Business

Smith-Midland (Smith-Midland Corporation (NASDAQ:SMID)) is a microcap that invents, develops, manufactures, markets, leases, licenses, sells, and installs a broad array of precast concrete products for use primarily in the construction, highway, utilities and farming industries. Their customers are primarily general contractors and federal, state, and local transportation authorities located in the Mid-Atlantic, Northeastern, Midwestern and Southeastern regions of the United States.

Precast Concrete

“Precast concrete is a construction product produced by casting concrete in a reusable mold or "form" which is then cured in a controlled environment, transported to the construction site and lifted into place. In contrast, standard concrete is poured into site-specific forms and cured on site.” (Wikipedia)

This is in contrast to ready-mixed concrete which is manufactured in a factory or batching plant and then delivered to a work site by truck mounted in transit mixers.

Precast concrete is one of the most popular construction material and the reason are due to:

- Tough, hard surface, making it extremely resistant to everyday dents and dings.

- Resistant to rain penetration, flood damage, wind-blown debris.

- Quiet and soundproof making it an ideal choice for commercial and residential construction.

- Can be formed in any shape, size, texture.

- Wi-Fi-compatible because it does not interfere with radio signals.

- Fireproof. Cannot catch fire, burn, or drip molten particles.

- Durable-Some buildings from 2000 years go are still standing.

- Increases with strength over time.

- Corrosion resistant and resistant to microbial attacks.

- Can be rapidly erected on site. Can be erected just in time so there is no need for storage.

- Appeals to investors due to resistance to everyday and extreme events.

(http://www.modularconnections.com/files/QuickSiteImages/100_adantages_of_precast_concrete.pdf)

Business Strategy

First, I would like to discuss how the bidding process works and how Smith-Midland actually makes money. For a construction project, a general contractor that provides the construction service bids for it. The general contractor does not have materials because they are focused on the construction and not manufacturing. The materials they need are provided by companies like Smith-Midland who will bid to be able to provide the materials for the general contractor. Smith-Midland has other sources of revenue such as shipping and installation and licensing, but a big part of their revenue still comes from product sales.

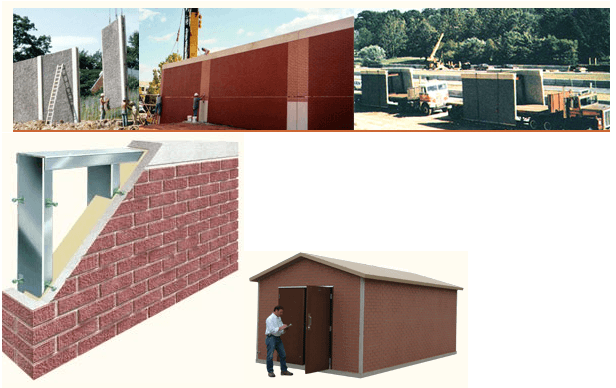

As you can imagine, this is a commodity industry and very cyclical, but that doesn’t mean there aren’t ways for companies to differentiate themselves. The way companies do that is by creating products with a unique set of properties that are better than their competitors. Smith-Midland accomplishes this with their innovate and patented products such as the SlenderWall which is a lightweight, energy efficient concrete and steel exterior wall panel used for building construction; J-J Hooks, a highway safety barrier; Easi-Set and Easi-Span, a transportable concrete building; BeachPrisms, a erosion mitigating modules. The company also produces custom precast concrete and generic highway sound barriers. Below are pictures of some products:

As a further validation that these are superior products, the company license these products out to other precasters. Their J-J Hooks® Barrier, Easi-Set™ and Easi-Span™ Precast Buildings, SlenderWall™, SoftSound™ and Beach Prisms™ as well as certain non-proprietary products, such as the Company's cattleguards, and water and feed troughs all can be licensed out.

The terms of the license call for an initial one-time administration and training fee ranging from approximately $25,000 to $60,000 and royalty ranging from typically 4% to 6% of the net sales of the licensed product. The fact that they have over 65 licensees worldwide does imply some sort of product superiority. Even Oldcastle, the largest precaster in North America is a licensee. Now you might be asking yourself why SMID is not dominating this industry when they have superior products. The answer to that question is that superior does not mean cheaper. Many customers are happy with the good-enough products or products that are slightly inferior but good enough for the job and cheaper. For some people, the huge cost of building with more expensive construction materials just isn’t worth it.

Note: Top 5 Largest concrete producers are:

1) Oldcastle: 280 plants; $7.46 billion in revenue in 2013

2) HeidelbergCement: 146 plant; $4.63 billion

3) MDU Resources Group: 72 plants; $4.47 billion

4) Lafarge; 180 plants; $4.27 billion

5) Holcim: 263 plants; $3.55 billion

(http://www.theconcreteproducer.com/business/tcps-top-10-producers_o.aspx)

It should be noted that if you go back to the company’s 2004 annual report, the company already carried most of its current product lines, except for the beach prism. So they haven’t been able to produce many new products, but they have been able to improve on their existing products. Despite this, I would not count on product differentiation to be much of a competitive advantage. Pricing seems to be a big factor, and while customers do care a lot about quality, it’s very difficult to "out-quality" (don’t think that’s a word) your competitors in something like precast concrete and in times where everyone was bidding at low prices, Smith-Midland saw revenue decline. (Note: In FY 2011 and 2012, SMID cites competitors bidding at very low prices as reasons for YoY revenue decline).

Industry Forecast

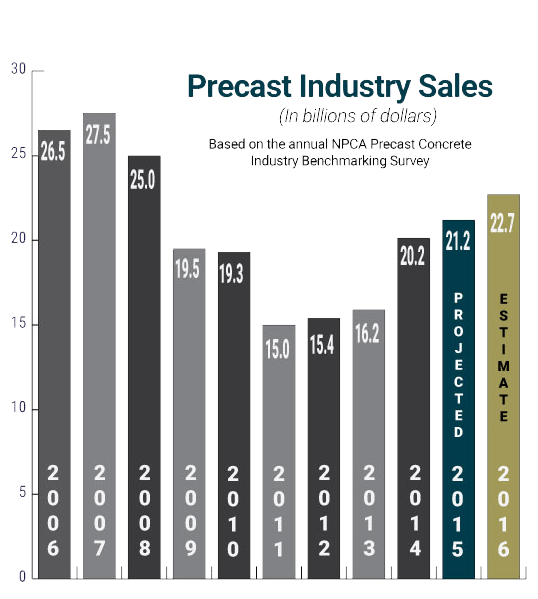

Ever since the great recession, the precast industry has still not recovered to pre-recession levels. According to Freedoniagroup, US demand for precast concrete products is forecast to rise 6.4 percent per year to $12.2 billion in 2018, spurred by rebounding construction activity.”

- Nonresidential building construction applications accounted for the largest share of precast concrete products demand in 2013 and are expected to see the most rapid gains in demand going forward.

- The residential market for precast concrete is forecast to see above average annual growth through 2018 due to increase in housing completions. (I don’t think looking at month to month housing start data is a good idea just like looking at the day to day movement in stock prices is also not a good idea.) I would not be worried about a downturn in housing unless it is very obvious and you see the date falling off a cliff.

http://www.freedoniagroup.com/industry-study/3244/precast-concrete-products.htm

http://www.tradingeconomics.com/united-states/housing-starts

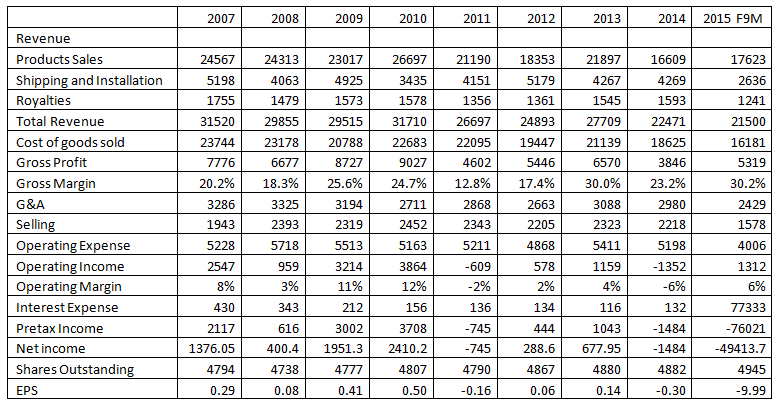

Financials (in thousands)

(Note: Only the first 3 quarter of FY2015 results were reported at the time of this writing.)

As you can see above, revenue tends to fluctuate a lot and margins are very thin. A few things I would like to point out:

- Revenues only declined by one million from 2008 to 2009 and we all know that was a terrible year.

- Results of the great recession of 2008 can be felt many years after the crisis. For example, SMID's five-year average revenue after 2008 was lower than five-year average revenue pre-2008.

- Smith-Midland can still have a great year even in the middle of a recession, like in 2010 if, they win some large contracts.

- Sales of their barrier rental products tend to increase dramatically during every presidential election and inauguration year. (Such as this year)

- There is a set of products that are quite recession resistant. According to the company:

In FY2014, CEO claims in the shareholder letter that “The Great Recession is over for SmithMidland… we have enough orders to be profitable through February 2016 and beyond; and we continue to be awarded new jobs every week.”

What I didn’t like about the shareholder letter was how there was no mention of revenue decline. In the 10-k, management states it was weather related. I compared their results to US Concrete and USCR made no weather related claims. However, USCR is in the ready-mix concrete business which is different than precast concrete. Still, if the weather was as bad as SMID claims it to be, USCR should’ve also been affected, but they were not. I’m not trying to say that management of SMID is making false claims, but I just don’t like it when management blames the weather for their problems. Now it should be noted that weather does play a huge role and SMID’s business is seasonal. Revenue drops off a bit in the winter months and picks up in spring and summer. Another fact to note was that backlog dramatically increased in the fourth quarter of FY2014 to 12.9 million compared to 10.6 the prior year, so that does lend credence to management’s claims that project have been delayed.

Catalyst for future Growth

Management’s plan to increase shareholder value includes:

-Lean manufacturing: Improve operational efficiency. This will mostly be felt in reduced COGS since manufacturing overhead are included in COGS. It has been more than 5 years since management embarked on their lean journey and I don’t know how much of the improvements were actually due to operation leverage vs product mix vs lean improvements.

- R&D efforts to speed the development of new products and improving existing products.

-Acquisitions: Not in the sense of acquiring another company for substantial amounts of cash, but more like acquiring another precast concrete plant which will broaden geographic reach. These are very small acquisition and usually do not have to be disclosed.

- 305-million-dollar five-year highway bill. This is probably the most important catalyst and having talked to SMID’s management, the company is already starting to benefit from new projects as a result of this bill and will mostly see most of the benefits in 2017 as projects really start to ramp up.

http://www.wsj.com/articles/congress-strikes-compromise-on-5-year-highway-bill-1449001406

Valuation

For a company with no growth or growth equal to the economy, a LTM PE of 10 is very fair. Geoteam wrote a great article on seekingalpha projecting a rolling forward 4 quarter EPS of $0.76 (http://seekingalpha.com/article/3688986-smith-midlands-blowout-quarter-unnoticed-market-price-target-7_00-7_50). With the passage of the highway bill, I think this is achievable and very fair. SMID is not really that great a company, but with an incoming catalyst I believe an investor can see capital appreciation of 50-100% within a year.