Buying MHGU Before Rest of Market Discovers This Undervalued Gem

Meritage Hospitality Group Inc. operates quick-service (Wendy’s) and casual dining restaurants. As of April 17, 2015, it operated 151 restaurants in Florida, Georgia, Michigan, North Carolina, South Carolina, and Virginia.

On June 1, 2015, we alerted GeoInvesting premium members that we initiated a moderate sized long position in MHGU and coded the stock a GeoBargain on the Radar when trading at around $7.90. Our action was based on a robust fiscal 2015 growth outlook and a 100% increase in its previous special dividend announced on May 20, 2015.

On July 14, 2015 MHGU reported strong fiscal 2015 second quarter results:

- Q2 2015 sales of $51.0 million vs $40.5 million in the prior year period

- Q2 2015 net earnings of $2.2 million vs $1.2 million

- Q2 2015 EPS of $0.29 vs $0.16

Quotes from management:

“Our newly renovated Wendy’s restaurants are generating compelling double digit same-store-sales increases along with high customer satisfaction. The system goal is to have 60% of the restaurants image activated by the end of 2020, and we are currently on schedule for 10% of our restaurants to be image activated by year end,” stated Meritage CEO, Robert E. Schermer, Jr.

“Additionally, the Company is developing a multi-year project pipeline for expansion in its uniquely branded chef-casual restaurants, which we believe will continue to enhance operating margins,” added Mr. Schermer.”

Management stated the Company is currently performing ahead of its 2015 earnings guidance listed below:

- Sales growth of 25% to 30%

- EBITDA growth of 60% to 65%

- Net Earnings growth of 100%

- Special dividend growth of 100%

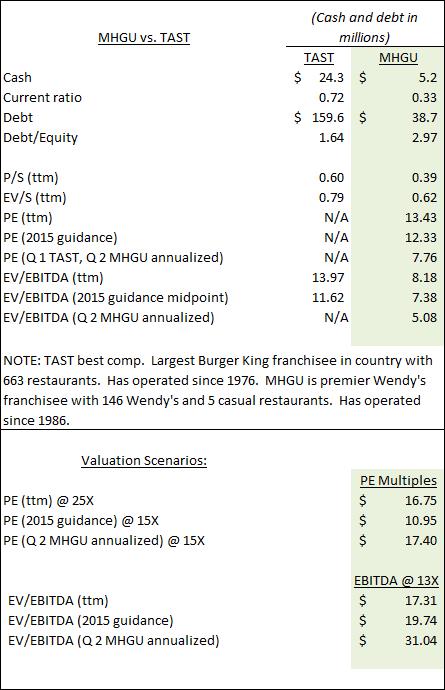

Valuation metrics and scenarios

The GeoTeam interviewed CEO, Robert Shermer, on June 17, 2015, and promptly coded MGHU as a GeoBargain at $8.50. Our key takeaways from the interview include:

- The key driver of MHGU’s business is its 146 Wendy’s franchised restaurants. Wendy’s is a 45 year old brand with 6,500 restaurants and over 300 franchisees. The average age of a Wendy’s franchisee is 65 and they own 6 restaurants. Wendy’s has embarked on an “image activation” campaign that will systematically force franchisees to either upgrade their restaurants or sell them to others who will. The average cost to update the Wendy’s restaurants is $500,000 to $720,000 and it is assumed only about a third of franchisees will do so. That means larger franchisees like MHGU will have ample opportunities to acquire additional restaurants as Wendy’s franchises move from weaker to stronger hands. Wendy’s hopes to ultimately reduce the number of franchisees from 300 to 30.

- MHGU’s has had excellent results acquiring and upgrading Wendy’s franchises. Typically, restaurants are acquired for 5.5 to 6.25X adjusted EBITDA. On average, the restaurants MHGU has acquired to date had around $490,000 trailing EBITDA. MHGU has been able to leverage its IT platform and operations and administrative resources and infrastructure to nearly double the EBITDA of acquired restaurants. Further, MHGU’s restaurants that have had image activation makeovers are generating 25% to 33% more revenue than before meaning there is substantial upside potential in the company’s existing holdings. Management expects to have 14 additional newly built restaurants in service by the end of 2015.

- MHGU’s net income of $2.8 million for 2014 fell well short of management’s guidance of $4.3 million for understandable non-elective and elective reasons. The cost of beef far exceeded expectations during the year but has since fallen back. Profits were also temporarily impacted by lost revenues and preopening costs of restaurants acquired in Atlanta. 2015 operating results will be greatly augmented by those restaurants that were placed back in service in January.

- Management is projecting 2015 revenues of $205 million, EBITDA of $14 million, and net income of $5.4 million or nearly $1.00 per share. Longer term, they expect to have 250 restaurants generating $500 million annual revenues by 2020.

Caveats:

- While quarterly revenues are expected to grow steadily, quarter to quarter net income is likely to be volatile. The key swing factor is preopening costs that are recognized in full when restaurants are placed in service. There is an ebb and flow to deals so which quarters will be impacted and by how much is somewhat unpredictable. Investors should keep in mind that preopening costs are positive expenditures for the business since more restaurants are being upgraded or newly built and placed in service benefiting future periods. We encouraged management to consider reporting both GAAP and non-GAAP earnings so investors can readily see the impact of preopening costs.

- Input costs such as beef can be volatile and the ability to pass along price increases to consumers is limited. A material increase in the minimum wages of workers could also impact operating results.

- MHGU has a material debt burden of around $42.4 million and a low current ratio of .33. Note, however, that the company generated $8 million cash flows from operations in 2014 and has a favorable debt amortization schedule. Giving further comfort is the rapid growth of EBITDA that at the midpoint of guidance for 2015 would be $14.3 million and $20.8 million for the next twelve months if Q 2’s EBITDA is annualized.

- Management missed 2014 guidance due to the delayed timing of acquired/renovated restaurants coming online in Q 4. Q 2 operating results are running ahead of guidance.