Tss Inc (OOTC:TSSI) ($2.75, $60.5M market cap), announced Q2 2024 results:

- Sales of $12.2 million vs $14.5 million in the prior year

- Reseller revenue of $4.9 million vs $10.6 million in the prior year

- System integration and facility management revenue of $7.2 million vs $3.3 million (higher margin)

- EPS of $0.06 vs a EPS of $0.01 in the prior year

During Q2, we made a significant investment in our production capacity, which came online at the beginning of June,” said Darryll Dewan, CEO of TSS. “This expansion, compounded with process improvements, has significantly increased our volume capacity for rack integration and decreased the cycle time to complete each rack within our existing facility. The expansion was driven primarily by the surge in demand for server rack builds related to generative AI, as the AI market expands as a whole.”

“To be clear, the volume ramp we've been anticipating is now underway. Our OEM customers have robust pipelines and we are seeing their deals beginning to close including one significant program the was started in the second quarter and will more dramatically impact the third quarter. We believe our Q2 performance was a harbinger of results to come. Our strategic inclusion in key customer programs signals a bright future as OEM pipelines materialize.”

We highly encourage you to read the conference call transcript to hear how positive the management team sounds and the encouraging outlook they provide.

Here is a small excerpt:

“The pipeline deals of our OEM partners are large and we anticipate some variabilities as the market adapts to rapid technological changes. But make no mistake, we're witnessing the dawn of a transformative era in our industry and TSS is at the forefront. This is not just exciting, it's validating. It confirms our strategy, our investments, and more importantly, the tireless efforts of our exceptional team. I'm proud of this team and as we navigate this dynamic landscape, we're just not riding the wave of AI revolution, we're helping to propel it forward.”

—--

More TSSI highlights and breakdown:

Here is what you need to know: after years of stagnant growth in systems integration revenue, the company finally delivered strong revenue growth in this higher-margin business segment, which has primarily built and delivered racks for traditional (enterprise) data centers in a building. This revenue was up 113% to $5 million and carried gross margins of 43% for the quarter.

The company reported earnings per share of 6 cents versus Q2 2023 EPS of 1 cent . These numbers were clear quarterly records for the company’s systems integration business. Overall gross margins were 36% versus 22% last year.

The growth in the systems integration business was fueled by the company’s backlog of AI integration work beginning to materialize in June.

Overall Q2 sales came in at $12.2 million versus $14.5 million . Investors who are not familiar with TSSI will not understand that the headline number doesn’t tell the whole story.

Remember, the reseller/procurement business can be lumpy. This is basically revenue generated from its OEM customer (Dell), asking TSSI to procure hardware/software that Dell does not sell, but its customers want. It’s a low gross margin business (we estimate around 1 0% ), but strengthens TSSI relationship with OEMs. It also opens the door for TSSI to develop closer relationships with customers, so that it can possibly perform higher margin system integration services for them. One thing to keep in mind is that even though this business is a low gross margin business, it’s a high revenue business and a good deal of the gross margin flows right to the bottom line. This quarter, the segment produced income of $600,000 .

Investors who have been following TSSI understand that the near to midterm growth story and the impetus for valuation multiple expansion to occur revolves around its ability to grow its systems integration business. This is pure data center work. Up until Q2, there has been no dramatic growth in rack integration. All we had was a very lumpy revenue stream in the reseller business here and there. It’s tough to value a business on that type of revenue stream.

Now, recall that in the last few earnings calls, management has said that they have positioned the company to be able to grow the rack integration business by 10x . We are finally getting a glimpse of the type of profitability the company can experience as it grows the system integration business. In fact, on the earnings call, I asked the CEO if efficiencies will improve as the company scales. He very confidently said yes.

It’s going to be interesting to see how earnings per share will play out as the company gets closer to the 10x capacity goal. Prior to this quarter, I had estimated that EPS could reach at least $0.20 per at full capacit y. Now, I think that’s potentially conservative. Regardless, it looks like it won't be long until the company is approaching an annual EPS run-rate of $1.00 per share.

I’ll let you decide what P/E to throw on that.

There was another very important takeaway from the earnings call. Management already indicated that they’re going to need more capacity heading into 2025. So, that’s giving us a clue that our $0.20+ EPS assumption could be right around the corner and that 2025 should be a banner year for the company. To accommodate for this growth, management said that it’s eyeing up moving into a new facility to meet demand. Why is this important?

It’s been pretty much assumed that the company's current facility is “dedicated” to its “large OEM customer”, partly because the OEM has actually invested money into the facility. So, we think moving into another facility will allow TSSI to more aggressively expand outside its large OEM relationship and reduce that very large customer concentration risk.

I should add that we think that the company now meets the minimum shareholder equity requirement for an up-listing from the OTC.

Longer-term, two other sources of revenue could help add to and diversify TSSI’s growth.

Modular Data Centers

Modular data centers are built at a facility and delivered to the customer’s location, typically outside. This option is easier for a company to plan/expand than with an enclosed data center. Traditional data centers that are enclosed require more pre-planning in terms of deciding how big of a building to build to accommodate imprecise expansion needs over time. Modular centers are lighter, customizable, smaller, quicker to deploy, require less equipment, can be more energy efficient, and can be located closer to the processing “edge.”

The company spent some time on the Q2 2024 call talking about how this opportunity is starting to shape up as well they can go after

“In our modular data center business, while we've seen year-over-year improvement, we're now engaged in promising discussions with prospective customers. Our focus is on building a solid backlog to fuel revenue growth in 2025 and beyond.

We're observing increased refresh activities in existing installations, though new builds are taking longer, particularly for AI solutions due to high GPU demand and anticipated technology releases. In the long term, we see potential synergy between AI and modular form factors, especially for use cases like autonomous vehicles and other time-sensitive applications in underserved areas.”

Facilities Management

This segment provides maintenance services and hasn’t been a consistently big driver of revenue, although it has grown this year, including 44% in Q2 to $2.3 million. This is an area of the business I need to dig into because it carries gross margins of over 70% . I’m not quite sure how the revenue moves with the rest of the business, but it currently appears to be only tied to modular business which is why the company wants to step up plans to grow the modular business. So, my original assumption that this revenue would automatically go up with the system integration business was incorrect, although I would not rule out management seeking out ways to expand that business to its system integration business.

What we now know is that getting the modular business growing could be extremely additive to our quarterly EPS run-rate of $0.20+.

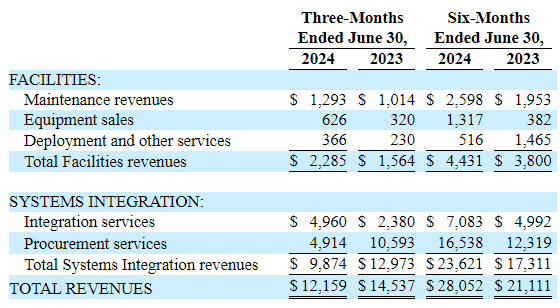

Here’s a breakout of the revenue in all of the companies segments outlined in the Q2 filing :

The gross margin breakout is provided in the management, discussion and analysis section of the Q2 filing.

Caveats:

- Revenue, especially the reseller business will be lumpy. For example, on the Q2 call, management indicated that Q3 will come in at $50 million.

- How will the company pay for purchasing /building/leasing another facility to expand in 2025?