Summary

- According to the SMLR CEO, WellChec contracts have been signed for immediate delivery from several top 25 health insurers.

- Insurers need valid risk models for patients. Obamacare or not, the SMLR risk assessment package appears to be carving out a new market.

- Recent Q3 proof-of-ROI accelerated their business outlook.

- SMLR transformed a 'basically worthless', and often skipped, annual wellness physical into a highly profitable, high patient satisfaction event. This is disruptive innovation by any other name.

- Whether SMLR's WellChec is the IPOD of annual medical exams remains to be seen, but it is fair to say that they are making traditional exams look like a Walkman.

Investigating contract wins

I wanted to find out why Semler Scientific (NASDAQ:SMLR) went from one 'tiny' WellChec contract last quarter to 'several large' contracts this quarter, and an even stronger 2016 outlook, after a notably brief Beta testing period, and despite all of the questions surrounding Obamacare's viability.

SMLR CEO Doug Murphy-Chutorian recently revealed sharp contract growth in the Q3 earnings call, being fulfilled as we speak in Q4:

Of importance during the third quarter, our sales team obtained several new contracts for our WellChec service. We anticipate WellChecing for these new customers in the fourth quarter of 2015 and continuing into 2016. Potential customers for WellChec range from small health insurance plans to major health insurance plans to other organizations. Our recent contract wins include customers from both types along this spectrum…We believe that the business prospects and opportunity for Semler improved significantly during the third quarter of 2015 as we received several larger orders for our WellChec service which we began to fulfill in the fourth quarter that we're currently in, in 2015…two contracts as I said were started before the end of the third quarter and multiple other ones ongoing in the fourth…the revenue numbers here are substantially bigger than what we've reported before...At this time we're not giving guidance other than to say these contracts are large.

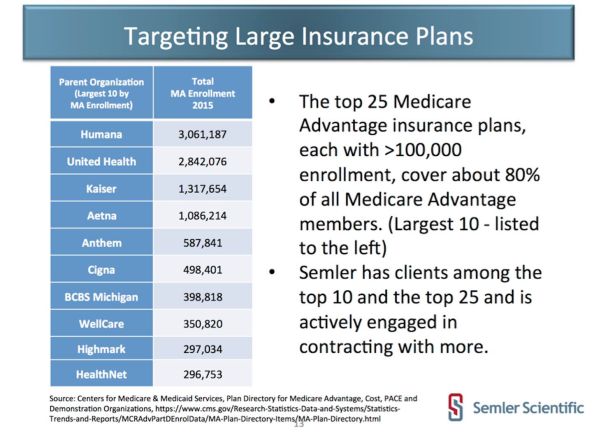

It is very much worth your time to listen to SMLR's conference call to hear how the CEO emphasizes words like 'substantially bigger' and the like. SMLR has 5 of the top 15 Medicare Advantage insurance providers counted as customers, including Unitedhealth Group (NYSE:UNH), 2.8 million Medicare Advantage members strong, and several other yet unnamed customers. We do know via Medicare's website that the top 15 insurers each have Medicare Advantage rolls of between 100,000 and 3,000,000 each.

Details are withheld regarding how 'large' these concurrent contracts are being executed right now. But we do know that if any 2 of their top 5 customers sent them 1% of their customers or more, SMLR is going to surprise Wall Street with profitability. Include these reference points with your due diligence:

- 5,000 WellChec patients per quarter at historical $750 billed per patient, and 80% gross margins, are needed to turn SMLR profitable, on top of their very steady, predictable, recurring Quantaflo revenue.

- Every additional multiple of 5,000 WellChec patients per quarter given same assumptions results in about $2.5 million of free cash flow, per quarter.

But well before considering an investment, please study below Semler's value proposition in depth. We need to know exactly why contract growth is occuring, and whether it is sustainable.

The reasons appear to be 3 fold:

1 WellChec converts annual wellness exam bystanders into highly satisfied customers

2 WellChec delivers immediate Proof-of-ROI

3 WellChec increases Medicare Advantage Star Ratings, directly translating into higher revenues

Semler's Innovation: Preventative Speed Diagnostics

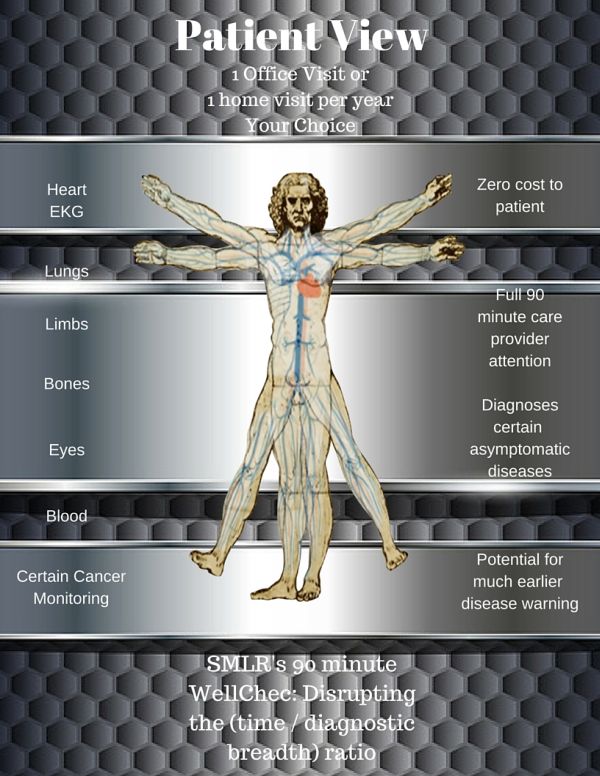

As a brief overview, WellChec is SMLR's answer to the patient's question, "Why can't I get a very comprehensive medical exam in at my home and at my convenience, once per year, fast and for free?"

Semler answered with a 90 minute portable exam, encapsulating the prohibitively slow, expensive, and scattered chronic diagnostics field into 1 comprehensive 'WellChec'. The below graphic illustrates SMLR's value proposition to patients.

Proof of ROI

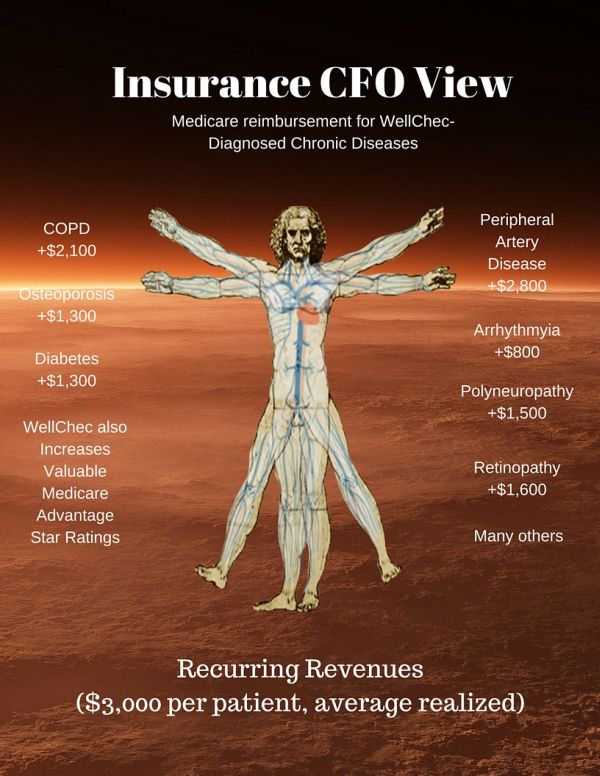

The patient invests about 90 minutes of time for a WellChec, conveniently scheduled at a medical office or their home. The patient pays nothing. The insurance company pays Semler an average of $750 per WellChec. Semler uncovers new chronic conditions. The Insurance company sends SMLR's complete Medicare diagnostic coding and paperwork to Medicare for an increase in annual, recurring funding for this patient. Noting the Q3 average increase of $3,000 for each $750 investment, SMLR gets paid promptly, and contract sizes are growing commensurately.

I generated the above graphic using financial data from the Centers for Medicare and Medicaid, and SMLR's most recent quarterly earnings call.

Getting patients to show up: Disrupting the wellness exam value proposition

Dr. Ezekiel J. Emanuel reflected a widespread opinion about the limited value of the traditional annual physical. In his January 2015 New York Times Op-Ed entitled Skip Your Annual Physical, Dr. Emanuel stated that screenings are on the whole, not worthwhile:

"There is only one problem: From a health perspective, the annual physical exam is basically worthless…(Exams) may discover a disease, but one that either would never have become clinically evident and dangerous, or one that is already too advanced to treat effectively." Dr. Ezekiel J. Emanuel

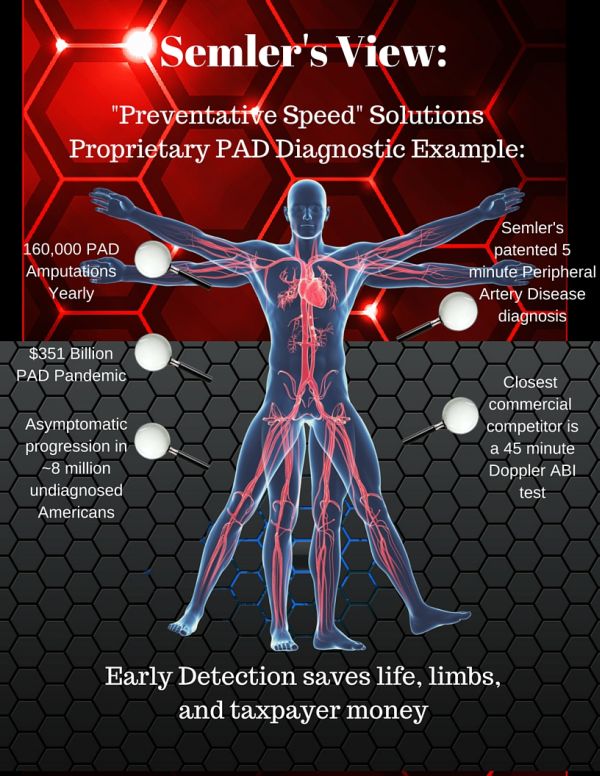

Dr. Emanuel has several good points. 160,000 Americans that lost their legs last year due to Peripheral Artery Disease (PAD), which SMLR's WellChec could have diagnosed in 5 minutes as part of a 90 minute WellChec, the proprietary and only preventative speed PAD exam on the market, may disagree with him however. SMLR's PAD competition is Doppler Ultrasound ABI, which requires a physician referral, costs roughly $600, requires specialty vascular medical personnel to administer, and at a time cost of about 45 minutes plus travel time to a vascular specialty clinic. Further underscoring the problem with status quo, PAD is asymptomatic in 75% of cases, thus presenting no cause for ordering a test until it is too advanced to treat effectively.

Undiscovered and untreated, PAD progresses to amputations, heart attacks, and strokes, and a $290 Billon annual price tag. Semler is changing that. WellChec's early warning about a broad array chronic diseases including PAD, which meet Dr. Emanuel's criteria of dangerous and detectable early enough to treat, is a major driver behind WellChec's market share gains.

Educated consumers are skeptical about the value of annual wellness exams. SMLR's WellChec is changing that, too. WellChec customers answered the question "Will you come back for another WellChec next year" with "absolutely yes" 80% to 95% of the time to date, according to SMLR's CEO during the Q3 earnings call Q&A. SMLR's CEO emphasized that SMLR intends to continue to provide a premium quality experience to keep satisfaction ratings very high, which he believes is one of the major reasons for increased contract volume and breadth.

Who loses and who wins when WellChec gains market share?

WellChec gains come at the expense of specialty diagnostic centers. WellChec has consolidated and greatly reduced the aggregate time and expenses associated with a number of formerly distributed diagnostic services.

SMLR and primary care physicians (PCP) mutually benefit, since PCPs can now outsource the mandatory, and difficult to schedule, annual wellness visit to SMLR. With an average of 2300 patients per primary care physician in the United States, the time re-allocation opportunities for overstretched doctors is significant. Note that Semler keeps its staff lean by training outsourced medical staff to administer WellChec, delivering 80% gross margins inclusive of contract personnel costs.

SMLR and insurers mutually benefit in a number of ways:

1 Increased 'Capitation' premiums, a direct insurer revenue driver

2 Higher Medicare Advantage Star Ratings, a direct insurer revenue driver

3 Increased patient treatment cost visibility, reducing insurer risk

Insurer win #1: Capitation Revenue

Capitation is a system of fixed payments per year per patient, which pays more based on the number of chronic conditions diagnosed and documented. So in other words, Medicare pays about $10,000 per patient annually to the Medicare Advantage Insurer. Medicare pays an additional $2,100 per year if the patient is diagnosed with COPD, one SMLR's many WellChec diagnostics. SMLR's WellChec service has averaged $3,000 per patient in the form of increased annual capitation payments for insurers thus far.

Insurer win #2: Lucrative Medicare Advantage Star Ratings

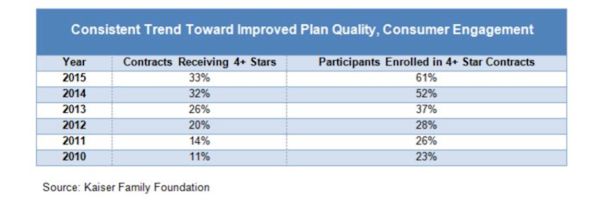

Medicare Advantage star ratings directly affect the bottom line. CMS rewards 4 and 5 star contracts and penalizes sub-3 star insurers yearly. CMS initiated 4 star insurer bonuses, a 5% increase in the benchmark payment, back in 2012*. Insurers rating 2.5 or less for 3 consecutive years can no longer participate in Medicare Advantage. As you would expect, higher rated plans have increased annual enrollment rates as well, further driving revenue growth for insurers.

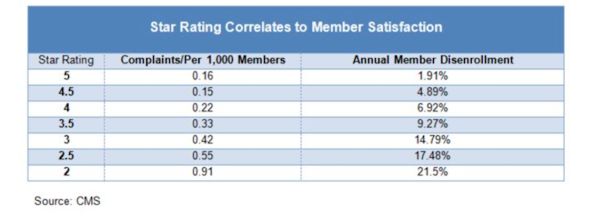

The table below illustrates that star rating financial incentives are working, and that consumers continue to migrate their dollars toward high star rated plans.

I extracted the below Medicare Advantage Star Rating criteria from Medicare.gov. SMLR's tools directly improve #1, #2, and #3 of the 5 criteria for their insurer clients.

MEDICARE ADVANGE STAR RATING CRITERIA

1 Staying healthy: screenings, tests, and vaccines

2 Managing chronic conditions: Includes how often members with different conditions got certain tests and treatments that help them manage their condition.

3 Member experience with the health plan: Includes ratings of member satisfaction with the plan

4 Member complaints

5 Insurer customer service

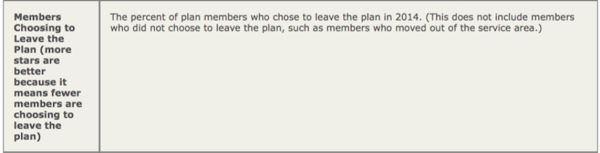

I extracted the above graphic from Medicare.gov, which gives greater detail of the #3 Member Experience Star Rating criteria. As you can see, there is a dual penalty for losing customers, both revenue loss and Star Rating erosion. An annual event that increases customer satisfaction, as WellChec has done thusfar, is a welcome contributer to an insurance plan.

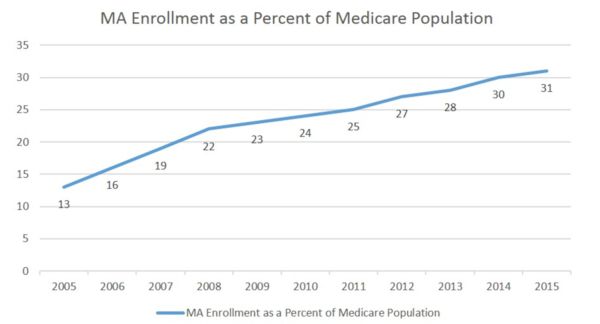

Member satisfaction, member retention, early chronic condition identification, regular screening, and Insurer revenue growth are very much interrelated for the 17 Million patient and growing Medicare Advantage market. SMLR's WellChec boosts each of these key 'Star Rating' revenue drivers.

The below chart shows that the 17 million patient Medicare Advantage market itself has steadily gained market share but still has considerable room for growth. (click to enlarge)

*Contrarian View: Medicare Star ratings pre-date Obamacare (2007 inception), but some financial bonus incentives tied to star ratings are directly tied to Obamacare. Thus the 2012 through present insurer bonuses for outstanding star ratings carry significant political risk.

Insurer win #3: Obamacare or no Obamacare, this is the risk business

Customer turnover is a well-documented health insurer problem even amongst highly rated healthcare plans. This translates to hundreds of thousands of new patients with unknown health risks added to insurer balance sheets annually.

Obamacare or no Obamacare, health insurance companies are in the risk business, and knowing as much about your patients medically as possible is a key competitive advantage. Paying SMLR $750 each to screen prospective new customers in order to positively identify several chronic conditions which may carry 5 figure plus price tags in the near term is profitable business, and in no need of Government subsidy.

Scaling business model to meet contract growth

Semler is run by 24 employees, of which 3 are executive officers, as well as a 16 member sales and marketing force. A Google Patent search reveals that the officers and directors are mostly physician-inventors, as is their CEO who is named as a inventor/contributor to 20 patents. SMLR develops their own software and diagnostic devices, while maintaining maximum flexibility for expansion, outsourcing WellChec exams to contractors, who have produced high patient satisfaction ratings and are key to the 80% WellChec gross margins.

Valuation and Risk

This is not the same company that it was 6 months or even 3 months ago.

6 months ago, SMLR was a steadily growing one trick pony called 'Flochec/Quantaflo' (proprietary vascular disease rapid diagnostics) with profitability projected some 2 years away, certainly after an additional round of financing.

3 months ago we found out that their experimental Trojan Horse WellChec had performed extremely well given only 'one tiny' contract (SMLR CEO page 5, Q2 earnings call) of about 200 patients.

Today, as a result of delivering customers ROI multiples that of the $750 per patient billed, we have a sub-$15 million fully diluted market capitalization SMLR executing several concurrent (SMLR CEO page 4, Seeking Alpha Q3 earnings call transcript) larger contracts as we speak, and a robust and growing 2016 contract pipeline. SMLR's CEO will not quantify what exactly a large contract looks like, but we do know that SMLR has 5 of the top 15 health insurers as clients, each of which has 6 to 7 figure Medicare Advantage customer lists. What we know is that a couple hundred patients is a tiny contract to SMLR, their follow-up orders from several different clients are larger, and at historical gross margins 5000 quarterly WellChec patients push SMLR into positive cash flow with room to spare. It seems very likely that profitability has moved from a long range goal to a near term goal.

Variant View: Speculative investors need also fully consider the SMLR CEO's fair warning that this business model is literally months old, and although greeted enthusiastically, is only now being implemented on a broad scale.

It is tempting to value SMLR as though a mining company that currently has the only cost effective tools available to extract a mineral of economic and human health value. But valuing this company with any precision is next to impossible, since exact contract magnitude and percentage of contracted patients ultimately scheduled and tested incurs too many variables to quantify in these early innings. Be certain to invest the time to read the last few earnings call transcripts in their entirety.

It is refreshing however, to see a company that unveiled its best product a full year post-IPO, consequently allowing us an entry point that does not factor in even 1% of the addressable market despite having 5 of the top 15 customers for such services already contracted. SMLR carries all of the sub-$100 million dollar company risks you would expect, but clearly very little of the upside potential is baked into the cake.

Conclusion:

This a near term contract growth story, a newly constructed Trojan Horse evolved of a 1-trick pony, and perhaps best of all the unfolding of a potentially wonderful human story. A compelling metamorphasis of the annual wellness exam, SMLR's WellChec has unique potential to save life and quality of life for years to come.

DISCLAIMER: GeoInvesting has no affiliation with the author of this report in any way and is not endorsing his research, nor has GeoInvesting vetted this information in any way. The GeoTeam does not attest to the accuracy of the information contained in this report and always urges investors to conduct their own due diligence. The GeoTeam has received no compensation for the dissemination of this report. The GeoTeam may or may not have a position in any stocks mentioned in this article prior to its publication.