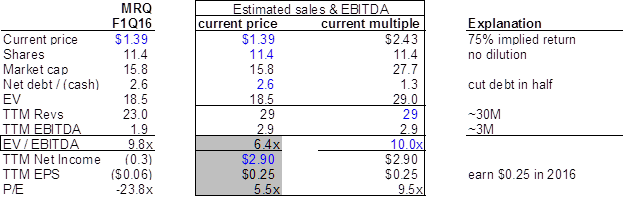

FTLF is a $16M mkt cap / $19M EV trading at 10x trailing twelve month EBITDA, a not unreasonable multiple for a company that should produce 60% topline growth plus cash flow generation.

However, trailing-EBITDA was hurt last year after GNC changed its franchise distribution policy. With the rebound from - and anniversary of - that issue, and the additional boost from iSatori – acquired in Oct 2015 to provide new products, brands and distribution channels – FTLF should be able to produce $29M in sales, $2.9M in net income and $0.20-$0.25 in 2016. That’s would be about a 3-fold growth in income.

Against that forecast the stock is trading at 6x estimated profits, an incredibly inexpensive multiple for a company growing topline 60% y/y.

If the company were to trade at its existing 10x multiple against forecast $2.9M EBITDA, it would imply a ~$2.45 share price, or 75% return. That in a nutshell is the thesis on the stock.

1. Operates different from other companies in the industry. Most simply put, FTLF is managed to run for profit and cash flow and that alone, strangely enough, is one key differentiator between itself and its competitors.

From a financial perspective, the drivers of that differentiation are twofold. Since the current CFO joined the company, they have lowered S&M spend to just ~10%-15% of revenues compared to 15%-20% for MSLP and north of 20% for Isatori Inc (OOTC:IFIT), which it acquired in late 2015.

It also runs the company with exceedingly lean overhead, lowering G&A costs towards the same 10%-15% band vs north of 30% for MSLP.

In essence, it can do this b/c the company solves a different sort of problem than its competitors. Where MSLP and its like want to get its customers "ripped" – reinforcing that message with expensive celebrity endorsements - FTLF aims to make more money for its core customers, the GNC franchise owner.

It provides a product that is similar to – and some believe better than – the more expensive branded items on the wall. It shares the money it saves on lower S&M and G&A costs with the GNC Franchise owner and that in turn, provides the franchisee a higher margin product to sell.

It’s a classic grassroots retail strategy. At the GNC franchises I visited, the store managers loved the products, they loved selling it even more b/c it brought them the most margin, and they experienced fewer returns along the way.

As evidence of the brand loyalty among GNC Franchisees, was told by an attendee that at GNC’s recent franchise convention, attendance at FTLF’s presentation exceeded all its competitors with fanatical appreciation for the company and product.

2. Last year, the company experienced temporary issues investors misunderstood.

A franchise owner of a GNC store can allocate 10%-20% of its shelf space to whatever products it wants. For several years, FTLF went door to door to GNC franchisees selling a like product of the celebrity endorsed products that adorn the walls.

These products - 3rd party manufactured - provide the customer a sort of "generic" version of what they came into buy and concurrently is one of the highest margin products in the store for the franchise owner.

I have visited several GNC franchise stores and the franchise owners all affirmed, FTLF is the profit driver for their stores, customers like the product, it generates few returns, and has a high reorder rate.

Incidentally, I also heard repeatedly that Fitlife reminds them of Cellucor 10 years ago. (Cellucor is a successful brand now selling in Costco. It is owned by NutraBolt which received an undisclosed investment from PE in 2014).

By 2014, FTLF had so deeply penetrated the GNC Franchise ecosystem that it was selling DIRECTLY to more than 900 out of ~1,000 domestic GNC stores. Franchisees would order quarterly directly from FTLF, pay with credit cards and FTLF would ship out product direct to the franchise store.

Like any good company smelling a low cost opportunity, GNC changed that. They decided FTLF could no longer sell direct to franchisees but had to sell via the corporate wholesale system, to get a cut of the sale.

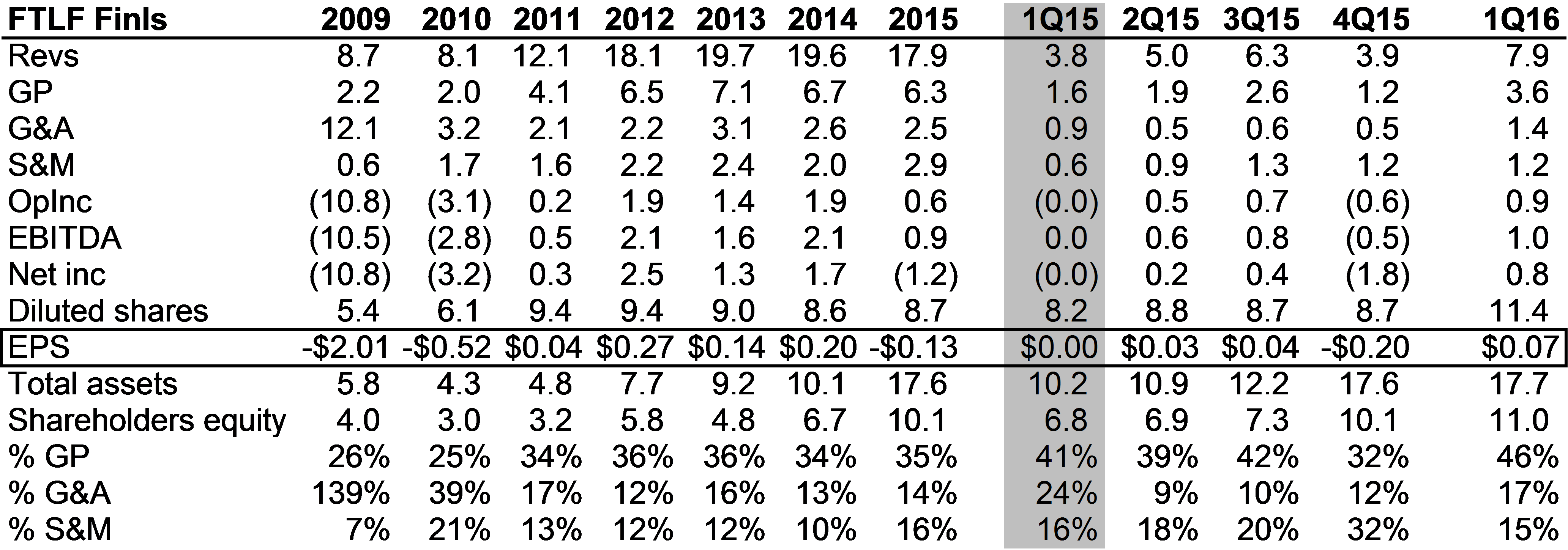

As a result of that channel change, through 9-mos of 2014, customers stocked up on direct orders, and sales skyrocketed. Then the distribution channel shifted in 4Q14 and sales plummeted. The channel disruption impacted mostly 1H15 as sales clawed back to slight y/y growth in the back half of 2015.

3. These issues have “anniversaried”

In 4Q15, the initial impact of the channel disruption lapped itself.

In 1Q16 organic growth increased 37% to $5.3M.

4. Combined with the acquisition of a distressed competitor.

At the end of 2015, FTLF not only lapped the channel disruption it closed closed on the acquisition of iSatori, a distressed maker of a complimentary nutritional supplement that has distribution channels into independent channels and growing brand recognition.

In 1Q16, this business added $2.6M in sales.

As a result of the easy comps acquisition, total sales increased 104% in 1Q16 to $7.9M. I expect growth for the full year should be roughly 63%.

Concurrently, margins should remain steady as the costs eliminated from credit card fees and shipping are offset by GNC's cut of the sale.

5. GNC: Warts and refranchising, but what is the long term strategy.

THE PRIMARY RISK with the thesis, beyond the standard boilerplate "anything can happen" is, simply put, "WTF is going on with GNC."

Over at GNC, all the headline metrics are declining, but the business is far from terminal. 2Q16 sales were $673M down 2.4% while franchise sales declined 6.6%. Activist shareholders are involved in the name. The CEO just left, which is a good thing in this case. As of yesterday (7/28), the stock is down -35% YTD vs 6% for the S&P and -52% over last 52-weeks.

Questions around it: Is it going to merge with Vitamin Shoppe? Can it gain online traction, where more than 30% of supplement sales have migrated? Can it fix its pricing strategy? This article sums up the attitudes and sentiment on the company and the stock.

But putting aside fear and hysteria for a moment, GNC generated $300M in FCF in 2015, up from $230M in 2014. It generated $110M through 2Q16 vs $160M in 1Q15. This is more than enough to service the $1.6B in debt outstanding and also continue to buy back shares.

At 2Q16, GNC operated 3,506 corporate owned stores and 1,163 franchise owned stores. In 1Q16, the last time it reported such information, it generated $33k in operating income per franchise store compared to $23k OpInc / corporate store. That's a 1.5x difference.

Understanding the profitability differential b/t franchise and corporate stores is key to understanding why GNC announced a "refranchising strategy" late last year to convert 200 corporate stores to franchises this year, and 1,000 stores over the next three years.

Franchisees are the profit generators to GNC. And, FTLF is the profit generator to the franchisee.

Is all this all really so straightforward? Additional risks and conclusion.

There two big structural headwinds in the stock.

GNC is not going out of business tomorrow, but it can set whatever terms it wants. For example, with FTLF now selling product through GNC wholesaling, payment terms have changed. DSO’s are up to 60 days vs 53 last year and 30 days before the channel disruption. We expect this will remain a constant going forward.

FTLF is adapting as well. They understand that the only way around the DSO issue - and the over reliance on GNC in general - is to open new channels, which FTLF is pursuing.

I view FTLF’s core capability as getting good product on shelves and sold. The CEO John Wilson, is a former accountant who worked in the finance department at KO before transitioning to operations there. Incidentally he is also the son of John C Wilson, former CFO of the venerable Emerson Electric (EMR) from 1975-1986. So Wilson knows what success looks like and how to get product on shelves.

The CFO Mike Abrams is a former investment banker at HC Wainwright and Burnham Hill who joined the company b/c he saw a way to run a business different from other companies in the space.

Channel diversification was an impetus for the iSatori deal. It Not only has FTLF already turned the acquired business profitable but the acquisition has enabled the company to lower its reliance on GNC Franchise stores from 90% of sales to less than 70% of sales, still substantial but essential for health, growth and safety.

The second structural headwind is that the "push" strategy that works at GNC franchise stores simply won't work online. The company needs to generate an online base to both diversify its distribution channel away from GNC and remain relevant in a world where sales continue to migrate online.

I don't know the future. I don't know what's going to happen at GNC over the next three years. Will it get bought? Will it be an acquirer? If it is acquired I have to assume GNC will continue to honor its franchise agreements.

But I feel confidence in the misunderstood past and likely near term future. And as investors see growth and profits, they tend to bid higher multiples. So even while there is uncertainty around GNC, an educated investor can manage that risk and find opportunity in the markets’ misunderstanding.

DISCLAIMER: GeoInvesting has no affiliation with the author of this report in any way and is not endorsing his research, nor has GeoInvesting vetted this information in any way. The GeoTeam does not attest to the accuracy of the information contained in this report and always urges investors to conduct their own due diligence. The GeoTeam has received no compensation for the dissemination of this report. The GeoTeam may or may not have a position in any stocks mentioned in this article prior to its publication.