$CRTN provides consulting services for communications digital media and technology in the United States, UK, and Western Europe. On November 14, 2016, we published a small note on CRTN stating that our full “Reasons for Tracking” (RFT) the company was forthcoming. You can see that note here. We also added the stock to our run to one screen here.

As a consulting firm, the company helps customers with strategic decisions when they offer new products and enter new markets. It also provides customers with advice on how to tackle certain administrative tasks to maximize revenue and maintain customer satisfaction.

The Company Has Our Attention

Shares are trading near liquidation value which we feel makes a good case for limited downside with substantial upside from current levels. Shares are essentially priced for business failure.

- At around $0.70 the company is trading near our most conservative estimate of liquidation value of $0.61. But we think a more realsitc range falls between $0.68 (excluding intangible assets) and $0.75.

- Restructuring moves aim to:

- Reduce lumpiness in revenues

- Explore recurring revenue projects

- Enter growth markets

- The company could be in the position to maintain profitably heading into 2017

- Insiders are buying shares

- Stock came under pressure after a big investor sold his stake in July on no news. Shares have not recovered since

- Complex earn-out agreement masks real value. We took into account the earnout terms in our liquidation value calculation.

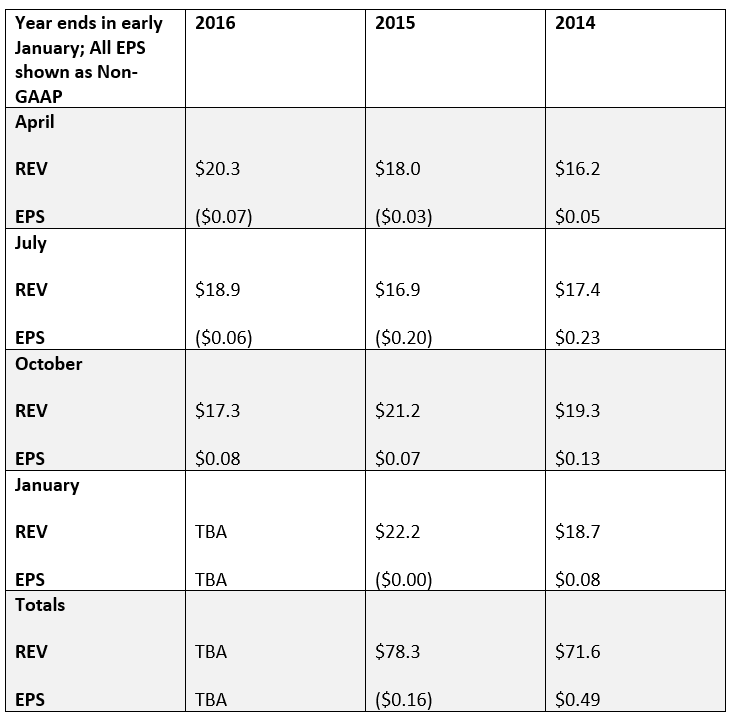

- Efficiency improvements are beginning to take shape; CRTN posted positive EPS in Q3 2016 for the first time in several quarters,

Brief History

Cartesian was founded in 1990 by Richard Nespola and went public in 1999 at a valuation of over $1 billion. Formerly named TMNG Group, the company changed its name to Cartesian Inc in 2014. Over the course of its history the company acquired a range of businesses, continuously seeking to broaden its service offering, trying to compete with big players like $ACE.

Donald Klumb took over as CEO from Richard Nespola in January 2012. After some initial success with a turnaround plan, the stock price and fundamentals had disappointed while the company failed to compete profitably with big consulting companies. Klumb had served as CFO since 1999. A big issue facing the company is that revenue is often being generated through big projects with limited customers. Another issue that arose overtime was that as its customers grew in size they took a lot of services that CRTN once provided to them to their own internal operations.

The New Deal

Former microcap fund manager and shareholder Peter Woodward stepped in as CEO of Cartesian in mid-2015. We agree with the new vision of management as they attempt to orchestrate a turnaround of the business fundamentals. Management concluded that Cartesian should not try to compete with providers of a broad range of services, but should carve out a niche in the telecom, media, and technology consulting arena to provide better differentiated services. Cartesian is also moving away from project-based consulting towards more stable recurring long term managed services. The company is also targeting telecoms and related companies that will need their services as network infrastructure continue to go through some transformations and upgrades. This “evolution” should continue for years, providing CRTN with longer term customer relationships and some visibility.

Results Starting to Pay Off

On November 10, 2016, the company reported Q3 2016 financial results that returned the company back to non-GAAP profitability after 3 quarters of losses.

We don’t think Q3 is the new bottom line run rate for the company, but it gives us a glimpse of what the company could look like and some comfort that the business may be able to sustain profitability (at least at the EBTIDA level) in 2017.

So, while we think it’s too early for CRTN to declare victory in a very competitive and changing environment, we think management has adopted the right plan.

There is no doubt risk to the story. The company has had some inconstancy with maintaining profitability. But it is not often you get an established company selling at around liquidation value with a good shot at substantial upside. So, we consider the play at current prices or less as a cheap one year call option with considerable upside. In 2014 when the company was a smaller and reporting profits the stock traded over $4.00 per share.

Why We Think the Stock Could Be Undervalued

CRTN has a stable balance sheet, with $21.9 million in current assets, $19.6 million in total liabilities, and $5.3 million in tangible equity that serves as a proxy for liquidation value. Note that the degree of confidence in this liquidation value is higher than with most companies because the parts that cannot be easily valued, like PP&E, are minor parts of the asset value. Most the assets are liquid. We believe the downside is somewhat limited by the low price and that the value of the assets has a tangible book value per diluted share of roughly 61 cents. We arrive at this figure using the company’s balance sheet, as is.

Another factor that causes the stock to be undervalued is that CRTN has an outstanding earn-out agreement that will cause them to pay cash and stock. The earn-out agreement is with Farncombe France SARL, a company acquired in 2015, and leaves CRTN with up to $1 million cash payable. The total liability, as of October 2016, is $1.9 million of which a portion is to be paid in stock and a portion in cash. A more accurate way of calculating liquidation value, therefore, includes taking the liability from the earn-out off the books, subtracting the maximum amount of cash payable under the agreement and adding the maximum number of shares issuable. This calculation yields a liquidation value of 68 cents per share. So essentially the earn-out agreement liability seems to be overvalued on CRTN’s books.

In the chart below, we show liquidation values based on the company books as well as our own internal calculations (including and excluding intangibles in both scenarios). The calculations can be found in the appendix.

There are old warrants and options outstanding, but they are currently so far out of the money (>$3.60 strike) that we do not consider them dilutive at this point.

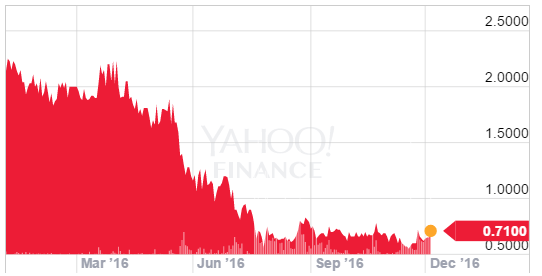

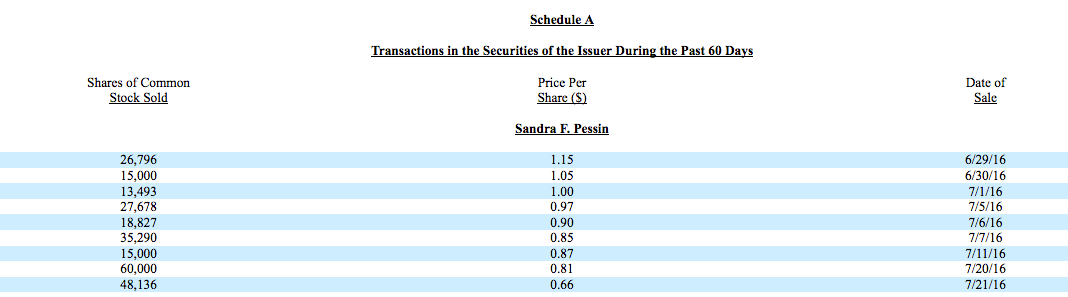

The stock recently come under great pressure when a major shareholder, Norman Pessin, sold shares during July on no news.

The stock has not recovered since then. The lack of news indicates that there was no superior short-term insight or insider information Norman Pessin was trading on. It looks like he simply wanted to exit his position. We consider this selling pressure artificial and without a fundamental justification.

Company insiders also seem to recognize the low price as temporary and artificial. They started purchasing shares upon the price decline that went along with Norman Pessin’s share liquidation.

As of January 2, 2016, CRTN had 360 total employees, of which 293 were full-time. At the current price this works out to an enterprise value per full time employee of around $22,000. The company recognized that it had to make efficiency improvements. It seems they have been cutting the head count and reducing costs as indicated by the decreasing SG&A expenses throughout 2016.

From the latest conference call:

“Q3 marked an important shift for us in achieving our near-term objectives and returning the business to adjusted EBITDA profitability and reducing our working capital burn. We surpassed those goals achieving overall net income profitability. We made substantial progress in managing our cost, demonstrating that our business can be profitable as long as we continue to execute on our sales pipeline and manage our cost efficiently”

We will construct more complete valuation scenarios once the company gives investors more clues about its sustainable operating metrics.

Caveats

- The business is downsizing, so revenues are expected to decline

- If efficiency improvements stop or revert, the company might once again be losing money from operations

- Delays or failures in big projects could have material adverse effects on the business

- Prior restructuring initiatives did not stick

- Our liquidation value estimate is only preliminary

- We need to determine cash burn on an on-going basis as it could influence liquidation values.

Appendix: Liquidation Value Calculations

(All numbers from latest 10Q)

*Calculations Per the Company’s Book, Excluding Intangibles

[(Book Value of Equity) – (Intangible Assets)] / Diluted Shares Outstanding

($5,984,000 - $655,000) / 8,777,000 (Page 16, 10Q)

= Liquidation Value per share: 61 cents

*Calculations Per the Company’s Book, Including Intangibles

$5,984,000 / 8,777,000

= Liquidation Value per share: 68 cents

*Our Calculations Properly Accounting for Earn-Out, Excluding Intangibles

[(Book Value of Equity) – (Intangible Assets) (Contingent Liability From Earnout Agreement) – (Maximum Cash Payable Under Earn-out) ] / [(Diluted Shares Outstanding) (Maximum Shares Issuable Under Earn-out)]

($5,984,000 - $655,000 $1,941,000 - $1,000,000) / (8,777,000 461,000)

= Liquidation Value per share: 68 cents

Note 1: Maximum Cash Payable Under Earn-out is £719,483 pounds sterling, converted to USD based on an exchange rate of £1.000 = US$1.393 as of October 1, 2016

*Our Calculations Properly Accounting for Earn-Out, Including Intangibles

($5,984,000 $1,941,000 - $1,000,000) / (8,777,000 461,000)

= Liquidation Value per share: 75 cents