Once again, the GeoTeam has uncovered an information arbitrage opportunity (bullish Form 10-Q commentary not included in the press release) in Smith-Midland Corporation (SMID). SMID invents, develops, manufactures, markets, leases, licenses, sells, and installs an array of precast concrete products for use primarily in the construction, highway, utilities, and farming industries in the United States.

On 10/26/15 we alerted premium members that we were taking a pre-earnings position in SMID, when the stock was trading at $2.95. We had been tracking the company for several years and Q2 2015 commentary piqued our interest when management indicated the company was ready to embark on a new period of growth.

On November 2, 2015, we published our research note detailing our reasons for optimism. We followed up on November 3, 2015, by coding SMID as our newest GeoBargain.

On November 12, 2015, an hour before the close, SMID reported blow-out Q3 2015 results that exceeded even our expectations.

- Total revenue of $10.4 million for three months ended September 30, 2015 was $4.4 million or 74.1% more than revenue generated in Q3 2014.

- Net income of $1,152,056 for Q3 2015, compared to net income of $112,490 for the same period in 2014, a 1,000%+ increase.

- Basic and diluted earnings per share were $0.24 and $0.23, respectively, for Q3 2015 vs. $0.02 basic and diluted earnings per share for Q3 2014.

Management’s commentary in the press release follows:

Rodney Smith, Chairman and CEO, stated, “The management and associates at the Company are extremely proud to be able to present the financial results for the third quarter of 2015, one of the best quarters on record for Smith-Midland. All of the associates of the Company have been instrumental in making this quarter so successful.

“Smith-Midland is five years into our lean journey and under President Ashley Smith’s leadership, we have made significant improvements such as highly improved production planning, many improvements in employee efficiency and significant product quality improvement, and the journey continues.

“One of our top priorities for the remainder of 2015 and also in 2016 is continuous New Product Development through our Smith-Midland Research and Development team. Arguably one of the best research and development teams in the Precast Industry, we are currently developing several new products which include Non Bolted Highway Parapet, Slenderwall III and a Highway Crash Cushion using SoftSound. Innovative product development has always been the key to the future for Smith-Midland from a sales and profitability standpoint and to maintain our competitive edge for the Company and our international family of Easi-Set licensees.”

In addition, the company provided bullish commentary in the Form 10Q MD&A that was not included in the press release . Following are excerpts from the MD&A regarding SMID’s revenue segments. We encourage you to read the entire filing here :

Soundwall sales - $871,711 – “Management expects that soundwall revenue should remain relatively strong during the remainder of the year and into 2016.”

Archetectural Panel sales - $412,176 – “While the construction economy has been trending up for the past 12 months, the volume of architectural projects continues to be less than that of other wall panel projects and also while not as competitive as last year, are still the most competitive bids.”

Slenderwall sales - $1,005,492 – “The two new Slenderwall projects that started in the second quarter of 2015 resulted in increased revenue for the nine months ended September 30, 2015, when compared to the same period in 2014. Slenderwall sales should remain strong throughout 2015 and into the 2016.”

Barrier sales – $617,101- “During the three and nine month periods ended September 30, 2015, we have received several medium size barrier orders which have not shipped as of yet, however, these orders are expected to ship in the fourth quarter of 2015 which should significantly increase barrier sales in the fourth quarter of 2015 over the fourth quarter of 2014.”

Easi-Set® and Easi-Span® Building Sales – $692,169 - “ Management believes that the Company may see a slight increase in building sales during the fourth quarter of 2015 over the fourth quarter of the prior year based on its current building backlog , but customer installation demands will control when final installation will be made.”

Miscellaneous Sales – $320,784 - “Management believes that miscellaneous sales will increase slightly during the fourth quarter of 2015 over the fourth quarter of the prior year.”

Royalty Income – $425,831 - “Management believes that royalties will continue to increase moderately over the remainder of 2015 as a result of the continuing improvement in the construction industry.”

Barrier Rentals – $3,137,761 - “The increase resulted primarily from two large rental contracts awarded the Company for two short-term barrier rental projects in Washington DC and Philadelphia, PA for the month of September 30, 2015. These projects were related to the Papal visit, and this type of special event may not be repeated in the near future or in the year 2016. The Company will endeavor to find this type of project in the future, but projects like this one are particularly few and far between. While the increase in revenue for barrier due to the special project was significant, regular barrier rentals excluding the special projects revenue were up significantly for both the three and nine months ended September 30, 2015 when compared to the same periods in 2014. The increase was due to the continued increase in the construction industry and particularly in highway infrastructure spending.”

Shipping and Installation – $1,223,599 - “With the shipping revenue generated by the current projects shipping and the new ones beginning to ship in November, shipping and installation revenue should increase in the fourth quarter of 2015 from the fourth quarter of the prior year. For the full year 2015, the Company will continue to be behind 2014 revenues based on the installation and shipping activities discussed above.”

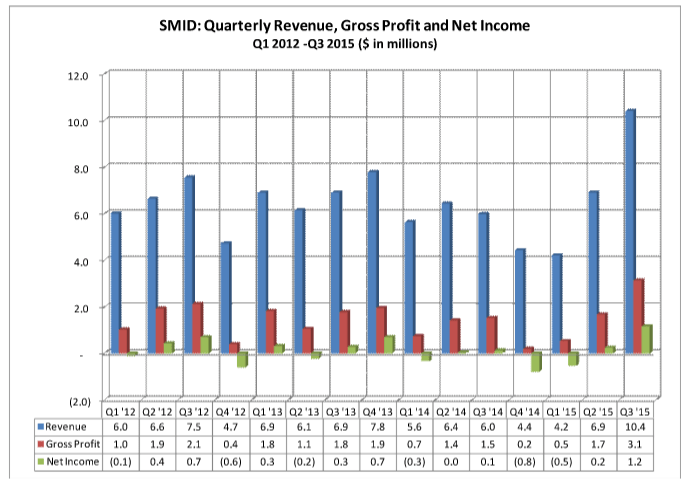

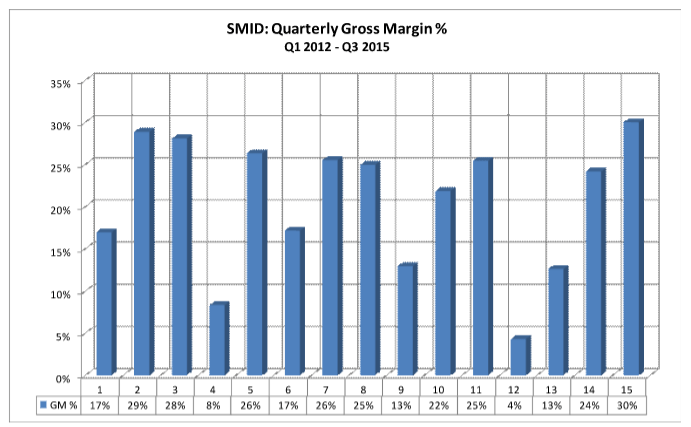

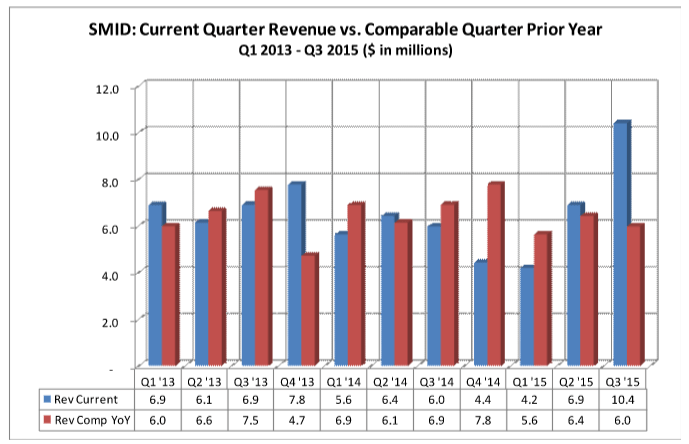

The following quarterly charts give perspective on how far SMID has come since Q1 2012 and an indication of how much momentum the business currently has. Revenues, gross profits and net income are all strongly headed in the right direction. Also, quarterly revenue comps vs. the same period in the prior year are strong. Barring an unusually severe winter we expect SMID’s business momentum to continue well into 2016.

Valuation

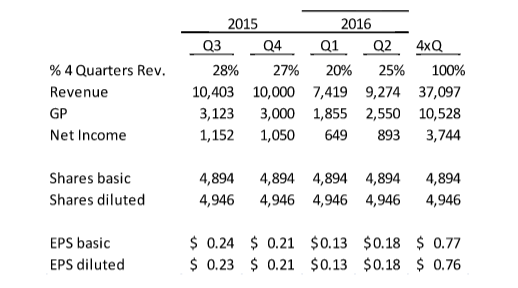

We believe SMID should be valued between $7.00 and $7.50 per share based on two valuation approaches:

- Projected operating results for four quarters with Q3 2015 as the base and estimating the next three quarters using historic quarterly revenue distribution % for the last four years. Q1 is the weakest quarter seasonally due to winter weather.

Applying a 10x multiple to estimated diluted EPS of $.76 implies a $7.60 value.

- Competitor USCR has a Price/Sales ratio of .95. Applying that ratio to our four quarter revenue estimate of $37.1 million yields a $7.13 value.

Next Steps

We hope to interview management in the near future to determine how much of the recent momentum will carry through to future quarters. Given SMID’s recent performance and the seemingly inevitable increase in infrastructure spending on highways and bridges in the U.S., we are confident that Q3 2015 was not a one-off event. We anticipate SMID’s recent momentum will continue in the near term.