On June 11, 2018 we disclosed that we took an initial position in Iec Electronics Corp. (NYSEAMEX:IEC). On January 14 2019, we looked to increase our position size in the stock.

We believe IEC is building a leading product offering, led by a proven CEO. Although we don’t believe shares are incredibly cheap based on trailing financials, we think changes management made since 2015 positions the company to consistently grow revenue, with earnings growing at a faster pace than sales. Like Cas Medical Systems, Inc. (NASDAQ:CASM) and some other stocks we initially buy that don’t look cheap on paper, IEC is a bet on management.

IEC Electronics is a 52-year-old company that describes itself as a:

“…premier provider of electronic manufacturing services (“EMS”) to advanced technology companies that produce life-saving and mission critical products for the medical, industrial, aerospace and defense sectors. We specialize in delivering technical solutions for the custom manufacturing, product configuration, and verification testing of highly engineered complex products that require a sophisticated level of manufacturing to ensure quality and performance. Within the EMS sector, we have unique capabilities which allow our customers to rely on us to solve their complex challenges, minimize their supply chain risk and deliver full system solutions for their supply chain.”

Electronic manufacturing services are:

“…provided by companies that design, assemble, produce, and test electronic components and printed circuit board (PCB) assemblies for original equipment manufacturers (OEMs). EMS companies may provide a variety of manufacturing services, including design, assembly, and testing. EMS companies may be contracted at various points in the manufacturing process. Some companies require only a design file from the customer before proceeding to develop the product, source the components from a trusted distributor, and assemble and test the product.”

IEC has built a one stop shop for its customers and actually benefits from keeping manufacturing activities in-house and in the U.S.

In our opinion, the steps IEC has taken over the last three years should help it command a higher multiple than many players its peer group, due to its focus of targeting less cyclical and less predictable market segments than its peers. You can view a virtual presentation given by the CEO at the LD Micro Conference (from which we have pulled some slides) here.

Our reasons for tracking the company are:

- Proven CEO

- Sticky customer base

- Reaching a growth inflection point

- We see upside to analyst estimates based on information arbitrage

Quick Facts

- Head Quarters: New York

- CEO: Jeffrey Schlarbaum

- Number of Employees: 689

- Price: $6.95

- Insider Ownership: 2.3%

- Trailing 12 month P/E of 46.3

- P/E of 12.1 on analyst EPS estimates of $0.57 for fiscal 2019

- P/E of 6.7 on analyst EPS estimates of $1.03 for fiscal 2020

- Shares Outstanding: 10.2 million

- Market Cap: 71.2 million

- Publicly Traded EMS Companies Smtc Corporation (NASDAQ:SMTX), Key Tronic Corporation (NASDAQ:KTCC), Celestica, Inc. (NYSE:CLS), Sigmatron International, Inc. (NASDAQ:SGMA), Jabil Inc. (NYSE:JBL), Kimball Electronics, Inc.(KE),Plexus Corp. (NASDAQ:PLXS)

Reasons For Tracking

Proven CEO

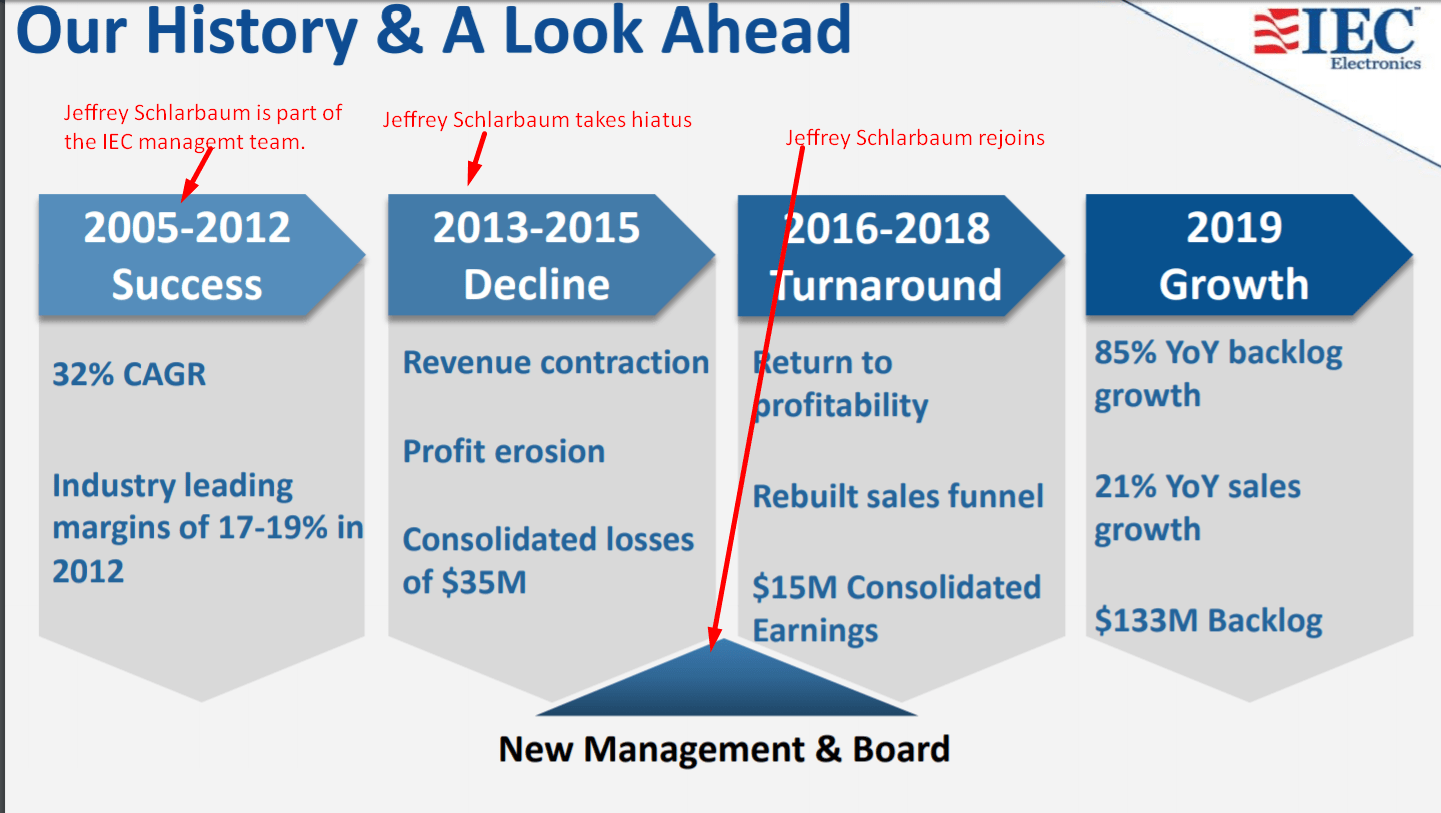

As a reminder, we met Jeffrey Schlarbaum, the CEO of IEC, at the LD Microcap Conference in early June 2018 and connected with his vision for growth. Jeffrey Schlarbaum was appointed as CEO in February 2015 and between April 2004 and February 2013 he was President of IEC.

As President, he was instrumental in pivoting the company away from targeting cyclical consumer, lower margin markets, like gaming systems, to stickier markets. His initiatives led to IEC experiencing several years of consistent growth. During this stretch, the stock went from around $1.00 to a peak of around $8.00 in 2011.

Schlarbaum left the company in February 2013 over a CEO succession dispute and disagreement with the direction management wanted to take the company. During this hiatus, the company made several missteps, including a failed acquisition strategy and loss of key customer segment focus. During his absence, IEC shares declined from around $6.00 to hit a low of ~$3.00 in 2013.

He then rejoined the company in February 2015, with the stock trading at ~$4.50, and has been doing a great job of rebuilding the business to recapture some of the operational benefits that it once possessed by implementing the same strategy that led to growth when Schlarbaum was President.

This slide from a recent investor presentation says it all:

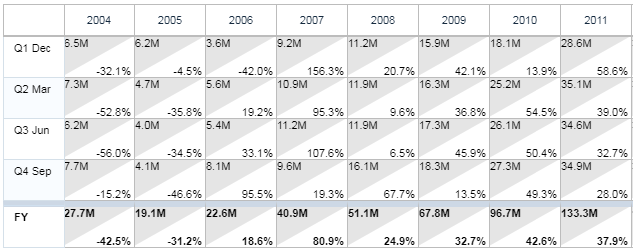

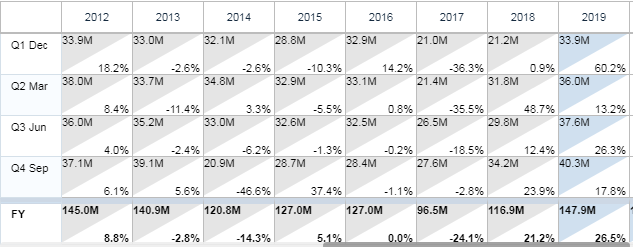

Here is a comprehensive look at the company’s sales history since 2004:

You can easily see the growth that the company experienced under Jeffrey Schlarbaum’s first run as CEO from 2004 to 2013, as well as the subsequent dip after his departure and the resurgence upon his arrival again. During his first tour of duty, EPS was solidly profitable, with EPS reaching $0.78 in 2012, before incurring losses upon his departure.

Sticky Customers

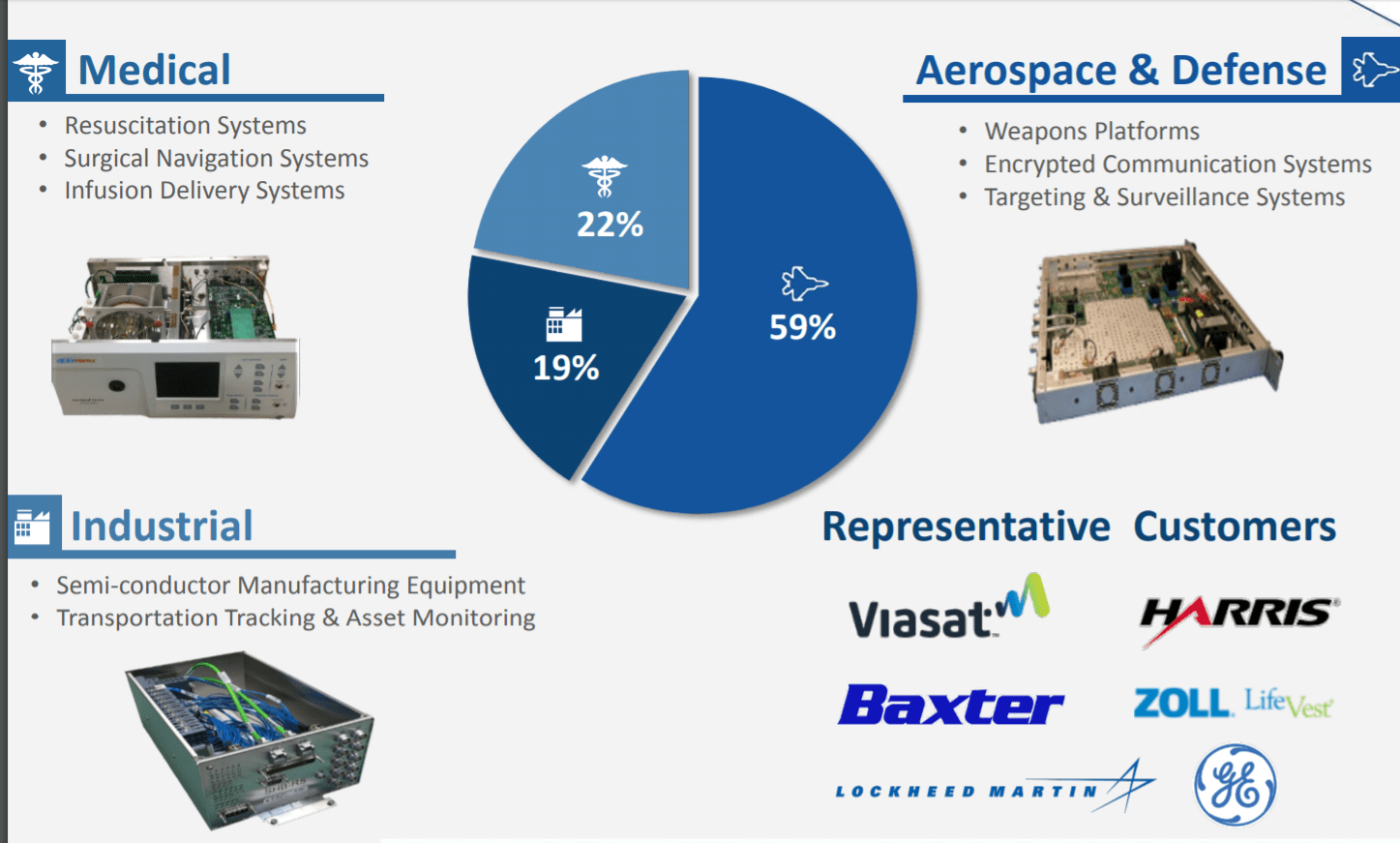

The company has made steady gains by focusing on serving less cyclical customers in high growth markets with good visibility and high switching costs (sticky customers). Specifically, IEC is targeting highly regulated firms that require highly engineered products that are complex, mission critical and save lives:

Part of IEC’s stickiness (compared to some of the competition) comes from offering its customers a complete solution by:

- Working closely with them to develop products to meet customer needs

- Focusing on a few key markets, as opposed to many markets

- This helps the company know its customers better than competitors using a “shotgun” market approach

- Keeping critical manufacturing activities in-house, allowing IEC to maintain high quality standards, deliver product to its customers quickly and react quickly to changes/disruptions in its markets

- Providing pricing flexibility that comes from keeping manufacturing in-house

- Providing in-house product testing

Who knew that one day a company that manufactures its products in the U.S., as opposed to outsourcing to China, would again be considered a good thing?

The customers that IEC serves take comfort from this, especially because they are concerned about protecting intellectual property. In fact, the Trump tariff wars could bring customers that have been outsourcing to China to IEC’s door step.

An added benefit to these efforts is that, at 12%, IEC commands higher gross margins than can be typical of lower tier EMS companies (whose gross margins are often less than 10%). In the end, customers are willing to pay a premium for the complete offering that IEC delivers.

Growth Inflection Point

IEC has reported 3 quarters in a row of positive sales growth, while maintaining profitability. Even though they are maintaining profitability, they have yet to show consistent YOY EPS growth, which has been one of our concerns.

- Q4 2018 sales of $34.2 million vs $27.6 million in the prior year; $0.13 vs. $0.07

- Q3 2018 sales of $29.8 million vs $26.5 million in the prior year; $0.02 vs. $0.08 (EPS down to supply constraint issues)

- Q2 2018 sales of $31.8 million vs $21.4 million in the prior year; $0.15 vs. -$0.05

As indicated in the company’s Q4 conference call, it looks like IEC has clearly reached a positive inflection point and is ready to enter a new phase in its growth story.

“Jeffrey T. Schlarbaum, President and CEO of IEC Electronics commented, “With the close of fiscal 2018, we believe our Company has fully exited the turnaround phase and is well positioned to drive sustained growth. Our strong fourth quarter performance was characterized by increased revenues levels, which have not been seen in 5 years, as well as strong backlog growth. Revenue and volume growth are being driven in large part by our ability to win new projects from existing customers as they recognize IEC’s value as a reliable and consistent manufacturing partner and discover the breadth of our diverse, vertically integrated capabilities.”

With an $18 billion market opportunity, IEC’s top line growth opportunity is very compelling. However, we are more excited about the earnings leverage IEC can achieve as it grows revenue for the following reasons:

- IEC still has a long way to go to reach top tier industry gross margins of 18%

- Many of the upfront costs associated with onboarding new clients over the past couple of years will not be present moving forward

- The company is moving into a new and more efficient manufacturing facility

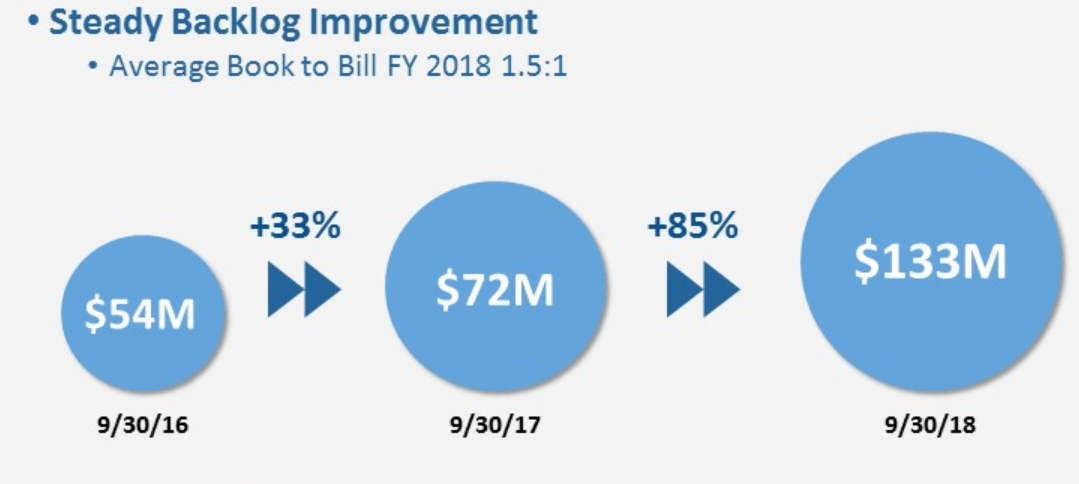

- Steady backlog improvement

Analyst estimates confirm that IEC is at a growth inflection point, with EPS estimates slated to be $0.56 and $1.03 for fiscal 2019 and 2020, respectively (FY ends in September).

Information Arbitrage: Upside to Analyst Estimates

While current estimates indicate nice growth for 2019 and 2020, by applying a P/E of 10 to 15 on 2019 EPS estimates of $0.57, the stock is already trading at the low end of a fairly priced range of $6.00 to $9.00.

However, 3 factors could lead to shares trading above this range:

- As we pointed out on November 28, 2018, analyst 2019 estimates might be conservative, as they don’t seem to take into account the guidance the company gave on its Q4 earnings conference call

- We stated: “Management's comments regarding the absence of its typical seasonal decline from Q4 to Q1 indicate a possible nice beat for Q1 2019. Current analyst estimates for Q1 are $28.6 million for revenues and $0.04 in EPS.” This compares to sales and EPS of for Q4 2018 of $34.2 and $0.13 respectively.

- 2020 analyst EPS estimates indicate that IEC’s EPS will grow 80% to $1.03, from 2019 estimates

- Estimates do not take into account acquisitions, a strategy we think the CEO is going to pursue

- In fact, on January 11, 2019, the company snuck in an 8-K detailing amendments to its current revolving credit line, increasing its limits to $27 million from $22 million; this may imply that an acquisition may be right around the corner

Overall, we think Schlarbaum’s plan will allow IEC to trade at premium valuation multiples. We also think shares could experience a short-term pop to the high end of our valuation assumption range as the market gradually becomes aware of the commentary in the IEC Q4 earnings conference call.

Eventually, we believe IEC could wind up near $20.00, sometime in 2020.

Caveats

- Although 12% gross margins are above the industry average, we still consider them (as well as the high-end potential of 18%) to be well below gross margins we look to normally invest in

- Visibility for the future of the company is still not where it has to be

- Being that IEC is a technology company, investor sentiment will be highly sensitive to market views on economic sentiment, even though the CEO’s plan may limit the company’s exposure to economic cycles

- Supply constraints (due to the strong economy) could impact the ability of the company to meet customer demands

- The company does not outsource its manufacturing, which gives it some flexibility on this risk since it can manufacture product as soon as supply constraints abate

- As of Q4 2018, IEC had a cash balance of zero, although over the years it has been typical that IEC has operated with little to no cash on hand

- Even though they are maintaining profitability, they have yet to show consistent YOY EPS growth, which has been one of our concerns.

- We have not performed a deep dive industry analysis

- Not Cheap on trailing 12-month basis