Business

Electromed (ELMD) was founded by Mr. Robert Hansen and Mr. Craig Hansen and incorporated in Minnesota in 1992. In 2010, the company went public. Electromed is a medical device microcap that develops and provides innovative airway clearance products applying High Frequency Chest Wall Oscillation technologies in pulmonary care for patients of all ages. Their flagship product is the Smarvest SQL which replaced their Smartvest SV2100. A picture of the Smarvest is shown below.

So as you can see, the Smartvest is a vest that you actually wear and its purpose is to stimulate mini coughs in order to loosen mucus from the walls of lung airways and/or propel mucus toward larger airways, where it can be easily coughed out. So as you may have probably already figured out at this point, Electromed’s target patients are people with Cystic Fibrosis, Bronchitis, COPD, or some other disease that affect airway clearance. A typical CF patient would use the Smartvest about twice per day and 5-20 minutes per session. A video could demonstrate the Smartvest better than I can using words, so here is one:

https://www.youtube.com/watch?v=SniurItA5H0

Home Health Care

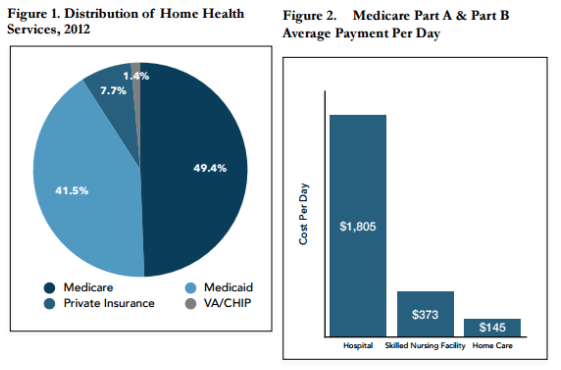

An investment in Electroemd is also a play on the home health care market as that is where the majority of Electromed’s revenue comes from. Home health care is a term that describes a wide range of services and/ or products that can be given to you for an illness instead of in a hospital or some other facility. The home health care market has been booming recently and will continue to do so in the foreseeable future and one of the primary reasons for that is because it actually cuts down on health care costs. Just think of how much it cost to stay overnight in a hospital compared to home. Secondary reasons include the aging baby boomers and better treatment in some instances. Here are some articles about the industry:

http://www.thegazette.com/industry-experiencing-rapid-growth-20140511

http://www.homecare100.com/homecare100/files/2014/2014-home-health-care-market-outlook.pdf

So the home health care market accounts for more than 60% of the actual health care market and the majority of it are paid by Medicare and Medicaid.

In the case of Electomed, the Smartvest is a much cheaper alternative than having to see a physio-therapist every day. There are also other reasons why the Smarvest would help reduce costs. In the 10-K:

“Studies show that HFCWO therapy is as effective an airway clearance method for patients who have cystic fibrosis or other forms of compromised pulmonary function as traditional chest physio-therapy administered by a respiratory therapist. However, HFCWO can be self-administered, relieving a caregiver of participation in the therapy, and eliminating the attendant cost of an in-home care provider. We believe the treatments are cost-effective primarily because they reduce a patient’s risk of respiratory infections and other secondary complications that are associated with impaired mucus transport. Secondary complications, such as pneumonia, may be serious or life-threatening and often result in costly hospital visits.”

Financials

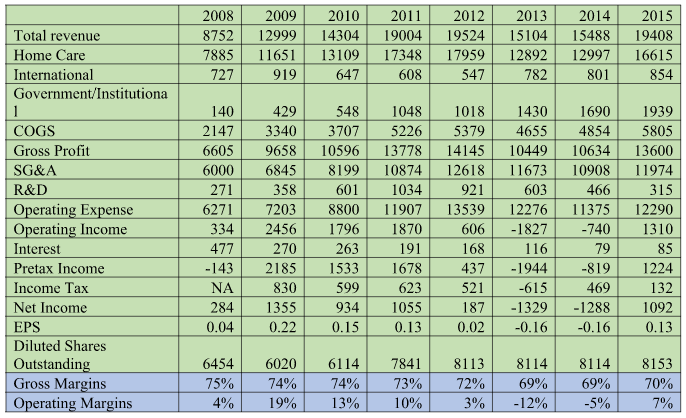

Electromed was able to achieve double digit growth from 2008 to 2011 before it briefly stalled in 2012 fell off a cliff in 2013. The founder and CEO resigned on May 4, 2012 to pursue other opportunities in another company in which he is the founder of and Kathleen Skarvan took over on November 29, 2012. On the surface, this looks like the CEO does not have confidence in the company or else why would he leave to join another company? Another possible concern would be the qualifications of the new CEO. OEM Fabricators, Hutchinson Technology Incorporated, and Disk Drive Components Division. What do these names have in common? Well these are all companies the current CEO has previously worked for and not a single one of them is related to biotech or medical devices. An investor at the time would be very hesitant to call a bottom, but Kathleen actually did a good job turning the company around which goes to show that you can still be a good manager even if you don’t have industry experience.

http://www.businesswire.com/news/home/20120514006574/en/Electromed-Chairman-CEO-Robert-D.-Hansen-Announces

You can see that the company also have very high gross margins (>70%) and operating leverage. The 26% revenue growth in 2015 lead to a 300% change in net income (it was negative in 2014) which resulted in a EPS of 0.13. The release of the Smartvest SQL definitely played a role in the turnaround effort. Below is the actual 510(k) which is a form that medical device manufacturer has to file before they can market their product.

http://www.accessdata.fda.gov/cdrh_docs/pdf13/k132794.pdf

Now Electromed’s latest quarter (Q2 2016) was even better with revenue of over $6 million and EPS of 0.13 which is the same Electromed did for the entire 2015 fiscal year. It should be noted that reimbursement timing helped them out a bit. According to the 10-Q, about $250,000 in revenue was shiftd to the current quarter due to reimbursement timing. If you assume the same gross margins (78.2%) and don't adjust any selling expense, operating income should've been $195,500 lower. Using the same tax rate of 13%, we have a net income of $897,343 which would give us an EPS of 0.11 instead of 0.13. Now even that is still very impressive. The company seems confident that this level of revenue is sustainable and they hired a VP of sales. The CEO stated that “We believe we have raised the range on the level of net revenues we can generate quarterly. This should, in turn, result in stronger operating income as we expect our revenues will grow more quickly than our expense base.”

Another minor tailwind is the Consolidated Appropriations Act, 2016 that included a two-year moratorium on the medical device excise tax under Obamacare. The excise tax was 2.5% which is quite huge for a company with only 7% operating margins. However, I believe this will be offset by the increase n R&D in the future. You can see that R&D started dropping off since 2012 and has continued dropping since the Smartvest SQL was approved. This is quite normal, but once the company starts R&D for the next generation product, expenses should start to increase.

http://finance.yahoo.com/news/electromed-inc-reports-record-6-213000755.html

According to the company, the potential market size for the Smartvest is about $110-120 million. This is not exactly huge and might put a cap on future growth, but it still quite large compare to their current revenues with plenty of room to grow.

For valuation purposes, if ELMD is able to achieve EPS of 0.09 to 0.13 per quarter going forward and you apply a PE multiple of 15, it is conservatively worth $5.4 to $7.8, which is about a 30% to 100% upside from today’s price ($3.90).

Caveat

-CEO does not have much experience in this sector. So far, this has not been shown to be a negative.

-Quarterly revenue will fluctuate due to reimbursement timing.