By Maj Soueidan, President & Co-founder of GeoInvesting

Introduction

At one point during my interview with Michael Morrison, the CEO of Datawatch Corporation (NASDAQ:DWCH), he stated:

“We are sitting in a good place with a very differentiated technology.”

Those types of statements are music to my ears when I am hunting for potential stocks that can multiply over time, sometimes known as multibaggers. It’s a term coined by my favorite stock picker and legendary fund manager, Peter Lynch.

Although I don’t own the stock yet, we at GeoInvesting are adding the 25 year old data management software company to our Multibagger Model Portfolio. We considered adding the stock to our Favorite Model Portfolio too, but as we will explain, we believe growth could be somewhat lumpy on a quarterly basis in the near-term as the company completes a shift in its business model.

As a reminder, our Favorite Model Portfolio is designed for stocks that we think are timely in the short term. Our Multibagger Mock Portfolio is designed to highlight stocks that we think have the right management teams and share structures in place to multiply in value several times over the next 3 to 5 years. However, we may deem that some of these stocks may not be timely in that certain factors may pose a near-term risk. When this is the case, we try to point this out, as we are doing with DWCH.

When we hold the opinion that a stock is both timely and offers longer term compounding potential, we may add it to both model portfolios.

We believe that DWCH is in the sixth or seventh inning of transitioning from a perpetual licensing business model to a recurring revenue software model that we think could eventually provide the company with a more predictable revenue stream, better growth outlook and an expansion in its valuation multiples. We really like where management is taking DWCH, but until the business fully shifts, the company could report surprise negative quarters, chasing short-term investors to the sidelines.

Specifically, we believe that investors who think the profitability achieved in Q3 2018 (year ends in September) is the new standard, are probably making a risky assumption. Software businesses are typically focused on driving top line growth through aggressive sales and marketing spend. We thought it would be prudent that you understand this risk up front. From the Q3 2018 conference call:

“Non-GAAP net income of 940,000 or $0.07 per diluted share shows that we continue to be very disciplined with our approach to investing in the business an approach that’s grounded on maximizing total revenue growth while running the company to a breakeven level.”

Analyst EPS estimates may be too optimistic in assuming DWCH will consistently maintain profitability through 2020.

But an upside surprise that could render analyst revenue estimates to be somewhat conservative is also possible. This is because analysts may not account for some of the synergies driven by a new product line-up giving the company a complete offering in the data analytics market for the first time in its history. We understand tha that If and when we pull the trigger to establish a position in DWCH, we may have to take a long term outlook on our position.

An exciting and game changing development at the company is the recent acquisition of a predictive analytics company that provides the company with significant cross selling opportunities and the potential to meaningfully increase its recurring revenue base (currently 60% as of the most recent quarter). Faster than expected cross selling execution and the consummation of additional acquisitions could accelerate the company’s transition.

Here is a snapshot of what analysts are expecting in terms of sales and earnings (Year ends September):

Sales

EPS

We are particularly keen on tracking DWCH due to the difference in the enterprise to sales multiple (EV/S) it trades at compared to the best publicly traded comparable, Alteryx, Inc. (NYSE:AYX), who is losing money: 4.3x vs. 23.7x. Part of the reason for this big divergence in EV/S probably has to do with the fact that almost 100% of AYX’s revenue is recurring. While we are not saying that DWCH’s EV/S will rise to 20 , the disparity is still worth noting.

We Love Recurring Revenue Transformations

Understanding the Recurring Revenue Model

In order to understand where DWCH is heading, I thought it would be a good idea to discuss the characteristics of three common software revenue models:

- Perpetual License

- Subscription

- Software as a Service (SaaS)

Traditionally, software companies sell their software platforms in a fashion where customers pay a large one-time, up front licensing fee, and then lower annual maintenance/update fees based on a percentage of the licensing fee. This arrangement is sometimes referred to as a perpetual license. Basically, the customer pays once and owns a license to use the software forever.

By contrast, in recurring revenue software models such as subscription and SaaS models, the customer pays smaller on-going fees for the right to use the software for a period of time. Even though revenue per customer in this type of relationship is typically less in the short term, compared to a perpetual license, over time a customer could end up generating more revenue. These models also give companies a smoother quarterly revenue profile which appeases investors’ risk aversions. SaaS type models also open the door to more potential customers because the large upfront perpetual licensing fee limits the size of customers that a software company can target.

Smaller and medium size enterprise (SMEs) may not be able to afford bigger price tags. In fact, in the U.S., “30 million SME accounted for two thirds of net new private sector jobs over the past few decades” and make up 99% of all companies in the European Union (EU). Shortly after the turn in the millennium, SaaS models started to gain steam.

Model Outline

Here is a brief comparison on how the three models look:

Pre-SaaS/subscription fee model days, commonly referred to as perpetual licenses. Typical aspects of these relationships include:

- Customer pays one-time, up front, licensing fee to own the software

- Revenue is recognized on the books right away

- Customer has the option to pay an annual upfront maintenance fee to receive services and updates from the Company. Fee can be renewed, annually.

- Fee is recognized over the term of maintenance contract. The unrecognized portion of the fee is recorded as deferred revenue on the balance sheet.

- Servers and hardware are usually the responsibly of the customer, also referred to as on-premise relationship.

Assume a software company inks a $100K deal with a customer on January 1, 2018:

- On January 1, customer pays $100K for right to own the software

- Revenue is recognized on the books right away.

- On January 1, customer agrees to pay 20% ($20k) of license fee as maintenance for one year. Revenue is recognized over 12 months.

- Company gives customer option to renew the annual maintenance contract for $20K.

- Lifetime revenue to company equals one-time payment of $100k $20K for as many years as contract is renewed.

- After 3 years, revenue received was $160K

Subscription fee model, Aspects of this type of relationships include:

- Customer pays an annual upfront fee for the right to use the software and receive maintenance services for a period of time.

- Until recently, the entire fee was recognized over the term of the contract. The unrecognized portion of the fee is recorded as deferred revenue on the balance sheet.

- Now, due to a new GAAP accounting rule, Topic 606,* under certain conditions, a portion of the fee must be recognized right away, and a portion is recognized over the life the contract.

- Customer has option to renew the relationship, annually.

- Servers and hardware are the responsibly of the customer, also referred to as on-premise relationship

- In the short run, the annual upfront fee is typically less than the combined fees that would occur under a perpetual licensing arrangement.

Assume a Software Company inks one year $50K deal with a customer on January 1, 2018.

- On January 1, customer pays $50K for right to use software and receive maintenance services for one year. Assuming Topic 606 is applicable.

- 80% Of revenue is recognized on the books right away.

- 20% Of revenue is recognized over the term of contract.

- Company gives customer option to renew the relationship, annually.

- Life time revenue to company equals payments for as many years as contract is in place.

- So, after 3years revenue received = $150

Software as a Service (SaaS) Model, Aspects of this type of relationships include:

- Customer pays an annual upfront fee for the right to use the software and receive maintenance services

- Until recently, the entire fee was recognized over the term of the contract. The unrecognized portion of the fee is recorded as deferred revenue on the balance sheet.

- Now, due to a new GAAP accounting rule, Topic 606, under certain conditions, a portion of the fee must be recognized right away and a portion is recognized over the life the contract.

- Customer has option to renew the relationship, annually.

- Unlike a perpetual license or subscription fee model, servers are hosted in the cloud and less hardware is required to be maintained by the customer.

- In the short run, the annual upfront fee is typically less than combined fees that would occur under a perpetual licensing arrangement

Assume a software company inks a one year, $50K deal, with a customer on January 1, 2018:

- On January 1, customer pays $50K for right to use software and receive maintenance services for one year. Assuming Topic 606 is applicable.

- 80% of revenue is recognized on the books right away.

- 20% of revenue recognized over the term of contract.

- Company gives customer option to renew the relationship, annually.

- Lifetime revenue to company equals payments for as many years as contract is in place.

- After 3 years, revenue received is $150k

SaaS and Recurring Revenue Transformations Present “Valuation Gap” Opportunities

Our attraction to DWCH builds on our obsession to find stocks with mispriced recurring revenue business models. Long-time GeoInvesting members know that one of our favorite places to look for these types of chances is in companies that are transitioning their businesses from lumpy revenue streams to predictable and growing revenues. Software companies shifting from perpetual licensing models to SaaS models are a great place to find these gems.

SaaS, or recurring revenue “transition companies”, will often experience large discounts to valuations compared to peers that are mainly generating recurring revenue. This gives us a chance to buy shares of well-managed companies at attractive valuations. This valuation gap generally exists for two reasons.

First, until the business model shift is complete, revenue streams, quarter to quarter, can still exhibit a good deal of lumpiness. It will take time (maybe multiple years) for revenue growth to look cosmetically appealing on a quarterly year over year or sequential basis. This is because the smaller SaaS revenue streams are going up against larger perpetual licensing revenue, and investors often can’t see what lies beyond the surface.

Second, there is no guarantee that management will successfully execute a transition.

Some key transition trends to monitor are the change in the percent of recurring revenue as a percent of total revenue and the recurring revenue growth on a sequential basis (for example Q2 2018 vs Q1 2018). Eventually, year over year comps will present themselves favorably on an apples to apples basis. This is when valuation multiples can start to experience a significant and rapid expansion.

As recurring revenue at DWCH rises, we expect that its valuation multiples will follow suit.

*We are still gaining an understanding on how Topic 606 is applied when looking at different software business models. If any changes need to be made on how we interrupted the rule, we will surely let you know.

Reasons for Tracking DWCH

New CEO Rises to the Challenge

I am keenly interested in investing alongside experienced management teams that have faced and conquered major hurdles in their past, while building companies. Without exception, my first question when I am interviewing management teams is to ask CEOs to address challenges they have faced growing companies.

Investing in proven CEOs who were “humbled” by past mistakes reduces my risk and gives me the confidence to hold stocks through rough patches that inevitably occur. Great managers use missteps made in the past as a gateway to grow into the future. DWCH CEO, Michael Morrison, looks like he fits this mold.

Simply stated, DWCH helps its customers gather, organize and prepare data so it can be presented in a format that can be analyzed to possibly build predictive models.

In its most recent 10-K DWCH describes itself as:

“…a leading provider of self-service data preparation and visual data discovery software. Within the broader Big Data and analytics software market, Datawatch’s solutions are focused on the business intelligence and analytic tools and analytic data integration markets.” (Big Data)

And in its Q3 filing, which accounts for an acquisition made after the 10-K was filed, it states:

“Datawatch Corporation (the “Company” or “Datawatch”) is engaged in the design, development, marketing, distribution and support of business computer software primarily for the self-service data preparation, predictive analytics and visual data discovery markets.”

Michael Morrison joined the company in 2011. Morrison has been involved in several business analytics software companies since he graduated from Law School in 1987 and came to DWCH with an impressive pedigree. His work experience includes holding positions at Applix (old symbol APLX), Cognos (old symbol COGN) and International Business Machines (NYSE:IBM) between 2004 and 2011. APLX was acquired by Cognos in October 2007, where Morrison continued to play an executive role, which carried over to International Business Machines (NYSE:IBM) after it acquired Cognos in January 2008. His bio, per company disclosures, states:

“Michael A. Morrison, age 54, has been a director and the Chief Executive Officer of the Company since February 2011. From October 2007 until joining Datawatch in 2011, Mr. Morrison was Vice President, Financial Performance Management, at Cognos Inc., a subsidiary of IBM since January 2008. In this role, Mr. Morrison directed all development, product management, product marketing and strategic business development activities for the FPM business unit. From January 2007 to October 2007, Mr. Morrison was Chief Operating Officer of Applix Inc., having been vice president of worldwide field and marketing operations from 2004 until his appointment as COO. At Applix Mr. Morrison conceptualized, built and led the company’s strategic go-to-market sales model and growth strategies, and also represented the company to Wall Street and industry analysts. Before joining Applix in 2004, Mr. Morrison held various positions at Cognos, including vice president of enterprise planning operations, vice president of finance and administration, and corporate counsel. Mr. Morrison’s qualifications to serve on the Board of Directors include his business, operational, management and legal experience in the enterprise application industry, as well as his position as Datawatch’s Chief Executive Officer.”

Morrison explained that the business analytics “stack” consists of two major layers:

- Data management: Retrieving, organizing and massaging organic or third-party data so it can be analyzed

- Data analytics: Studying data to make more optimal business decisions (Drive revenue and save money)

Prior to Morrison’s arrival, DWCH was a one product category in the data preparation segment of the data management stack. The core focus of the company was driving profitability, with revenue growth taking a back seat. This is not the common path that many successful software companies in the early phase of their growth cycle usually take. Spending capital to drive sales growth and amass sticky customers is of prime importance.

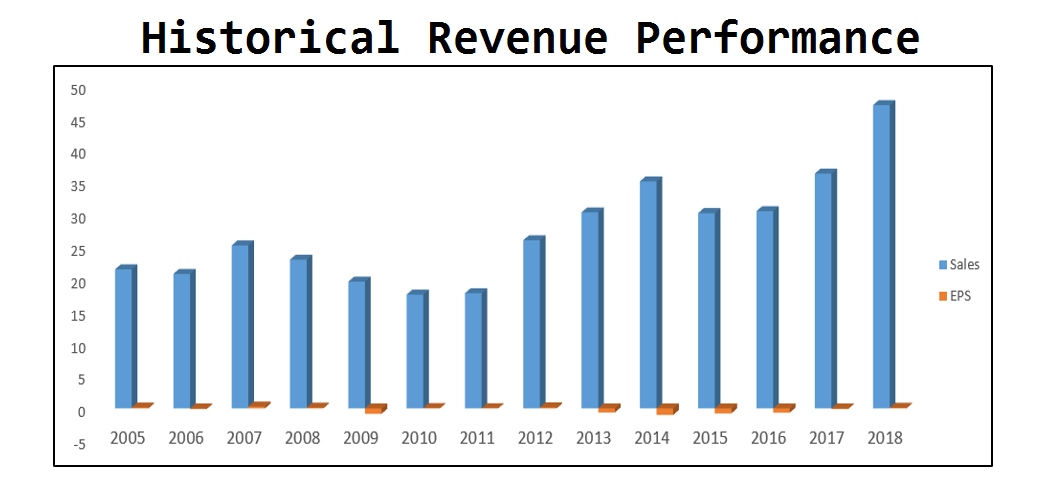

Before Morrison arrived, even though DWCH was largely profitable, sales were in a steady decline, falling from $25 million to $17 million over several years. They had declined for 15 straight quarters despite having developed a best in class product that could manage and clean the most difficult types of “static” (as opposed to data in motion) organic or third party data, wherever it resided (putting it in rows and columns), such as data included in:

- PDFs

- Web Pages

- Phone Bills

- Invoices

While the company had amassed over10,000 clients, Morrison pointed out that growing revenue became an issue because no official category existed for the company’s data preparation business. This made it increasingly harder to get customers to fully adopt what DWCH was selling. Furthermore, its legacy product (Monarch Classic) had not experienced a major update in several years.

As a result, Morrison’s first challenge was to forge a path to reignite revenue growth through replacing the entire organization, including the sales staff, with a more aggressive team (including some people from past relationships).

It seemed that Morrison was the magic bullet.

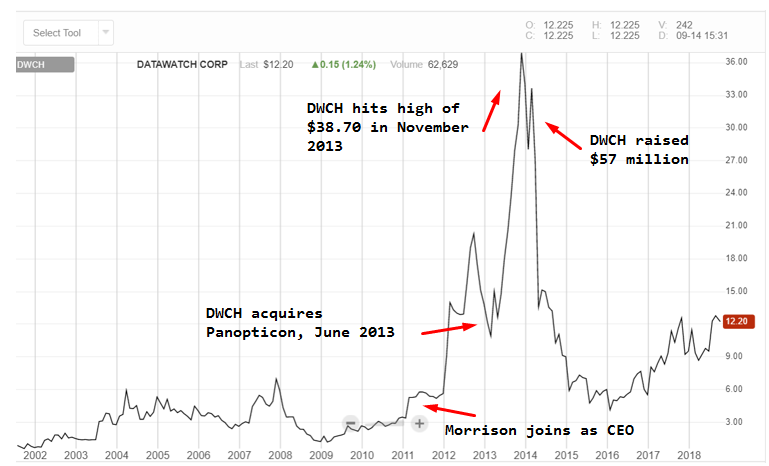

Over the next 2 years, the stock took off, on the heels of improved sales growth:

- His first full year with the company, sales grew 50% to $26 million

- His second full year, sales grew 20% to $30 million

In Morrison’s third year with the company, he knew he had “eaten” much of the low hanging fruit left behind by the old management team. Realizing that the “no product category” issue would soon limit growth, the company acquired Panopticon in June 2013 to enter a new market category. DWCH customers were asking for real time analytics services, which is what Panopticon delivered. The stock responded, reaching a high of $38.70 in November 2013 and the company raised $57 million. Sales reached $35 million in 2014.

In 2014, Morrison faced his second challenge. The defining event DWCH had been waiting for finally happened: analytics firm Gartner (NYSE: IT) came out with an official category for “data preparation”. Instead of seizing the opportunity to concentrate on what the company does best, Morrison decided to aggressively drive the revenue of Panopticon, a sexier area of the market at the time.

Also in 2014, DWCH brought on a new hire to head sales, replacing a duty Morrison was spearheading. These turned out to be bad decisions and did not deliver the expected results. To make matters worse, while DWCH was attempting to grow Panopticon, its major competitor, Alteryx, Inc. (NYSE:AYX) did what DWCH should have done by going “all in” on data preparation through a transformative acquisition. Business slowed, the company’s revenue flatlined at around $30 million, and the stock got pummeled.

Morrison shouldered the blame for this misstep, like good accountable CEOs do. He quickly responded by making some personnel changes to focus the business on strength of their data preparation business (Monarch), in part by introducing the next generation version of Monarch (Monarch Complete).

It took some time, but it looks like the company is gaining some traction. Sales have grown for 7 straight quarters and are on track to easily eclipse the company’s highest annual performance of $36 million, achieved in 2014. The company has had spotty spurts of growth in the past, so it still has it prove to the market that is has turned the corner. But with a more complete product offering, and a new recurring revenue model, this time around things could be very different.

CEO’s Vision for Growth Makes Perfect Sense

Soup to Nuts Solution

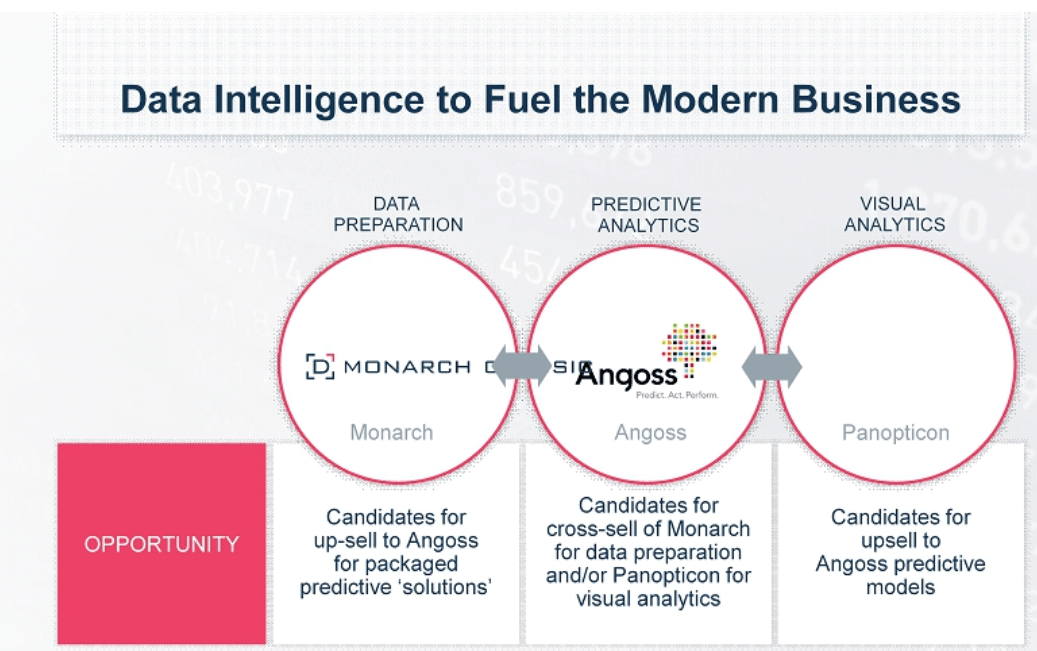

Over the past few years, DWCH has made some moves that now allow it to offer customers a complete data analytics solution. These moves are based around the following concepts:

- Organize

- Visualize

- Predictive Models

Organizing Data

DWCH’s product offering can work with data at rest or in motion.

“Data in motion is the process of analyzing data on the fly without storing it. Data at rest is a snapshot of the information that is collected and stored, ready to be analyzed for decision-making.”

Examples of static data include information contained in databases or in other formats, like Word documents and PDFs. Data in motion is generated from a myriad of sources where analysis is needed quickly to make decisions. Cyber security, IoT and real time medical monitoring applications are a few examples where data in motion would exist.

The company's legacy product falls under its Monarch division and deal with static data. Its original product, called Monarch Classic, is an on-premise, perpetual license solution (one large payment for the right to use the software forever, along with yearly maintenance fees).

Monarch Complete is their next generation subscription fee, on-premise solution introduced in 2015 (smaller recurring revenue payments, renewed annually). Complete is easier to implement by a customer’s data analysts and also reduces staffing needs.

Just recently, the company expanded the Monarch family to include a SaaS cloud solution, Monarch Swarm (smaller recurring revenue payments, renewed annually).

Visualizing Data

In 2013, DWCH acquired Panopticon to allow it to collect and organize data in motion and in real time, as well as create visuals from data. It also extends the capabilities of Monarch. While the Monarch family only finds, gathers and organizes static data, this software allows Monarch to go a step further to “feed” this data into Panopticon to create and present visualization material based on the data analyzed and massaged by Monarch.

Monarch and Panopticon possess unique characteristics that make them well suited for the type of data the software is geared to deal with: static versus in-motion.

Charts and heat maps like these are two visualization examples:

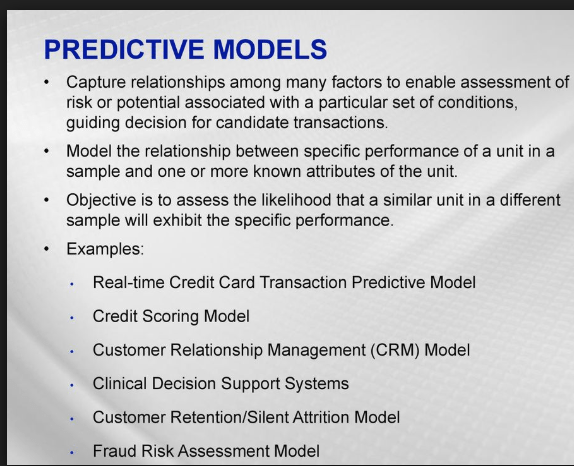

Predictive Models

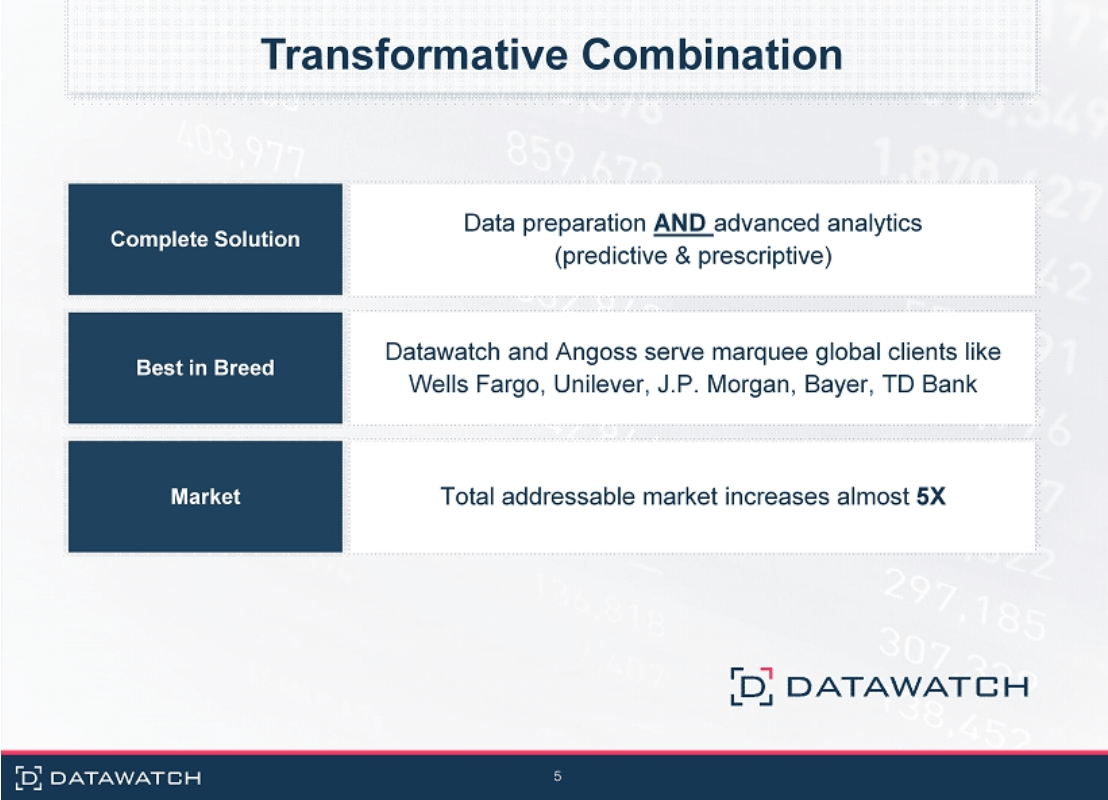

In January 2018, the company acquired Angoss Software, which generates over 80% recurring revenue and was a game changing transaction. Angoss increases DWCH’s revenue base by about 30% (Additional $10.5 in revenue using Angoss 2017 numbers), gives the company a complete offering and puts the company in one of the hottest areas of the data analytics industry: predictive analytics.

“Angoss delivers powerful predictive and prescriptive analytics that help businesses discover valuable insights and intelligence in their data, and the company was recognized as one of the leaders in the Forrester Wave: Predictive Analytics and Machine Learning Solutions, Q1 2017. Angoss data science solutions are used by more than 300 organizations in 30 countries, including many global firms such as Barclays, Unilever, Scotiabank, TD Bank, Bayer, Wells Fargo, Bank of America and Air Canada. Angoss provides rigorous modeling and validation tools for machine learning in high-value applications for customer segmentation, customer churn, credit risk scoring, fraud detection, next best action, collections and recovery, and many other mission-critical solutions.”

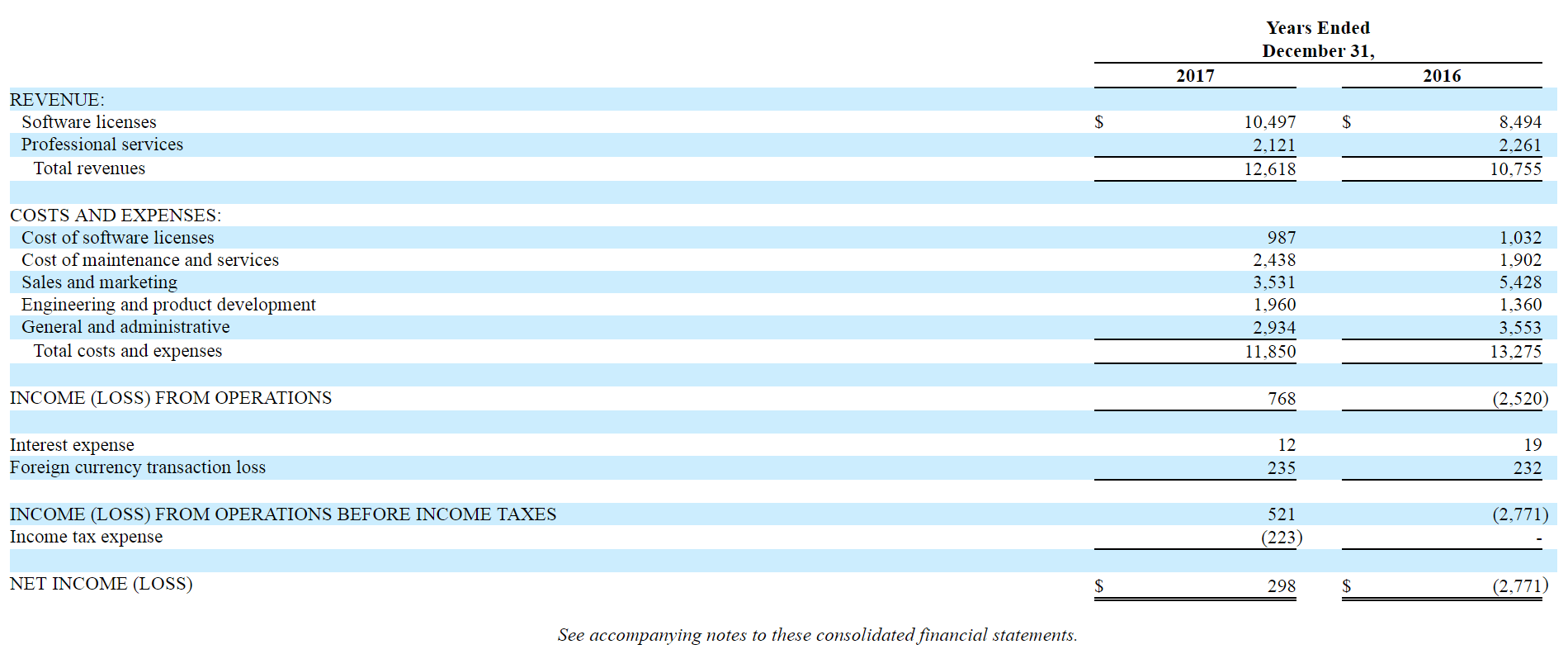

Taking a look at Angoss’s historical financials reveals that 2017 sales grew 17% and that the company swung to a profit.

(Image Source)

Here are some presentation highlights related to the Angoss acquisition:

Cross Selling Opportunities

Angoss doesn't really have an efficient data organization or visualization solution, and relies heavily on its customers to deliver data that is ready to be analyzed for predictive purposes. Now that Angoss is part of Datawatch, it can cross-sell these clients with Monarch and Panopticon for their data preparation needs.

Cross selling chances will also be available in DWCH’s current customer base in that data coming through Monarch or Panopticon can now be transformed into predicative tools. Angoss customers can now use Monarch or Panopticon for data prep and visualization data needs, too. Without Panopticon or Angoss, DWCH is just sending customers to companies like $DATA. Finally, cross selling chances exist between Panoptican and Angoss.

The Q3 2018 conference call transcript information arbitrage (InfoArb) highlights the strides the company is making:

Top Line

Various Management Comments:

“We have continued with the evolution of our go-to-market model, the outside sales team has remained focused on meaningful enterprise expansion while the inside team has continued to focus on transactional execution. The Hunter team continues to focus on new logo acquisition and closed another 73 new logos in Q3.”

“At the end of Q3 the team also hit a new milestone of 210 new logos since its inception earlier this year. Overall our pipeline continues to grow the Q4 pipeline coverage is healthier than has been in recent years. This includes our Panopticon pipeline which has significant six-figure deals and active sale cycles for Q4.”

“As Jim mentioned, our average deal size increased from approximately 39,000 in Q3 2017 to approximately 50,000 in Q3 2018. This is a trend that we expect to continue this year as our go-to-market focus on meaningful enterprise expansion continues to mature. Additionally our six-figure deals increased to 12 in Q3 2018 as compared to four in Q3 2017. Our integration of Angoss has been completed with regards to the go-to-market sales, marketing services, branding, product teams and back-office operations.”

“The underlying market and you can get this from a lot of industry analysts and all, the underlying market for streaming analytics is really starting to take off now. So we're in the right place at the right time. The products always been good. They were - in the early days after we acquired Panopticon we admittedly took it a little bit outside of its comfort zone.”

Q&A Exchanges

Chad Bennett (attendee)

“And then I know you guys don't formally guide, but considering the performance in the June quarter and it sounds like the confidence and good start to the September quarter. I would assume sequential improvement is reasonable both from a overall revenue standpoint and from a software license revenue standpoint is that fair?:

James Eliason (management)

It's fair and plus we’re going to our last quarter of the year, fiscal year for Datawatch. So it’s a fair comment and observation.

Improving Margins

Q&A Exchanges

Ilya Grozovsky (attendee)

“Just on the housekeeping front, you guys have looks like this quarter the OpEx was very much in control even better than I had expected kind of what’s the thought going forward specifically if you look at your G&A.”

James Eliason (management)

“So G&A some of that is going to go away in this quarter because as we mentioned the full integration of our Angoss back-office is completed so it’s going to drop. I would say I think as always the line leaders primarily jumped up within the product [side and can] [ph], with all the go-to market. They’re very measured in terms of making investments obviously Angoss is a big investment and I think they did a very - we all did a very good job of assessing what we had there. I would say all of Q2 we did that for the two months we own them and probably for the first half of Q3.”

“And now I know that we have plans to continue to invest not only in Angoss but across the company. So the plan hasn’t changed, we’re investing behind the revenue curve Ilya with [indiscernible] staying close to breakeven on a cash basis.”

Ilya Grozovsky (attendee)

“And then also on the margins for the maintenance and services piece kind of trended down a little bit, what’s the trend there going forward?”

James Eliason (management)

“That’s Angoss related, I think we had mentioned obviously they had a large, I'll call it managed services deal they did before we bought them. We took a very significant haircut on that deal so although we get the cash benefit of it on a revenue side, we don't get the full revenue benefit, but yet we’re carrying the cost of the people delivering it.”

“So it's down a bit its down three or four points on a percentage basis much like the revenue line that will come back in line over the next couple of quarters back into what we typically have 90% gross margins overall.”

Accelerating and Consistent Revenue Growth

Management is laying the groundwork for improved top line growth by driving recurring revenue and deepening its partner relationships.

Partner Relationships

DWCH sells its service through a direct sales force and partner relationships. DWCH partners come in two forms.

OEM partners are DWCH end customers or divisions of its customers. Through these relationships, DWCH attempts to identify instances where these customers’ divisions or clients could be candidates for DWCH offerings. In certain cases, when partners send a client to DWCH, it compensates them. For example, there may be an opportunity for a DWCH customer that is selling a solution software solution to his own customers to expand its offering to its customers by incorporating DWCH software. In this case, you can think of DWCH as a private label solution. In other cases, there could be instances where division of a larger organization refers DWCH to other divisions.

Of course, DWCH also has traditional reseller partners who basically just are the middlemen, finding customers that need to use DWCH services.

Using its customers and resellers as “ambassadors” allows DWCH to take pressure off its sales expense line and cast a wider net on potential customers. Now that DWCH has a complete solution, partner revenue contribution should accelerate. This Q3 2018 conference call excerpt talks about the better than expected progress DWCH is making on this front.

“We have continued to see increased traction in our partner channel. The partner team overall contribution grew 40% Q3 2018 versus Q3 2017. As previously stated cultivating the partner go-to-market has been investment for us, but has accelerated faster than our original projection of having an impact late in FY 2018.”

Driving Recurring Revenue

The company's transformation to a recurring revenue model began in 2015 when it launched Monarch Complete. DWCH has been encouraging its Monarch Classic perpetual license customers to transition to Complete and requires that all new Monarch customers use Complete. So far, of the 3000 customers that are using Complete, about half are legacy customers and half are new relationships. Panopticon revenue has traditionally been derived from perpetual license arrangements, but the company is transitioning it to a subscription model. Nearly 100% of Angoss revenue is recurring.

The cloud version of Monarch (Swarm) also generates recurring revenue, but is still an insignificant part of the business. Some customers may be weary to move to the cloud when data is highly sensitive and when privacy is a concern, but DWCH should be ready as businesses begin to understand the advantages of being on the cloud vs. on-premise and become more comfortable with the cloud

DWCH Recurring revenue was about 60% at the end of Q3 2018, up from about 25% a year ago, which could provide an opportunity to build a position in the stock at valuation levels below its comps, before recurring revenue rises, especially if the company continues to be active on the acquisition front. In fact, during its third quarter conference call management commented that:

“But I will say on the recurring revenue front, if we do not do anything with our current model it will just by virtue of our business continue to grow. We mentioned that it was almost 60% of our total revenue this quarter. We expect by the end of next fiscal year that will be a 10 points or more and we are - as we’re sitting here planning into next year, we’re debating whether to dial-up the transition there. It will naturally just come about over the course of the next two or three years, but we haven't decided yet whether we intend to dial it up and get there a little bit quicker. But like I said in the - if we don't do anything it still - we will be here a year from now with 70 plus percent of our revenue coming in on a recurring basis.”

Industry

Several favorable industry trends are working in DWCH’s favor.

Trend One: Self Service Analytics

A broad “big data” market that DWCH operates in is Self Service Analytics. This market is what Monarch Complete was created to address. $DATA was the first company to break into this segment. Traditionally, data at firms has been predominantly examined by data scientists. However, the amount of data being collected by businesses and the speed at which it needs to be diagnosed has created the need for automated or less labor-intensive solutions. This solution is called Self-Service Analytics (SSA).

“Self-service analytics is an approach to advanced analytics that allows business users to manipulate data to spot business opportunities, without requiring them to have a background in statistics or technology. Increasingly, vendors are introducing products that allow business users to work with data that's aggregated from a range of sources. The software provides users with a dashboard that allows the users to query and manipulate large amounts of data. In the past, such data analysis was solely the domain of trained data analysts, who are now often referred to as data scientists.”

Not only do self-service analytics give companies a competitive edge, but they can also save them money by reducing the need to hire data analysts. It also broadens the market. While data scientists will not disappear when dealing with highly sensitive data, SSA is quickly displacing the heavy reliance on data analysts and is expected to experience a CAGR of 20% between 2016 and 2022, reaching a market size of $10 billion.

In fact, Gartner just published a report, predicting that:

“by 2019, the analytics output of business users with self-service capabilities will surpass that of professional data scientists.”

Trend Two: Data Preparation (Monarch Family)

The more complex data being collected increases the need to make predictions with data. Privacy/security issues have created an increased emphasis to ensure quality: that the right data is moving though a business.

“Among tools, the data quality segment is expected to hold the largest market share in the data prep market in 2016. Data quality tools ensure that the data fits a particular user- specific task and is accurate & timely. Data quality is affected by the way data is entered, stored, and managed, and organizations are making use of the data quality tools to maintain consistency and improve decision making.”

DWCH is a great position to benefit from trends occurring in the overall data prep segment as well as its core emphasis in the self-service market.

“The data prep market size is estimated to grow from USD 1.46 Billion in 2016 to USD 3.93 Billion by 2021, at a Compound Annual Growth Rate (CAGR) of 25.2% during the forecast period.”

“Among the platforms, the self-service data prep segment is expected to grow at a fast pace during the forecast period. The demand for self-service data prep platform is increasing among enterprises as it helps canvas the existing data into user-centric formats, which then help in efficient data analysis, faster decision making, optimized internal business processes, increased operational efficiency, and a competitive advantage in the market.”

Trend Three: Visualization (Panopticon)

The increasing adoption of firms to perform predictive analysis from data has increased the demand for visualization tools. These tools allow companies to interpret large amounts of data through easy to understand visuals. As the saying goes, a picture is worth a thousand words.

Data visualization is a general term that describes:

“any effort to help people understand the significance of data by placing it in a visual context. Patterns, trends and correlations that might go undetected in text-based data can be exposed and recognized easier with data visualization software.”

“Visualization is central to advanced analytics for similar reasons. When a data scientist is writing advanced predictive analytics or machine learning algorithms, it becomes important to visualize the outputs to monitor results and ensure that models are performing as intended. This is because visualizations of complex algorithms are generally easier to interpret than numerical outputs.”

The data visualization market:

“was valued at USD 4.51 billion in 2017, and is expected to reach a value of USD 7.76 billion by 2023 at a CAGR of 9.47%.”

Trend Four: Real Time Data (Angoss)

Driving revenue, saving money and managing risk are key uses of “big data”. Predictive analytics:

“refers to the use of statistical tools and machine-learning algorithms to identify past occurrences, understand present outcomes and predict future consequences. Predictive analytics helps in detecting frauds, optimizing marketing campaigns, improving present operations, and reducing future risk. Predictive analytics refers historical and present data to forecast future activities, behavior, and trends. Predictive analytics model capable of processing historical and present data combines multiple variables and uses logistic regressions, decision trees, and time-series analysis. Use of predictive analytics has prominently grown alongside the emergence of big data systems.”

Mobile and IoT:

True mobile and real-time data. By 2025, more than a quarter of data created will be real-time in nature, and IoT real-time data will constitute over 95% of it.

Embedded systems and the Internet of Things (IoT). By 2025, an average connected person anywhere in the world will interact with connected devices nearly 4,800 times per day – basically one interaction every 18 seconds.

Mergers and Acquisitions

Acquisitions in the data analytics sector have been very active over the past several years. For example, according to this article on July 24, 2018, there were at least 5 recent acquisitions in this broad field that took place in 2018:

- Qlik acquires Podium Data

- Google (NASDAQ: GOOGL) acquires Cask Data

- Oracle’s (NYSE: ORCL) acquires DataScience.com

- Tableau Software’s (NYSE: DATA) acquires Empirical Systems

- Salesforce’s (NYSE: CRM) acquires Datorama

In addition, a few days ago, Adobe also announced it would acquire Marketo, a market-leading cloud platform for B2B marketing engagement, for $4.75 billion.

Although the acquisition valuation multiple of these deals was not disclosed due to the fact that the acquired companies were private, it is obvious that M&A activities have been plentiful in this industry.

Prior to 2018, several publicly traded competitors that DWCH mentions were acquired:

- Informatica was acquired by a group of companies in 2015 for $5.3 billion.

- Actuate was acquired by Open Text in 2014 for $330 million.

- Tibco Software was acquired by Vista Equity Partners in 2014 4.3 billion.

It won’t be surprising to us if one day DWCH enters the radar of those bigger players and becomes an acquisition target in the future.

Valuation

According to DWCH’s 10-K, its competitors can be classified into four broad categories:

- Large software companies, including suppliers of traditional business intelligence products that provide one or more capabilities that are competitive with DWCH’s products, such as IBM, Microsoft, Oracle and SAP.

- New and emerging vendors focused more specifically on data preparation, such as Informatica, Alteryx, Paxata and Trifacta

- Business analytics vendors focused on real-time visualization, such as First Derivatives and Zoomdata

- Independent vendors that focus on extracting specific data formats or sources such as machine data, data in content management systems, EDI, XBRL, HTML and PDFs. These competitors include Splunk, Actuate (Xenos) and Informatica, among others.

DWCH states:

“Our self-service data preparation and visual data discovery products compete with those of other companies in the Big Data and business analytics markets. These markets are highly competitive and include companies such as DATA, TIBCO Spotfire (a subsidiary of TIBCO Software Inc.), Qlik Technologies, Inc., Informatica, AYX, Paxata, Trifacta and $FDRVF (FDP.L), as well as larger technology companies such as IBM, SAP, MSTR, SAS and Oracle.”

Here is a look at some of the comps we deemed to be relevant. We omitted large diversified comps, International Business Machines (NYSE:IBM), Microsoft Corporation (NASDAQ:MSFT) Oracle Corporation (NYSE:ORCL) and $SAP from the analysis, as well as companies that are private where we could not reference valuations. Two private companies that DWCH also goes up against often are Trifacta and Paxata. We added Attunity Ltd. (NASDAQ:ATTU), which was not mentioned in DWCH’s 10-K.

|

|

EV/S

|

Adjusted P/E

|

TTM Sales (USD'000)

|

Market Cap (USD'000)

|

Percent Recurring Revenue

|

Gross Margins

|

Debt to Equity

|

|

Datawatch Corporation (NASDAQ:DWCH)

|

4.2

|

N/A

|

40,296

|

147,070

|

60%

|

88%

|

0.3

|

|

Alteryx, Inc. (NYSE:AYX)

|

23.7

|

N/A

|

162,360

|

3,760,000

|

95%

|

68%

|

0.9

|

|

Splunk Inc. (NASDAQ:SPLK)

|

13.2

|

N/A

|

1,463,738

|

17,220,000

|

50%

|

77%

|

0.0

|

|

$DATA

|

9.4

|

N/A

|

992,769

|

9,430,000

|

53%

|

77%

|

0.0

|

|

$FDRVF

|

5.7

|

109.3

|

240,357

|

1,070,000

|

42%

|

28%

|

0.2

|

|

Attunity Ltd. (NASDAQ:ATTU)

|

5

|

N/A

|

72,801

|

406,840

|

40%

|

72%

|

0.0

|

|

$MSTR

|

2.2

|

N/A

|

506,660

|

1,680,000

|

67%

|

81%

|

0.0

|

|

Informatica (based on acquisition valuation in 2015)

|

4.9

|

30.7

|

1,047,954

|

5,300,000

|

56%

|

81%

|

0.0

|

|

Tibco (based on acquisition valuation in 2014)

|

3.5

|

27.0

|

1,0762,34

|

4,300,000

|

69%

|

70%

|

0.6

|

|

Actuate (based on acquisition valuation in 2014)

|

2.9

|

73.3

|

107,274

|

330,000

|

74%

|

84%

|

0.0

|

|

Qlik (based on acquisition valuation in 2016)

|

4.5

|

N/A

|

630,498

|

3,217,000

|

57%

|

85%

|

0.0

|

|

Comp. Average

|

~8.0

|

|

|

|

|

|

|

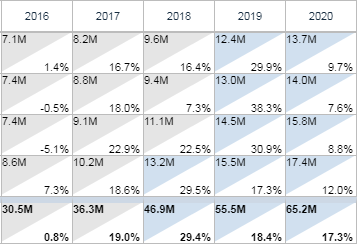

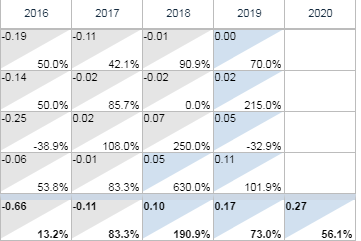

Over the past 5 years, almost all of the public traded companies have provided outsized returns:

It’s challenging to determine where the market will ultimately value DWCH. However, DWCH has the most complete product offering, the highest gross margins and is selling at an EV/S comfortably below five of its publicly traded comps. Furthermore, the recurring revenue as a percent of total revenue of four of these comps is below DWCH’s. Given that at one time, DWCH traded at a peak EV/S of about 10.4 in December 2013, we think considerable upside exists for DWCH if it can finally prove it has turned the corner for good.

Caveats

- Some investors will need management to provide more proof that the company has reached an inflection point.

- DWCH operates in a highly competitive industry and we have not performed deep channel checks at this time to see how they fare in the market. However, the company has been around for decades and has amassed over 10,000 customers. One thing I found interesting is that the company believes it has the only data visualization solution that can generate real time visuals with data in motion. With the growth in IoT, I see this as a large competitive advantage. Furthermore, it does appear that the company does have the one of, if not the most, complete service offering. More Q3 2018 conference call highlights:

“They’ve (Alteryx, Inc. (NYSE:AYX) ) stated they’re building their cloud ready Alteryx platform. I don't know when it will be in the market. I'm sure it will be quite competitive. We don’t see them in those use cases as of yet, but we do quite well at least, positioning ourselves and competing today when the driving agendas are cloud-based potentially SaaS-based solution for data prep data governance.”

“And the Datawatch platform can handle more data than anybody in the sector from structured to unstructured, from data at rest to streaming data in motion. We also have more experience and more loyal customers then anybody in this space. Our differentiated analytics platform and our rich history of innovation makes me bullish that our business momentum will continue to accelerate.”