Business Description

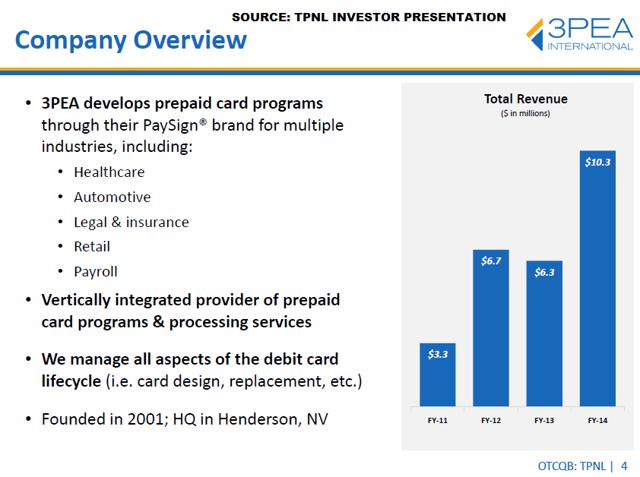

3pea International (TPNL) is an undervalued nanocap that is operating in the rapidly growing prepaid card industry. 3PEA International provides prepaid card programs and processing services for corporate, consumer and government applications. Prepaid card payment solutions are utilized as a means to increase customer loyalty, reduce administration costs and streamline operations. 3Pea’s prepaid debit card solutions are marketed under the PaySign ® brand. The company is a payment processor and debit card program manager, and derives revenue from all stages of the debit card lifecycle which I will get to in a second. Through their proprietary PaySign platform, the company provides a variety of services including transaction processing, cardholder enrollment, value loading, cardholder account management, reporting, and customer service.

Benefits of Prepaid Cards

A lot of people have probably used a prepaid card before. If you’ve been to a Starbucks, you know they offer “stars” each time you make a purchase with a Starbucks prepaid card which can later be used to get free drinks and stuff. If you have a Starbucks prepaid card, you are more likely to go to a Starbucks again rather than another coffee shops because you have an incentive to do so. Now of course, all of Starbuck’s competitors can offer their own rewards program and probably do. But that just means more business for companies like 3Pea.

Another benefit that most people probably don’t think about is that prepaid card programs can help businesses reduce costs. Prepaid cards can be used as a solution for recurring payments such as business payroll, incentives, and expenses. What this does is that it cuts the costs of processing payroll which is a lot more costly and lengthy process than loading a card with your employee’s wages which can be done within minutes. I could go on longer about the benefits but I will just list them here:

Employer Benefits

- Cost effective way to manage payroll

- Easy to implement solutions for your existing payroll services

- Reduce check, cash management and handling costs

- Reduce bank fees

- Reduce security risks involved with cash and check fraud

- Greatly reduce lost check replacement costs

- Payments to employees either instantly or within their own timeframe

- Issuing a prepaid card is often cheaper than sending international SWIFT or CHAPS payments

- Revenue earner

Employee Benefits

- Employees do not need to wait in queues to cash checks

- Replaces the need to cash check at high commission rates

- Employees will use fewer money orders

- Access to Internet purchases

- Employees have immediate access to funds on payday

- Saves time and money

- Employees can get account balance and transaction history via Internet, SMS or telephone IVR

- Share Money with secondary cardholders instantly at low cost via SMS

- Safer than carrying cash

- Benefit from safety features of Chip and PIN cards

- Anyone can obtain a card as no bank account or previous credit history is required

- Unbanked employees can use Prepaid Cards to make payments and obtain cash

It should also be mentioned that prepaid card has been gaining traction in Governments.

(https://www.prepaidfinancialservices.com/benefits/government-bodies/)

Below is a short video about prepaid cards.

https://www.youtube.com/watch?v=0ZLl7W1D6Gw

White paper about prepaid card.

(http://6d9d8ee3b24b98ab01c7-9b36caa56c1219a43771b85c9c534202.r82.cf2.rackcdn.com/storecard_whitepaper.pdf)

Prepaid Card Industry

“According to the 2013 Federal Reserve Payments Study, growth in prepaid card payments increased at the fastest rate from 2009 to 2012 when compared to credit, debit, ACH and checks. In this period prepaid debit transactions grew at a rate of 15.8% annually, reaching 9.2 billion transactions in 2012. Transactions on prepaid cards have a compounded annual growth rate (CAGR) of 30.7% in the years 2003-2012, and a CAGR of 15.8% during the 2009 to 2012 time frame.”

(TPNL 2014 10-K)

The prepaid card industry is a very fast growing industry, not just domestically but also globally as well. According to Mastercard, “The prepaid opportunity continues to grow around the world and is expected to reach US$822 billion by 2017. The popularity of prepaid is driven by its unique and practical ability to solve for almost any payment need. It democratizes electronic payments for those outside the traditional banking system and provides a transparent, cost-effective alternative to cash and checks for both governments and businesses. Prepaid also serves the needs of banked consumers who find it an ideal payment tool for segmenting spend such as travel and online shopping.”

(https://www.partnersinprepaid.com/pdf/a-look-at-the-potential-for-global-prepaid-growth-by-2017.pdf)

Business Model

The company has prepaid card programs in place with many Fortune 100 and Fortune 500 companies. Source plasma donors make up a large portion of their revenue. In slide 9, the company said that they have a strong presence in healthcare market which is saying that they have gained the most traction in this market and revenues are concentrated here. You easily find out who their customers are by looking at their customer list in their website which includes large pharmaceutical companies like Allergan and Amgen.

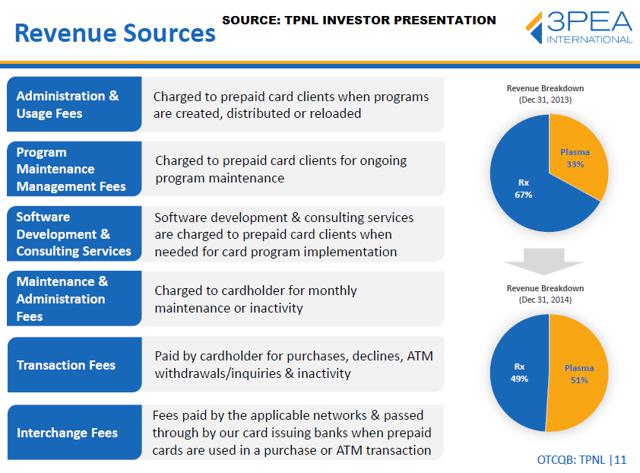

As you can see in this slide, the company has several sources of recurring revenues. The program maintenance and management fees are needed once in a while but I suspect it’s not that much. The bulk of recurring revenue is from transaction fees and interchange fees. (They are not exactly recurring, but it's close enough). The number of transactions will go down in a recession so you should keep in mind that the company is not recession resistant.

Below is a site about source plasma donation which readers should read since this is where the bulk of TPNL’s revenue come from. It should be noted that there is no customer concentration risk even though the company is concentrated in the healthcare industry. Management is feeling very confident that they can increase the number of plasma centers in FY 2016. They currently have 80 plasma centers using their Paysign Prepaid cards. The number of plasma centers in the United States is around ~450 so there are still room to expand.

http://www.fwdailynews.com/news/latest/aboite/rise-of-blood-plasma-centers-borne-by-medical-therapies/article_134e9da5-61ef-598b-91fd-10ab01a823ce.html

(https://www.bloodsource.org/Donate/Source-Plasma)

I also came across an article with a negative view on plasma donations. It is possible that TPNL’s revenue will decrease if regulations are made such that plasma donors are only allowed to donate fortnightly instead of twice a week which is currently the case in the US

(http://www.theatlantic.com/health/archive/2014/05/blood-money-the-twisted-business-of-donating-plasma/362012/)

Financials

| |

2011 |

2012 |

2013 |

2014 |

2015E |

2016E |

2017E |

| Revenue |

3300 |

6700 |

6307 |

10293 |

8000 |

10000 |

12000 |

| COGS |

2430 |

5305 |

4103 |

4655 |

3600 |

3600 |

4000 |

| Gross Profit |

870 |

1395 |

2204 |

5638 |

4400 |

6400 |

8000 |

| Gross Margin |

26% |

21% |

35% |

55% |

55% |

64% |

67% |

| Operating Ex |

591 |

820 |

1553 |

2887 |

4200 |

4600 |

5000 |

| Operating Income |

279 |

575 |

651 |

2751 |

200 |

1800 |

3000 |

| Operating Margin |

8% |

9% |

10% |

27% |

3% |

18% |

25% |

| Others |

63 |

62 |

59 |

141 |

0 |

0 |

0 |

| Tax |

0 |

0 |

0 |

0 |

0 |

0 |

1050 |

| Net Income |

216 |

513 |

592 |

2610 |

200 |

1800 |

1950 |

| Diluted Shares |

35248 |

39476 |

42395 |

42405 |

42405 |

47000 |

47000 |

| EPS |

0.01 |

0.01 |

0.01 |

0.06 |

0.00 |

0.04 |

0.04 |

(Adjusted for one time expenses)

As we can see from the financials, 3Pea started off in 2011 with about 3.4 million in revenue and grew to over 8 million in 2014. For 2015 I adjusted for a one time legal settlement and assumed Q4 15 will be similar to Q3 15. Gross margins will increase as revenues increase as they gain the benefit of leverage on their PaySign platform. While the company has benefitted from operating leverage from 2011 to 2014, the company decided to expand to Europe in 2015 which greatly increased their operating expense. Management said that it will take a while before Europe starts contributing revenue as there are regulatory barriers in starting any kind of prepaid card or payment processing business. However, 2017 should be when Europe starts contributing meaningful amount of revenue. The company also plans to expand into the automotive market, but progress has been slow and I wouldn't expect much revenue from automotive until late 2016. In the meantime, the bulk of revenue increase in the next 2-3 years should come from increasing the number of plasma centers and pharmaceuticals they can sign on. I believe their operating expense will continue to increase but at a lower rate. If my above projections are achievable, EPS should be 0.04 by 2017. According to management, their NOL carryforward should run out in a year or two so I assume they start paying tax in 2017. With a PE of 15-20, the PPS should be $0.60 to $0.80 which is about 4x the current price. This is in line with the average P/S ratio in this industry which is about a 4-5x compared to TPNL's current P/S of 1. Executive compensations are modest and insiders own over 70% of the company so I believe they are properly aligned with shareholders and want to see their expansion successfully executed.

It should be noted that revenues and earnings are very lumpy as can be seen in the quarterly revenues and EBIT. Q4 of 2014 was huge but was not sustainable, but management expects to have one of those quarters once in a while.

|

|

|

2011

|

2012

|

2013

|

2014

|

2015

|

|

Q1

|

Revenue

|

938

|

1484

|

2111

|

2407

|

1598

|

|

|

EBIT

|

22

|

92

|

241

|

-64

|

-426

|

|

Q2

|

Revenue

|

665

|

2549

|

1204

|

1233

|

2311

|

|

|

EBIT

|

76

|

155

|

310

|

-103

|

469

|

|

Q3

|

Revenue

|

278

|

622

|

1061

|

1707

|

2034

|

|

|

EBIT

|

47

|

107

|

-77

|

47

|

241

|

|

Q4

|

Revenue

|

1419

|

2045

|

1931

|

4946

|

|

|

|

EBIT

|

134

|

221

|

177

|

2871

|

|

Why the Opportunity Exists

If you look at the chart of TPNL, you will notice that it ran up from around $0.3 to about a dollar and then crashed to its current price of $0.23. This is due to a variety of reasons and I believe the crash is a bit overdone. First of all, the reason for the run up was partly due to a seekingalpha article by Dallas Salazar but mainly due to the blowout Q4 14 quarter that was not sustainable. The crash during the second half of 2015 was simply due to the fact that their Q4 14 quarter was not sustainable and a lawsuit that was settled this in Q3 2015 and the resignation of their CFO.

Although the resignation of a CFO is usually a red flag, I considered the resignation of Arthur de Joya a good thing for TPNL because they are now no longer associated with him. Arthur de Joya and his firm has been associated with microcap schemes in the mining sector accoding to a SEC release so I suspect that he was forced to resign due to disagreements with management of TPNL. (http://www.sec.gov/news/pressrelease/2015-9.html).

As for the lawsuit, you can read all about it here: https://www.unitedstatescourts.org/federal/cand/290007/

It is hard to tell who was in the wrong here, but according to 3Pea management, they decided to settle because they thought it was better than spending money on litigation fees. In anycase, this event is behind them and the stock has already taken the hit.

Conclusion

3pea is a rapidly growing company in the prepaid card industry which will benefit from operating leverage if they get more plasma centers to use their Paysign card. Expansion to the European and automotive markets are optionality at this point. At the current price of $0.23 and with a P/S of ~1, there is minimal downside.

DISCLAIMER: GeoInvesting has no affiliation with the author of this report in any way and is not endorsing his research, nor has GeoInvesting vetted this information in any way. The GeoTeam does not attest to the accuracy of the information contained in this report and always urges investors to conduct their own due diligence. The GeoTeam has received no compensation for the dissemination of this report. The GeoTeam may or may not have a position in any stocks mentioned in this article prior to its publication.