In our April 24, 2019 email, we mentioned that we had a chance to interview $STXS management and that our main takeaway was that the company is now entering the next phase of its turnaround process and looks to double revenue over the next five years. The company was not focused on growing revenues during the first phase of its turnaround. The company is now at a point where it does not need to raise funds going forward.

More insights from our interview:

Overview:

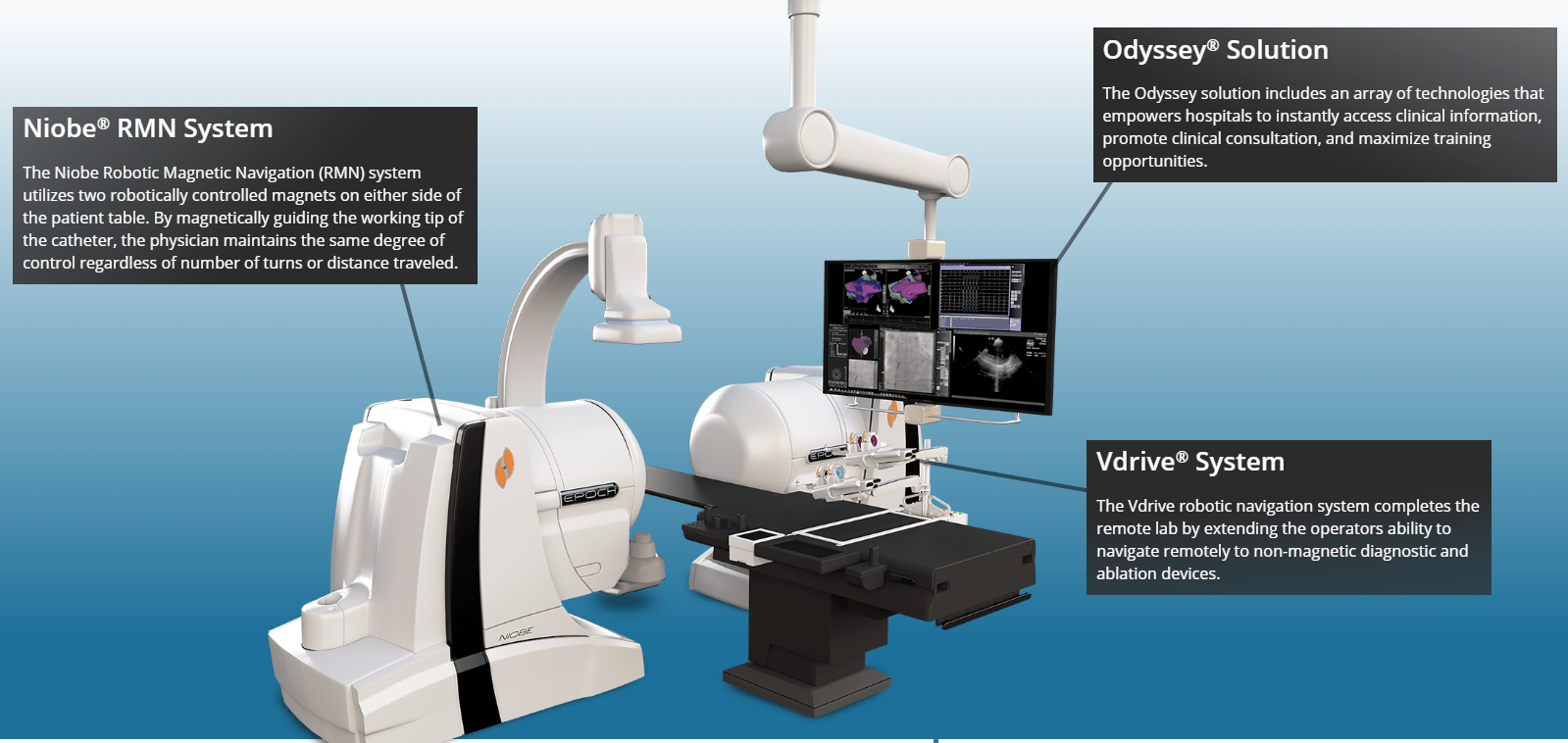

The company is the global leader in Endovascular robotics. Its main product is the Niobe Robotic Magnetic Navigation system. Below is the description of the system and a visual from the Company’s website:

The Stereotaxis remote magnetic navigation system utilizes two permanent magnets mounted on pivoting arms that are enclosed within a stationary housing, with one magnet on either side of the patient table. During a procedure, the physician guides the catheter movement by simply moving a computer mouse from a room adjacent to the patient but outside of the x-ray fluoroscopy field.

By magnetically controlling the working tip of the interventional device, the physician maintains the same degree of control regardless of number of turns or distance traveled. This provides the ability to safely access anatomic areas unreachable by other approaches.

The system has two recurring revenue streams with the Odyssey Solution and the Vdrive system, both of which work in conjunction with the Niobe system.

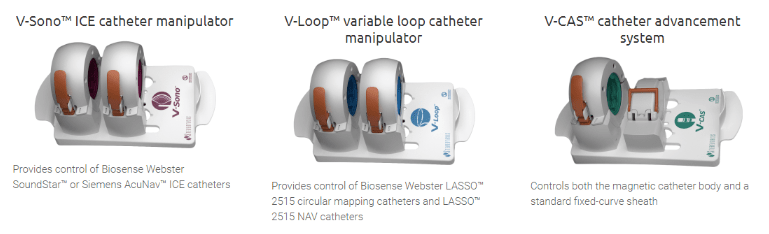

The Odyssey solution aggregates and integrates a vast amount of clinical lab information into one large screen and a single mouse and keyboard control, as shown above. The Vdrive System completes the remote lab by extending the operator’s ability to navigate remotely to non-magnetic diagnostic and ablation devices. Below are the 3 components of the Vdrive System:

Early History:

The company went public in 2004 and was spending a lot of money on marketing its product, however, the product did not meet industry expectations at first. Management had told us that the speed of the system was slightly slower than expectations. Furthermore, the company was spending too much capital on ancillary products that it did not have a competitive advantage in, instead of investing in its core robotic technology platform. Finally, management stated that the company did not offer support services to physicians using the product.

The company began growing revenue but was incurring losses as it progressed forward. In 2014, the company brought in Martin Stammer as new CFO to help relieve itself of the financial handcuffs its operating losses had caused. They were not spending much on R&D during those years and had to issue preferred stock to help clean up their debt.

From 2016 to 2018, the company finalized its balance sheet clean up (the company currently has no debt) and begun its R&D efforts once again. And as we mentioned above, the Company is now in growth mode, looking to drive the top and bottom line moving forward (we discuss in more detail below). In 2017, the company hired CEO David Fischel to help with its growth.

Market Opportunity:

The endovascular market is a $4+ billion market growing at 10 to 15% annually. The Company claims that there is currently no competition in the market they serve of robotic treatment for cardiac arrhythmias (robotically controlling catheters). However, they do see competition in the ancillary products they sell. We were told that there are roughly 800,000 procedures a year and STXS currently only captures about 1% of the market.

Safety and Efficiency:

Most procedures are still done manually. The Niobe system is best used in complex procedures. The clinical data supports that Niobe system is safer and more efficient than manual procedures. We will guide you to the Company’s site for a full clinical data summary and it’s worth noting that the adverse effects from surgeries are under 1% with Niobe, versus ~10% manually.

Growth Mode:

The company is now focused on growth. Management stated to us that they believe they can double revenue in the next several years from its current installed base. After focusing on its installed base, they also believe there are other opportunities that can propel growth. While they did not specify, we think one avenue could be a system replacement cycle. The original systems were from 2003/2004 and most labs look to replace equipment on average every 10 years.

In the interview, management hinted at the excitement around its latest innovations but has not shared the details publicly yet. The plan was to do so at the Annual Heart Rhythm Scientific Conference to be held on May 8 to 11th, 2019. Our May 9th 2019 email gives more color on the innovations that have the company so excited. Below are the highlights from the company’s press release:

-

Innovative robotic surgery system, Stereotaxis Genesis™ RMN, enriches robotic magnetic navigation with increased efficiency, reduced size, and enhanced lab experience

-

Genesis RMN System to be available in combination with Stereotaxis Imaging Model S, a next-generation x-ray system offered as part of a complete robotic electrophysiology lab solution

-

Combined technologies greatly enhance the accessibility and affordability of robotics in electrophysiology

Possible Merger/Acquisition:

When we asked about other procedures that were being done robotically and how those companies fared, he mentioned two that were acquired. Medtronic (NYSE:MDT) acquired Mazor in December 2018. Mazor was a leader in robotic spine surgery. And, in 2013, Stryker acquired Mako, which was a robotic surgery platform for knee and hip replacements.

Mako shareholders received an 86% premium, while Mazor saw a 10% premium, but it was one of the largest orthopedic deals in 2018, valued at $1.7 billion.

We believe it is worth monitoring the company’s strategic partners as possible suitors in acquiring STXS. Biosense Webster and Philips Medizin Systems are its closest partners, both of which are private companies.

Caveats:

- Fully diluted share count is close to 100 million, well above the range we typically look for

- Unclear why only 1% of the treatment of abnormal heart rhythms are done robotically

- Execution risk remains a concern