RF Industries Ltd. (NASDAQ:RFIL) designs and manufactures a broad range of interconnect products across diversified, growing markets including wireless/wireline telecom, data communications and industrial. RFIL was actually a past GeoBargain that reached a high return of 68% during our coverage period, before its removal from the list in November of 2013:

“We first disclosed our long position in RFIL on 3/18/2013 at a price of $6.37 when we alerted premium members of our bullish article “Is Rf Industries’ (RFIL) Increased Dividend Payout a Clue to Consistent Growth?” We then added the stock to our GeoBargain list on 4/10/2013 at $6.46, however we are now removing RFIL from the list at the price of $9.50, or 47% higher than when it was added. The stock reached a 52-week high of $10.86, or 68% higher from our initial coding.

While RFIL has surpassed our near-term price target mentioned in our article of $8.75, it has not yet reached our higher end price target of $13.00.”

We removed RFIL due to some concerns we had about the stickiness of its growth plan. More importantly, RFIL disclosed a legal issue in its last two 10-Q's at a time that we felt could lead investors to question the integrity of management once/if these issues became more apparent:

“On May 24, 2013, a former employee of the Company filed a complaint with the San Diego, California office of the U.S. Department of Labor-OSHA alleging retaliatory employment practices in violation of the whistleblower provisions of the Sarbanes-Oxley Act. The complaint alleges that the former employee was terminated in November 2012 in retaliation for making disclosures relating to fraudulent accounting practices and lack of compliance with U.S. GAAP; violations of multiple Securities and Exchange Commission rules and regulations; and fraud against the shareholders. The complaint does not seek any specified amount of damages, but does seek various forms of relief, including the following: Reinstatement of the former employee’s employment, or in the alternative, an award for lost future wages, benefits and pension; back pay and bonuses; compensatory monetary damages in an amount to be determined; reasonable attorney’s fees; and all costs of litigation. The Company disputes the retaliation claim and has notified its employment practices liability insurance carrier of the demand.”

We certainly can’t ignore some of the allegations in the complaint, but it has since been settled and the company is now being led by a new CEO:

"The Company tendered the claim to its insurance carrier for defense and indemnification, and counsel appointed by the insurance carrier represented the Company in the matter. At a mediation held in July 2015, the parties agreed to settle the matter for an amount that was covered by the Company’s insurance policy. The parties have entered into a written settlement agreement and anticipate formal dismissal of the case within the next few weeks."

Looking at RFIL’s financial performance, this table illustrates the lumpiness and lack of growth RFIL has experienced over the years:

We are now placing RFIL back on our radar due to management’s cost control efforts that seem to paying off (under a new CEO), insider buying, and recent strong bottom line results.

Our reasons for tracking RFIL

1. Improved earnings

In our September 12, 2017 email, we highlighted RFIL’s strong Q3 2017 EPS results on weak revenue growth (fiscal year ends Oct. 31). The focus moving forward will be to step up revenue growth. The company reported:

- Sales of $7.8 million vs $7.6 million in the prior year

- EPS of $0.02 vs a loss of $0.05 in the prior year

Comments from the Q3 release:

"The RFI team has done a great job of putting strong cost controls in place. We are now focusing our efforts on increasing sales through improved go-to-market strategies and channel models across all of the Company's divisions. We have great quality products, a strong balance sheet, a solid team, and long-standing customer and vendor relationships. With those core fundamentals in place, the coming quarters are really about getting all of our businesses cranked up to deliver positive results. While we still have work to do, I am optimistic about the remainder of the fiscal year. In coming quarters I look forward to communicating more frequently about our ongoing strategies to profitably grow the business while maintaining the same level of quality we have delivered for over 35 years."

2. New CEO Robert Dawson comes aboard in June 2017 with a focus of cutting cost and increasing sales

"Robert Dawson's experience in information technology, telecommunications and wireless technology will help management support RFI's growth. His direct sales experience in wireless infrastructure, mobile and broadband networks fits right in with Company’s product line-up," said Mr. Hill, the company’s interim President and CEO.

Mr. Dawson has been involved with mergers and acquisitions in other public companies in the past.

3. Selling off assets

Even before the hiring of Dawson, RFIL had been making moves to streamline its business by disposing of assets in 2015 and 2016:

During March 2016, the Company announced the shutdown of its Bioconnect division, which comprised the entire operations of the Medical Cabling and Interconnect segment. The closure was part of the Company’s ongoing plan to close or dispose of underperforming divisions that are not part of the Company’s core operations.

On December 22, 2015, the Company sold the assets of its Aviel Electronics division at a gain of approximately $35,000. The sale of the Aviel Electronics division does not represent a strategic shift that has a major effect on the Company’s operations and financial results.

4. Focus on New Growth Areas

After reporting a loss for the first time since prior to 2006, management decided to point its technology towards the Distributed Area Systems (“DAS”) market:

For the first time in over two decades, in the fiscal year ended October 31, 2016 the Company experienced an annual net loss. In order to address the changes in the Company’s marketplace, the Company has focused its marketing and sales efforts, in particular in the rapidly growing Distributed Area Systems (“DAS”) market. As a result of these increased marketing efforts, the Company has seen a significant increase in sales during the nine months ended July 31, 2017, including in the sale of higher margin DAS products. The Company has also implemented stricter cost control measures and rationalized some of its operations. These controls have resulted in a significant decrease in the Company’s operating expenses during the nine months ended July 31, 2017. The lack of extraordinary costs/charges and the combination of increased sales and lower costs, have returned the Company to profitability for both the fiscal quarter and nine-month period ended July 31, 2017.

We first talked about DAS during our coverage of Wireless Telecom Group Inc. (AMEX:WTT) in April of 2013. A DAS network can provide more coverage and is more efficient than a traditional antenna. Since only a small percentage of the wireless market utilizes DAS, a good deal of growth opportunity could be in the cards. Below is an overview of the DAS market from www.radio-electronics.com:

“The concept of a Distributed Antenna System, DAS has many advantages in some applications. A Distributed antenna system, DAS is a network of antennas spaced apart from each other, but connected to a common source. In this way the DAS is able to provide wireless or radio coverage within a given area.

The idea of a distributed antenna system is being adopted increasingly as it enables a number of advantages to be gained. However, this is at the cost of a larger more complicated system. Nevertheless, distributed antenna systems are being used in a variety of areas to enable the right coverage to be gained for several applications.

Although the concept of distributed antenna systems has been known about for many years, it is with the increased deployment of wireless systems within buildings and other difficult coverage areas that the idea of distributed antenna systems has come to the fore.”

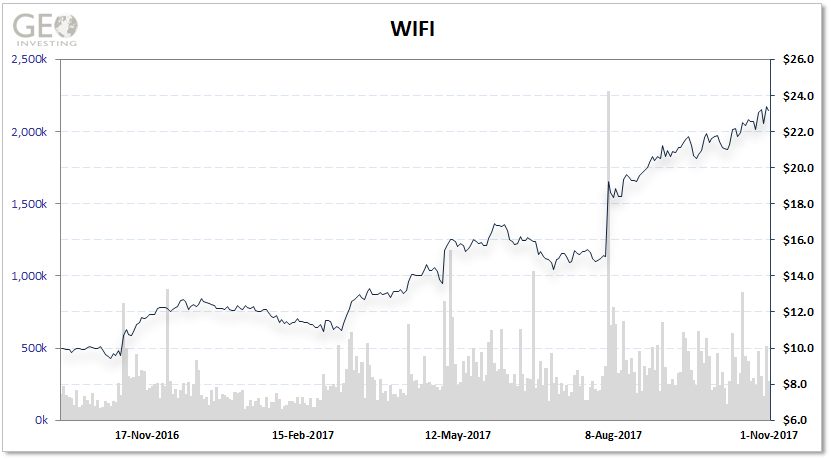

We noticed that Boingo Wireless Inc. (NMS:WIFI) is also benefitting from its focus on DAS:

We have also come across DAS industry stats that estimate it will grow from 2% to 6% out to 2020/2022. While not huge growth on the low end, RFIL revenue is tiny compared to the potential market size (near $7 billion).

5. Insider buying

Over the past month, a number of insiders have bought shares at open market prices, including new CEO Robert Dawson. While none of the purchases were of dramatic size, seeing a number of executives purchase shares shows that management has confidence in the story and is aligned with shareholders.

6. Growth and value

With its steady dividend and the company possibly being on the verge of entering a growth phase, RFIL becomes an interesting “growth plus value” candidate. The company has paid its 29th straight quarterly dividend with its past Q3 results. With an $0.08 annual dividend, the company currently has a healthy 2.9% yield. With no debt and a strong balance sheet, it seems the company’s trend of continued dividends should be sustainable. We would not have an issue with the company terminating its dividend and reinvesting in growth, assuming the rates of return are favorable.

Valuation

Based on traditional valuation measures like P/E, RFIL is not undervalued. However, the stock is trading right at its book value. If management successfully executes on its plan to drive growth, this story could get interesting. WIFI has been on a tear on the heels of its focus on DAS and is actually losing money!

The company’s balance sheet looks strong:

- Positive cash flow of $1.6 million (ttm)

- No debt

- Current ratio: 4.92

- Book value: $2.38

Speaking with management will help us understand the story better. Setting up timely interviews is something we continually strive to do..

Caveats:

- Telecom companies were slow to adopt DAS and there is no guarantee that they will continue their current pace of adoption

- Better technology could emerge

- We would like to learn more about RFIL’s acquisitions over the last couple years

- Seasonality; Q1 is the company’s seasonally weakest quarter and then sales generally strengthen throughout the year